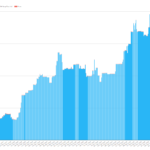

RFRs – CHF SARON Activity

We noticed that the SNB quoted Clarus data at the most recent CHF SARON working group. We show that Open Interest in SARON now stands at nearly CHF60bn. Most of this is in short-dated products, less than 2 years. We find that 77% of risk is traded in tenors shorter than 2 years. Markets need […]

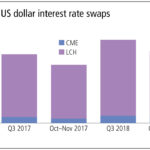

Swaps Data: Volumes Up amid Volatility

My monthly Swaps Review in Risk Magazine looks at: Cleared Interest Rate Swaps in USD, EUR, JPY Cleared Credit Default Swaps in USD, EUR Cleared Non-Deliverable Forwards Volumes in 3Q18 vs 3Q17 Volumes in Oct-Nov18 vs Oct-Nov17 Growth rates in these periods Please click here for free access to the full article on Risk.net.