Having blogged for a good few months now, it becomes second nature to look for different lines of analysis within the major markets that we haven’t yet covered. As a result, we find new ways of developing the existing products and adding to the layers of data.

However, always searching for that something new can lead us to forget how strong and powerful the core product itself actually is.

I discovered this on a recent flight to Australia when I thought I’d try to learn a little bit about the local swaps market before touching down. I briefly traded AUD swaps in London for a couple of years, and to be honest it was always very difficult to get a feel for the market. Much like GBP swaps, it is a very flow driven market, and as a result the banks with the largest books tended to enjoy an information asymmetry over the rest of the market.

Honestly, I think I managed to learn more about the AUD market through a ten minute review of October volumes via the various Clarus tools than I did in two years trying to trade the market itself!

Despite the fact that AUD swap markets are not written about to anywhere near the same degree as USD and EUR swaps, we nevertheless benefit from the same degree of trade reporting. This is, to a large extent, down to the pragmatic rule-making from ASIC that allows Aussie banks to report their trades just once, to the DTCC.

We cannot be sure that the figures from DTCC cover the same proportion of the market as we see in USD swaps – but nonetheless it is still a huge step forwards in price discovery and gives us a good idea of what sizes trade across which products.

AUD Market Size

There is a headline figure that dogs the swaps market in any Bloomberg article – “the $426 trillion interest rate swap business”. Afterall, everyone loves a big number. But is that really a relevant number? If you have a swap to trade that is only 0.1% of that size…surely it won’t move the market? Go to your dealer on Bloomberg and ask for a 10 year swap in $426bn and let us know what they say in the comments below…..

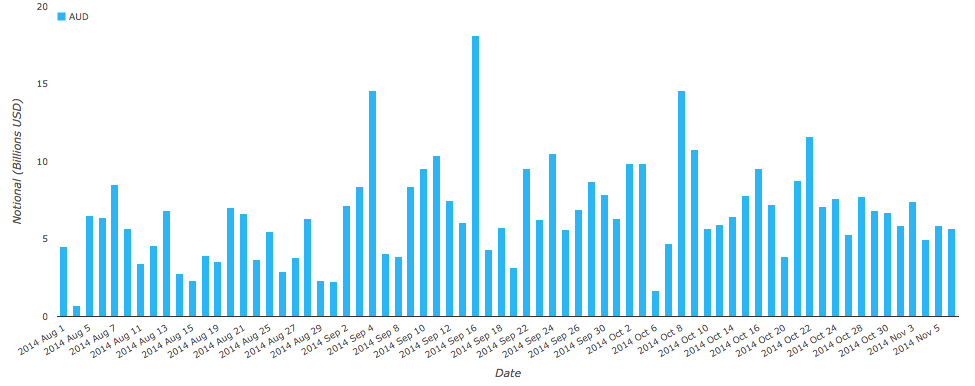

Anyway, I digress. The point is, that when you come to trade a swap, a more telling statistic is average daily volume – ADV or turnover. We can easily pull this from Clarus, where we can see the daily volumes traded in the three months until the end of October for all AUD swaps:

From which we can see that:

From which we can see that:

- The IMM date in September stands out as the largest trading day with nearly US$20bn equivalent trading.

- Whilst October 15th and 16th saw record volumes for the CME and SEF trading overall, October 8th (after the RBA meeting on 7th October) and October 22nd (after the publication of the minutes to the 7th October meeting) were more significant for volume jumps in AUD swaps.

- ADV is around US$7.5bn equivalent.

- Even AUD swaps suffer from the August lull….when it’s not even Summer!

AUD Products

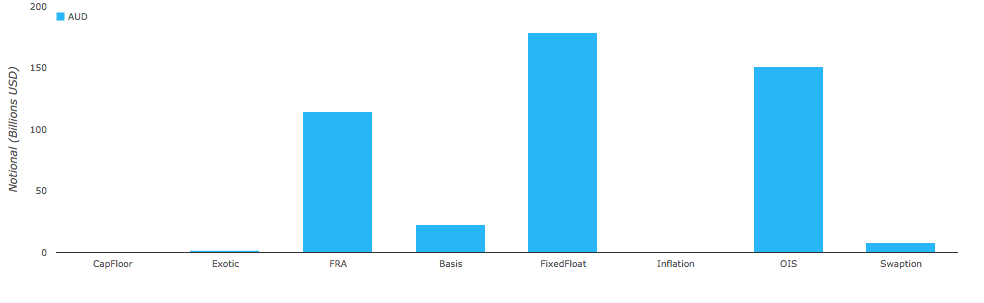

I always focus on Swap markets (with the occasional dalliance with FRAs and OIS…), but it is worth noting that AUD markets saw respectable volumes across FRAs, OIS, Swaps, Basis and even Swaptions during October 2014:

One thing I do find surprising is that the Inflation market has not taken off in Australia. Is a zero reading really a fair reflection of this market or some kind of reporting bias – having read a fair bit from ASIC, it’s not clear to me whether all swaps should be reported.

