Today we look at any trends in bespoke Fixed/Float swap trading On-SEF.

Last year I wrote an article about the longer term trends in the US swaps market by asking “What is Left off-SEF?” We determined that, generally speaking, 2/3rds of the USD Fixed/Float swap market is On-SEF. The Off-SEF world was generally a bunch of bespoke stuff.

Recently, I was asked a similar question another way around – “How much of the market is Non-MAT, but does trade on SEF?”

As a starter, I always like to remind myself what is MAT. It’s nice that this hasn’t changed (ever) in 3 years, and is still found in a PDF on the CFTC website. Generalizing, for Fixed/Float IR swaps, the rules boil down to:

- USD, EUR, GBP:

- 3M & 6M Libor, Fixed Notional, Standard terms/daycounts

- Spot Starting, Par Rate

- USD also gets some IMM-dated swaps:

- IMM with Par or MAC coupon

- Only the next two IMM dates

DATA

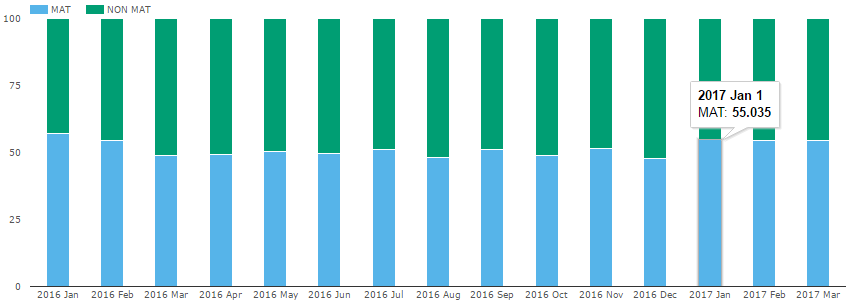

If I pull data for USD Fixed/Float swaps over the past 15 months, and look at it by whether the swap meets the MAT classification, I get:

Which tells me that pretty consistently, 55% of the USD Fixed/Float market is MAT (by trade count). I get similar answers for risk terms (~58%) and notional terms (~50%).

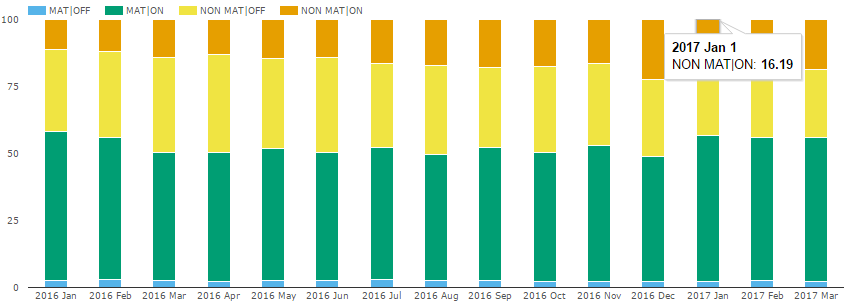

If we refine this a bit further and break this out by whether the swaps were traded on a SEF:

Few things to point out here:

- MAT & OFF: We see about 1% of swaps are MAT, but traded Off-SEF !? Interrogating these, they do appear MAT & non-Block, so I don’t know why they are flagged as Off-SEF. But let’s not start an FBI investigation here.

- MAT & ON: This is what we expect to see, a good chunk, roughly half the market, is MAT and traded on SEF.

- NON-MAT: You would be excused for thinking that everything Non-MAT is traded Off-SEF, but the Orange bars tells us that a growing portion, up to 22% of the USD market (in Dec 2016) was Non-MAT but traded on a SEF.

