I attended the FIA event last week in Chicago. Much of the same stuff. Bank capital, swaps regulation, clearing, MIFID. And the obligatory panel on bitcoin.

Over the past couple years, Bitcoin panels in our industry have tended to start out with the moderator making clear “we’re not going to talk about bitcoin the currency, but rather the blockchain”, and over the course of 75 minutes you would hear each panelist ponder how great it would be to settle a syndicated loan in 30 seconds instead of 30 days. Basically everything that Jamie Dimon extolls as the valuable part of bitcoin technology.

But this panel was different. This panel was about bitcoin the asset class. It was a refreshing perspective on changes within the derivatives industry in response to one of most exciting and volatile asset classes in a decade.

But this panel was different. This panel was about bitcoin the asset class. It was a refreshing perspective on changes within the derivatives industry in response to one of most exciting and volatile asset classes in a decade.

Don Wilson (Mr DRW) led the panel with representatives from across the industry. The panel, and a small background on them:

- Mike Belshe, CEO of BitGo. BitGo’s main business is analogous to a custody bank in our industry. In other words, they hold your assets (bitcoin) and keep it safe, provide reporting, etc. The thing about Bitcoin is that quite frankly, nobody needs to have a custodian; You can hold your private keys on a piece of paper, your brain, a thumb drive, etc. But if you’re a business not specialized in cyrptocurrencies, that’s a tall order. What happens if the guy with the private keys gets hit by a bus? BitGo has also done work on private blockchains, such as their effort with the Royal Mint, effectively allowing you to hold virtual gold (held by the Mint).

- Bobby Cho of Cumberland Mining. Cumberland is the crypto-arm of DRW, one of the largest proprietary trading firms in the world. Bobby’s team appears to have been making markets in crypto for a few years.

- Juthica Chou, CRO of LedgerX. LedgerX is both a CFTC-registered SEF (derivatives exchange) and DCO (clearing house). In laymans terms, the SEF means they can execute OTC derivatives, the DCO allows them to clear those derivatives.

- Michael Mollet of CBOE, the primary equity options exchange in the US. (Eg S&P and VIX). CBOE are launching a bitcoin future in the coming months.

- Adam White of Coinbase. Coinbase runs a couple of crypto exchanges: Coinbase (retail/business oriented) and GDAX (institutional). They claim to be adding 30,000 to 50,000 new clients PER DAY!

It’s clear from the discussion that the ecosystem for bitcoin and other cryptocurrencies is coming together. Basically, you now have, or will soon have, liquidity providers (DRW and others), institutional exchanges (eg GDAX and Kraken for physical, LedgerX for derivatives), listed futures (at CBOE), clearing houses (LedgerX), and custody firms (eg BitGo). Basically all of the plumbing required for an asset class to absorb institutional sized trading. And of course whispers of ETFs.

There was one particular highlight of the panel that stood out to me. To set the scene, this was mostly your typical derivatives industry crowd: a bunch of old men in suits. Maybe a few khakis. Then, during the Q&A, the mic gets passed to a young exec at a crypto exchange, dressed in his finest t-shirt and hoodie. He proceeded to ask his question about any perceived downside price risk in crypto, complete with a caveat “Dude, don’t get me wrong, I am super-super bullish”.

Couple other notable points:

- LedgerX was a bit dodgy on their bitcoin options plans, besides saying they intend to launch (but they had launched!). The interesting thing here was that as DCO, they require full collateralization. So if you sell a call on 10 BTC, you have to have all 10 BTC pledged in advance. Which can be appreciated, given the supply of Bitcoin is finite. Imagine that liquidity crisis!

- CBOE Futures Exchange (CFE) intends to make their Bitcoin future cash-settled. Which raises the issue of what index you would use? (Answer below)

- Gemini Trust (Winklevoss brothers) have been running a daily auction to fix both BTC and ETH prices every day. There’s your index!

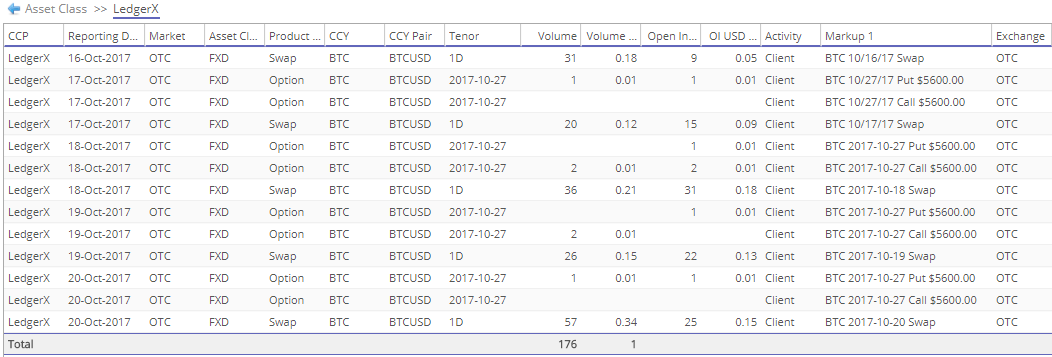

LedgerX Data

The day after the event, I got wind of a press release (or blog) from LedgerX announcing they had gone live that week, and had completed over $1,000,000 worth of notional in bitcoin derivatives. While our industry is used to numbers in the trillions of notional, that is quite an increase from zero!

