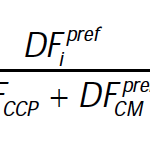

Capital requirements for exposures to CCPs

Following on from my article SA-CCR: Standardised Approach Counterparty Credit Risk, I wanted to look at the related topic of Capital requirements for Cleared Swaps and get a sense of the size of these requirements. Background In March 2014, the Basel Committee on Banking Supervision (BCBS) published it’s Standardised Approach (SA-CCR) for measuring exposure at default […]

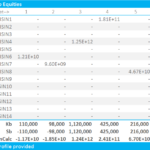

ISDA SIMM™ in Excel – Equity Derivatives

We build an IM calculator in Excel for Equity Derivatives under ISDA SIMM™. The methodology builds on the margin methodology for Rates products, and uses very similar formulae. We cover all forms of IM. This blog is for the Delta Margin. There are subtle differences to the implementation for Rates, mainly around the concept of “buckets” […]