With the referendum just around the corner, it would be amiss if we did not update our analysis of EUR/GBP and GBP/USD FX Options ahead of the vote. We also take a look at GBP FRA activity, particularly the FRA switch over the 24th June.

EUR/GBP and GBP/USD activity

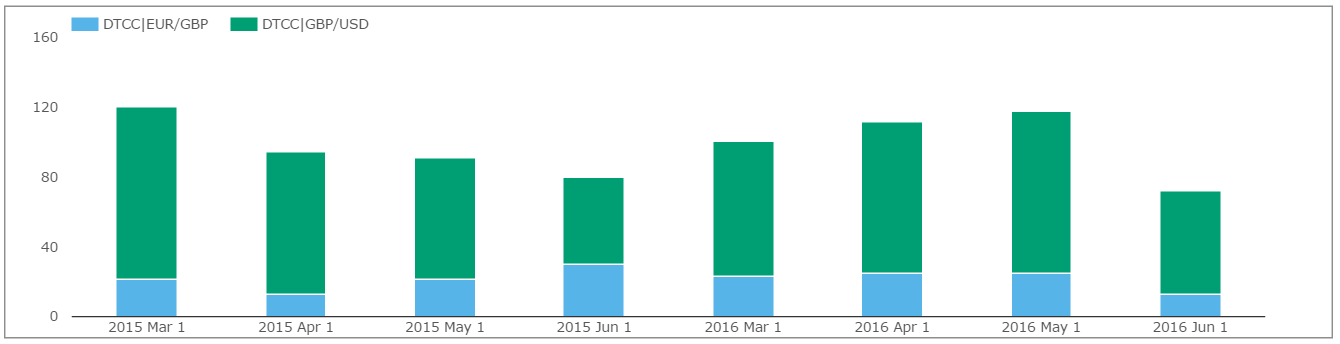

From SDRView Res, we can compare activity since our last blog (back in March) with the same period in 2015.

Showing;

- Average monthly volumes between March and May 2016 of $110bn (~$5bn per day) vs $102bn in 2015.

- However, volumes in June 2016 are running at more elevated levels, with $72bn already trading in the first 16 days, compared to just $79.7bn for the whole month last year.

- So the story is fairly consistent with our last blog – activity has hardly exploded higher, but it is between 5 and 10% higher than last year.