And because LedgerX is fully registered with the CFTC as both a DCO and a SEF, I knew there must be some data out there. So in true Clarus fashion, we loaded that up into CCPView.

So we can see some activity across both “swaps” and “options”. Some caveats/observations:

- We have assigned an “FX” designation to BTC. It just feels more appropriate. But I suspect the CFTC govern these as “Other Commodity”?

- The swaps are all 1D tenor. Now, I presume that is just a forward. So an obligation to buy BTC tomorrow. This would use the technical CFTC designation of “swap” for an outright forward. But I suppose they could be what an FX trader would call a swap – eg sell today, commit to buy tomorrow, akin to rolling a position. But surely not, it has to be an outright. Right?

- Finally, I’m not certain if the data we pulled was execution (SEF) and clearing data, or just the latter. I presume it’s both, but I guess the DCO could have cleared OTC bitcoin “swaps” that were executed away from the exchange (off-SEF).

How Volatile Is Bitcoin

One excellent outcome of swaps and options data is we could theoretically begin to build a BTC forward curve and imply some volatility.

To be fair, there have been exchanges such as Kraken and Poloniex which have allowed leveraged short selling of crypto, so there has been some (thin) data on lending rates, which we could use to generate a forward curve. But having forwards and options on an exchange together gives us a lot to work with. Only small problem being we only have 1-day forwards to work with, yet we seem to be working with 1-week options.

Heck, let’s not get tied down in nitty gritty of spot and forward rates, and lets just get some numbers out.

Using LedgerX data, we can start to get a feel for how the market is pricing bitcoin vol:

- On 18-Oct, with BTC mid at $5,387, the 9-day, $5,600 OTM calls were trading at $100/$200 (that’s quite a spread!). Implying a vol of roughly 55/85. Puts were similar. It’s a 40-delta-ish option.

- On 20-oct, with BTC mid at $6,070, the 1-week $5,600 OTM puts were trading at $70/$130. Implying a vol of roughly 72/96. It’s a 20-delta-ish option.

Let’s just call it 75 vol for the time being. And that’s a 1-week option.

Granted I’ve dumbed this down to using mid spot rates, no forward points, and we’re stuck observing a single option that was on opposite ends of the smile after 2 days. So we’re going to need more data to refine this. But let’s not get too picky here. This was week one of a soft-launch.

Worth putting this into context. We’re talking 75 vol. 1-week vol across all G7 currency pairs are trading in the single-digits. So you can see why this market might be attracting attention.

Summary

Bitcoin now has much of the requisite ecosystem to facilitate institutional participation in OTC derivatives. Exchanges, SEFs, liquidity providers, custody, and DCOs.

Exciting times in OTC derivatives.

A couple of thoughts:

1) Bitmex is trading a futures contract with December expiry, which gives us a ~2m forward price of $120 discount to the current price (do we still call it Spot, even with immediate delivery?). Assuming 2m USD yield of 1.05%, we can caluculate 2m BTC yield of about -12%. Yes. Negative yield. A quick examination of their historic price charts suggests that the futures price is more an indicator of market sentiment than a reliable source of yield. The future price is at a discount to spot in a falling market and a premium to spot in a rising market. This suggests that OTC traders should not be hedging BTC yield risk with yield-bearing instruments (which don’t yet exist), but with adjustments to their delta ratios.

2) Historical Volatility gives us sensible ranges for implied vol. 1week historical vol obvious fluctuates a lot. In the past year it has been as low as 10% (mid December, 2016) and as high as 200+% (mid July, 2017). 1m historic vol. has seen a range of 20% to 140%, 2m range has been about 40% to 120% and 3m has been about 60% to 110%. So your 75% estimate seems quite plausible.

Hi Andy, thanks for the comments and analysis. I love the -12% yield. I guess it makes sense that the forwards/futures are purely market sentiment rather than yield, as there is no true need (and no good way) to lend/borrow BTC.

Re vol – I was informed today about an unregulated options exchange (deribit) that has been around for a while, and the implied vols there are in the same sort of vicinity. Spreads also wide. Presumably a regulated (trusted) exchange and DCO will drive institutional interest and create a tighter market.

Great article BTW. I have also been wondering when BTC OTCs will come of age.

Thank you for the article. Any comment on whether CME offering cash-settled futures will remove the ‘limited supply’ bull case for bitcoin with unlimited ‘paper’ bitcoin? My concern is price manipulation. Thanks.

Yes its an interesting one. Personal opinion is that ignoring the limited supply of the asset is dangerous, and opens up any asset to manipulation. Probably not too different to daily LIBOR fixings (at least LIBOR manipulation in past years) where the derivatives market was multiples in size of the cash market.