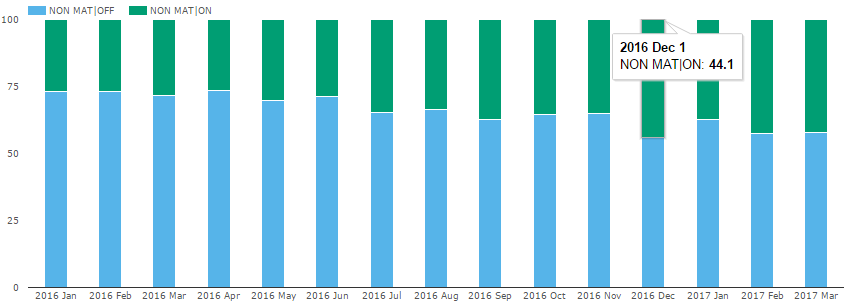

So refining our view to only Non-MAT’d swaps over the past 15 months:

This paints a nice picture: That over the course of the past 15 months, market participants are electing more and more to trade their non-MAT’d products on a SEF. December 2016 was a high watermark for this, where 44% of Non-MAT swaps (by trade count) traded on a SEF.

So this raises two questions:

- What are these Non-MAT’d products that are trading on SEF?

- What SEF’s do they trade on?

What Non-MAT Swaps Are On-SEF

So by just filtering on Non-MAT, On-SEF, USD Fixed/Float swaps, we can pull some stats. Remember now, this means we are looking at something like 16% of the total USD Fixed/Float swaps market here:

- 75% were reported by DTCC SDR, and 25% by BBG SDR

- 99% were cleared. Which makes sense. Though I do wonder about that 1% non-cleared: can a SEF execute a bilateral swap? The answer is obviously yes, they can, when you consider some of the non-clearable products that get traded on some SEFs. But, what do SEF’s do for things like credit checks in the case of bilateral? Must be in the rulebooks.

- Most important is breaking down these On-SEF trades by subtype:

- 51% are Back-Starting (related to portfolio compression / maintenance)

- 19% are Forward starting (not IMM or Spot starting)

- 6% are IMM, but beyond the prescribed first 2 serial months

- 11% are what we call Non-Standard. Predominantly, these have non-Par coupons, and hence up-front fees.

- 13% are Spot Starting. Predominantly Non-MAT’d tenors like 8 , 9, 11 and 25 year. Lots of them!

I hadn’t considered it before, but I presume if you are trading 10 year swaps on SEF all day and now you need to trade a 9 year, are you going to suddenly pick up the phone and call your favorite dealer(s) just because the trade is not MAT? As long as you’re doing an RFQ anyhow, why not use the SEF. Ditto for off-the-run IMM and forward start.

And – my thought for the day – why are 8 and 9 year swaps not MAT again?

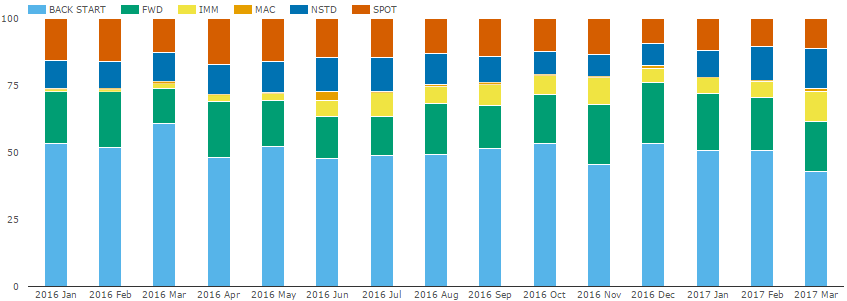

For full disclosure, we can plot these subtypes by month to spot any trends in any particular subtype:

The only thing we might glean from here is that more and more off-the-run IMM’s (Yellow bars) are trading on SEF.

Quick Exit

I’ve run out of time for today. I would like to answer the other question of which SEF’s these trade on. But we largely know half the story already. Given that half of this Non-MAT universe is back-start / portfolio maintenance stuff, it is the usual suspects for trade compression that are doing these trades (TrueEX, Bloomberg, Tradeweb). As for where the Off-The-Run IMMs, other forward start, and cock-dated spot starting swaps are trading – we’d just need to turn to SEFView and interrogate that data. Perhaps for another day.