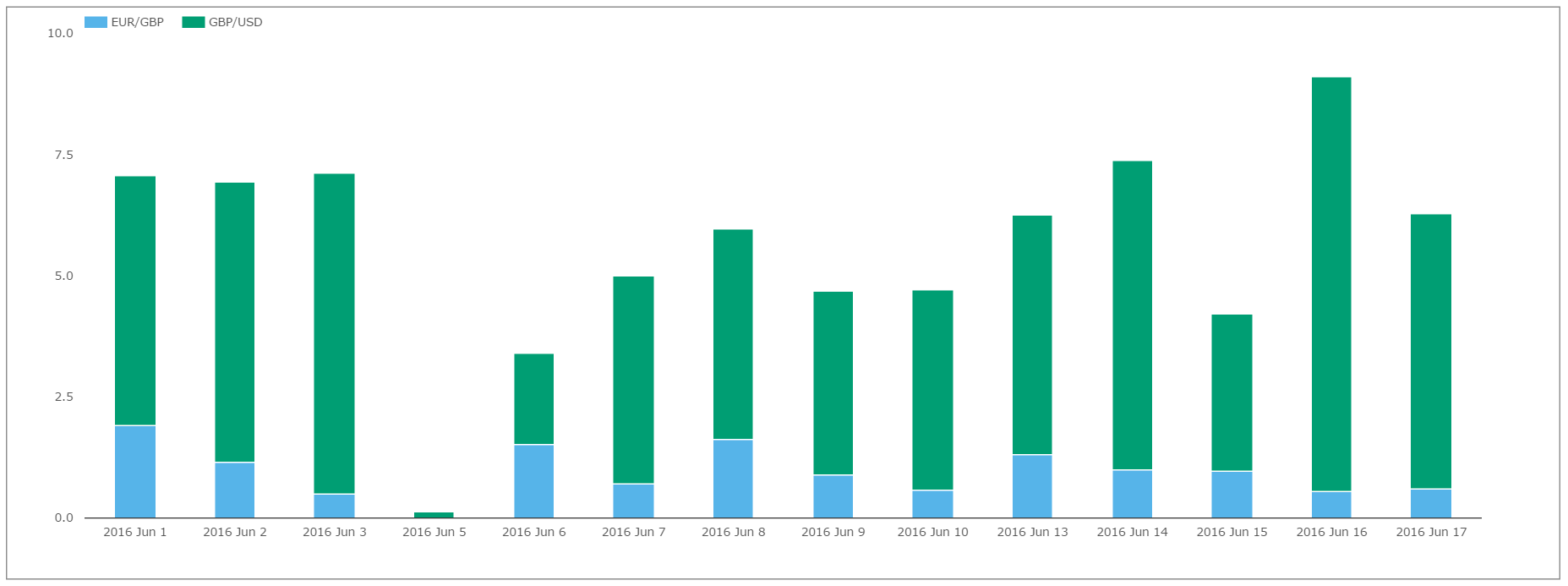

We can also look at the daily volumes this month. So far, Thursday June 16th has been the most active day, which tailed off slightly on Friday. I guess we will see a gradual reduction in trading as the digital event itself approaches this week?

Relative Volumes

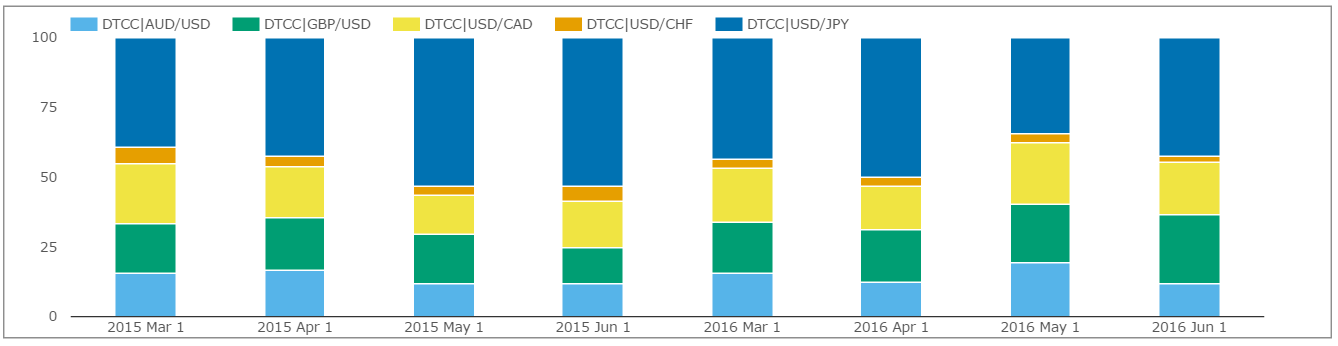

Let’s now take a look at GBP/USD activity relative to other currency pairs:

Showing;

- The contribution of each currency pair to overall activity as a percentage share of notional.

- GBP/USD normally accounts for up to 18% of activity, whilst USD/JPY can see a market share as high as 53%.

- However, in June 2016, GBP/USD has a much higher market share than normal.

- GBP/USD currently commands a 25% market share.

- USD/CHF has seen a drop in activity – maybe due to perceived increased SNB activity depressing realised volatility?

GBP/USD Detail

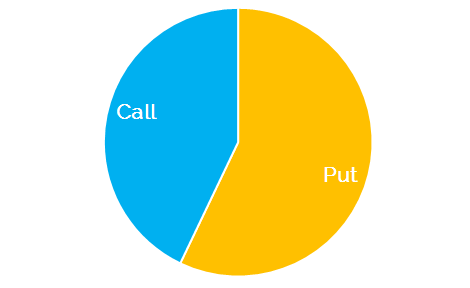

Activity is only somewhat elevated compared to normal levels. Nevertheless, it’s still interesting to look at what has traded. For example, the volume of Puts traded has exceeded that of Calls by 57% to 43% since March 2016 (see chart to the right).