Vanilla Swaps are clearly the volume winner – therefore let’s dig a little deeper and look at what type of swaps are trading in the AUD market:

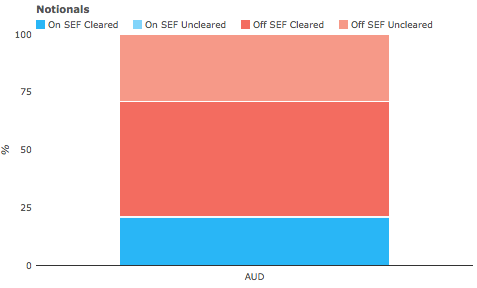

It is hardly surprising that the vast majority of swaps that trade On-SEF are spot starting, but the very high percentage of Fwds is just as notable as in other currencies. However, it’s interesting to see the uptake in MAC swaps – are we seeing one of the smaller markets lead the way in how swaps markets may evolve over the coming months? In theory, the AUD market is extremely concentrated amongst the big four local banks, therefore being able to hedge the bulk of their duration risk with market standard trades appears to be attractive to them. And will undoubtedly help in compression efforts.

To SEF or Not to SEF?

Remember that AUD is not one of the “super-currencies”, therefore there are no clearing or execution mandates in place for US persons under Dodd Frank. No market participant is required by law to transact on-SEF. However, market behaviour shows a decent take-up of on-SEF trading. Our previous chart already showed that nearly 50% of spot starting, cleared swaps were traded on-SEF during October 2014. We can also see that, across the whole market (cleared and uncleared), that nearly 25% of all swaps are traded On-SEF:

Is this take-up down to a reporting bias in the data? Maybe the reporting entities are simply playing it safe and executing on-SEF wherever possible. And is this therefore why the most recent OTC derivatives report from their home regulators reads as more market friendly than from some other jurisdictions? Whatever the reason, it stands out as a success story in the SEF world, where other markets do not see such penetration.

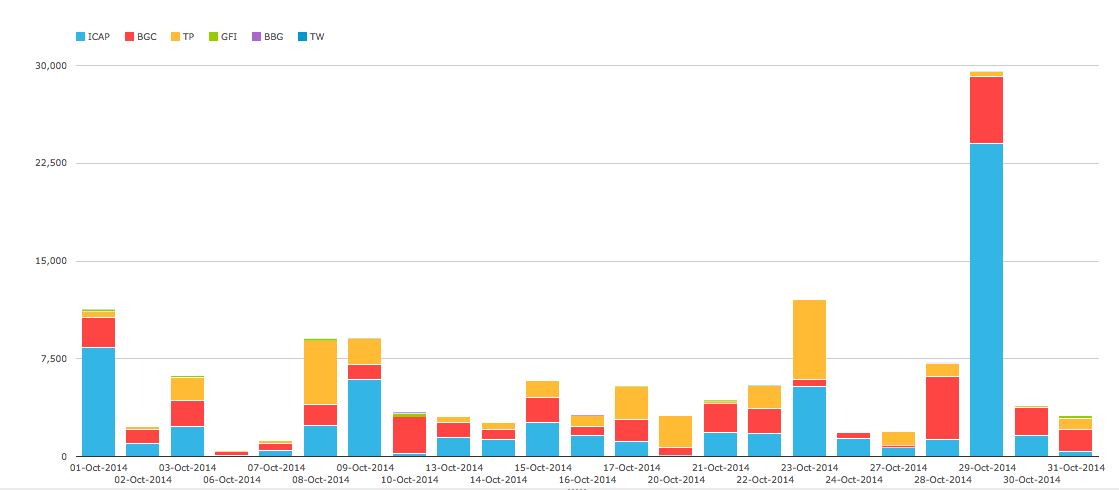

And finally, who is the big winner from these SEF volumes? Certainly not the Dealer-to-Client platforms who have benefited so much in the major currencies. The likes of Bloomberg and Tradeweb barely register with any AUD SEF volumes. Even the IDB market is hugely skewed towards one major player. Whilst BSEF may have had a good October in USD swaps, their market share is nothing compared to what ICAP enjoy in AUD swaps traded on-SEF:

I will leave it to Clarus users to see whether ICAP’s large market-share was down to the launch of “i-Swap” for AUD swaps back in April of this year, or whether they have always enjoyed such dominance.

Summary

So there you have it. A five minute distillation of the AUD swaps market. Hopefully I can find the ICAP office if I need to trade anything whilst I’m over here. I presume it’s near the beach….