Maybe this offers evidence of a preference towards buying insurance against a Brexit, rather than positioning to benefit from Bremain?

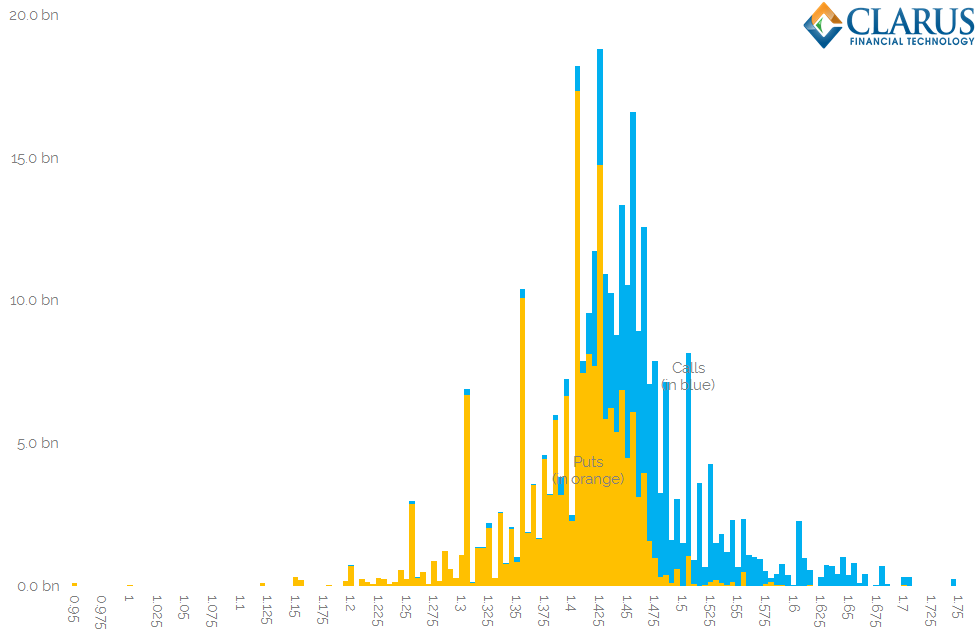

Certainly, when we look at the strikes that have traded, the tail on the downside is much longer than on the upside:

Showing;

- The volume of GBP/USD vanilla options written in half big figure increments since March 2016.

- We see Puts trading all the way down to 0.95 (i.e. below parity with the dollar).

- Whilst this single trade is an outlier (or an inverted strike?), we do see consistent activity all the way down to 1.20.

- Whilst on the upside, there is some activity between 1.675-1.75, but it mainly peters out after 1.60.

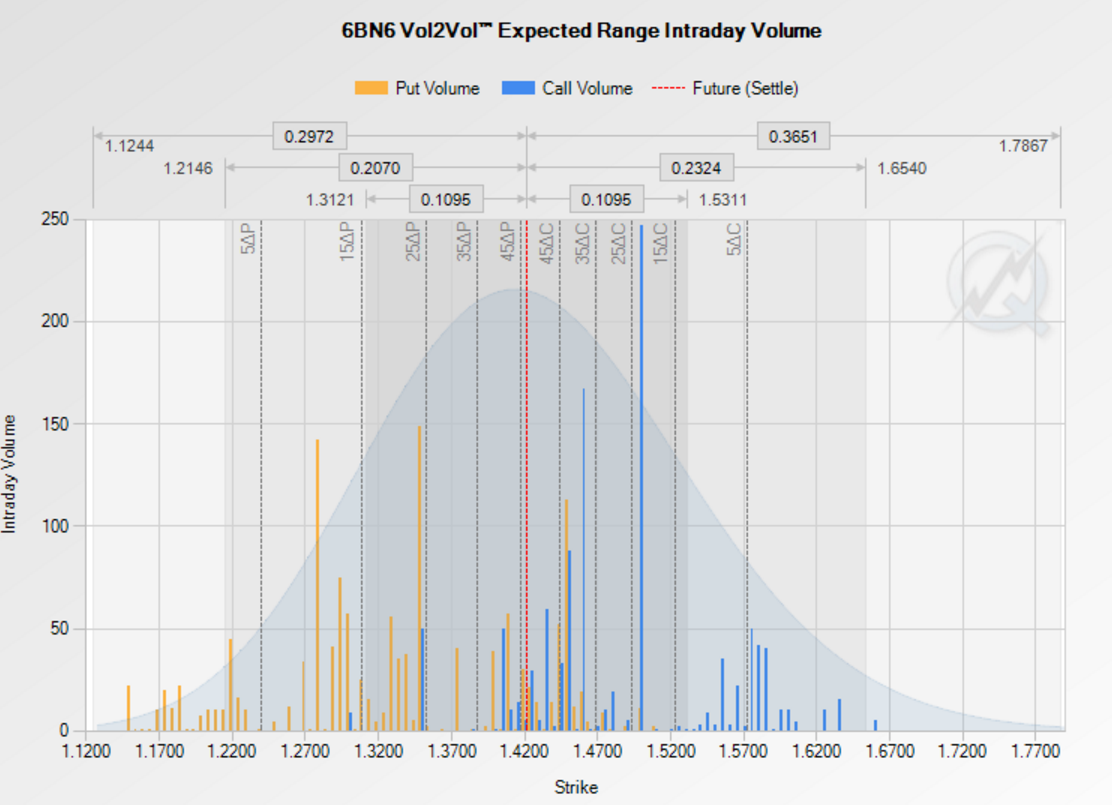

- Unsurprisingly, this is consistent with the CME’s Vol2Vol monitor for their GBP/USD options as well:

And what about the Rates Market?

The best measure of event risk related to the referendum in the Rates market is the value of the FRA-switch over the 24th June. This FRA switch involves buying (selling) a FRA that fixes before the referendum versus selling (buying) a FRA that fixes afterwards.

Assuming a result is declared by 11am London on Friday, the 24th June fixing will be the first Libor fixing after the result is known.

In terms of volumes this month, FRA trading has been running at fairly normal levels in June (an average daily volume of £11.6bn versus a 2016 average daily volume of £10.6bn before June).

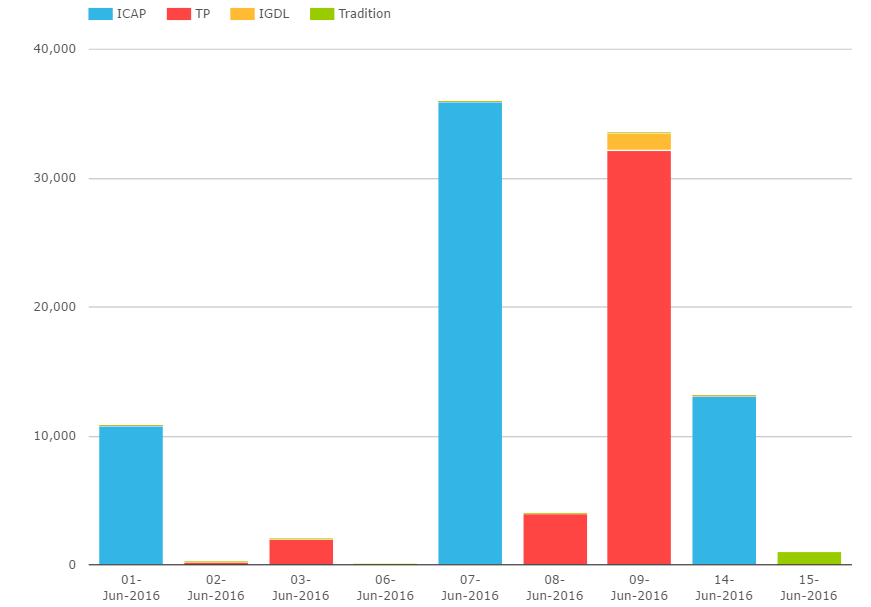

As we’ve looked at before, FRA trading is concentrated in portfolio management exercises run by ICAP and Tulletts. These are mid-market auctions that maximise possible volumes by matching offsetting interests across the market. We can see from a daily time-series of volumes in June that there have been 4 sessions so far this month:

Showing;

- From SEFView, the volume of all GBP FRAs that traded on-SEF this month.

- We can see that ICAP have run FRA matching sessions in GBP on the 1st, 7th and 14th. That would suggest another one is due tomorrow (21st June) – is that the last chance saloon for FRA hedging activity?

- Tulletts had a large session on the 9th June.

- We can use both SDRView and SEFView to analyse the prices of FRAs traded in these sessions.

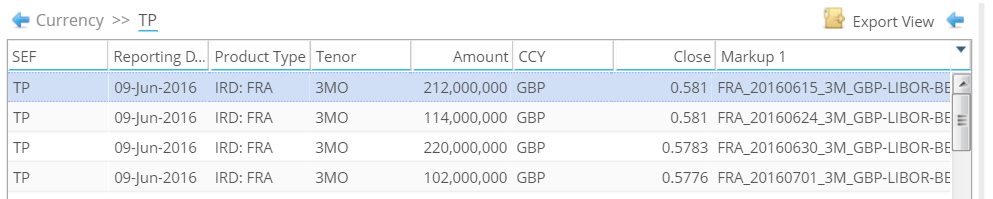

Analysing the prices in SEFView, we see that during the “TP-Match” (Tulletts) FRA matching session, the FRA fixing 15th June was matched vs the 24th June:

Showing;

- A FRA fixing 15th June at 0.581 in GBP212m

- And a FRA fixing 24th June at 0.581 in GBP114m

- This implies there is no event risk priced into FRA markets for the referendum – the market is not pricing in any impact on Libor fixings.

Via SDRView, we can see a similar thing happened during the ICAP FRA matching session on the 7th June. FRAs fixing on both the 15th and 17th June were matched at just a -0.1bp price differential to FRAs fixing on the 24th June:

Overall, from the evidence within FRA trading data, the market does not expect a “digital event”. Virtually no re-pricing of Libor fixings is expected to occur after the Referendum result is known.

Now, there are two schools of thought when interpreting this data. One is that Libor won’t move in the event of a “Remain” result, and this is what the market expects.

The second is more worrying. In the event of a “Leave” result, contagion could cause credit concerns to balloon and Libor to fix higher – irrespective of BoE (and ECB!) rate cuts/stabilisation efforts.

Given the very high levels of vol in FX Options around the referendum, it seems strange that FRA markets would not have some concerns around this date.

Does it give any colour to the polls?

From this brief analysis of FX Options and FRA activity, we can see that:

- Activity levels across both FX Options and Rates are not at “panic” levels. There is more trading going on than usual, but it is not frantic.

- There is greater activity on the downside in FX Options, seemingly protecting against a slide in GBP/USD.

The first point is worth a caveat. With the extreme levels of vol at the moment, it’s a miracle there is any activity at all in FX Options. Bid-offers are wide, and the price of volatility is at historically significant levels.

The second point is maybe not a surprise. Project Fear or not, there are surely a multitude more ways that market participants could get burned through Brexit (e.g. contagion fears) than could profit from a Bremain result?

I personally can’t believe that Libor won’t move in the event of a “Leave” result. So if you really need some type of insurance against Brexit, selling short-dated GBP FRAs is a nice cheap option. However, it is cheap for a reason, as contagion fears in the event of Brexit may quell the effectiveness of the hedge. I would personally put my faith in Central Banks to provide enough liquidity to make sure the hedge pays off.