Using Client Open Interest figures we can project the share of CCP portfolio risk due to Clients once Clearing reaches a mature state. This will take several years as legacy non-cleared Rates portfolios (which dominate global notional outstanding) need to run off and be replaced by cleared trades under the US, EU and Asia client clearing mandates. However, at that time, the implications will be interesting.

What do we mean by CCP portfolio risk?

We all know that notional is not risk nor is it usually a worthwhile proxy for risk. When we talk about a Rates CCP portfolio the main metric used is DV01 or Interest Rate Sensitivities or Deltas. The products are largely linear and so “risk” breaks down into a matrix of DV01s across currencies and tenor points and indices. So risk is not a single variable but a matrix.

Nevertheless, it’s convenient to discuss risk as if it were a single variable that can easily be measured so that we can discuss reducing or increasing risk. Very often this works because when we say reduce risk we mean reduce risk at each node in the matrix or in the sense of reducing the impact of risk on variables like initial margin and capital. It’s convenient shorthand in either case.

Unfortunately there’s no reliable uniform source of portfolio risk for cleared portfolios and even reasonable proxy metrics like net DV01 across currency (sorry quants! I know this doesn’t properly represent cross-currency correlations) or CCP portfolio initial margin (better) or EAD under SA-CCR are all hard to get hold of – even for regulators, let alone you and I! The CCPs have some figures but these are not published except piecemeal to members. The members know their own portfolios but not those of other members. The regulators have not collected them centrally despite trade reporting regulations.

However, the verbal simplification works nonetheless. What is important is that when we say risk we mean it in the sense of being unmitigated by margin.

In addition based on the specific set up of clearing I think we can make a meaningful argument using a couple of simplified models of clearing and some carefully adjusted notional information which is publicly available.

What do we mean by client and member portfolios?

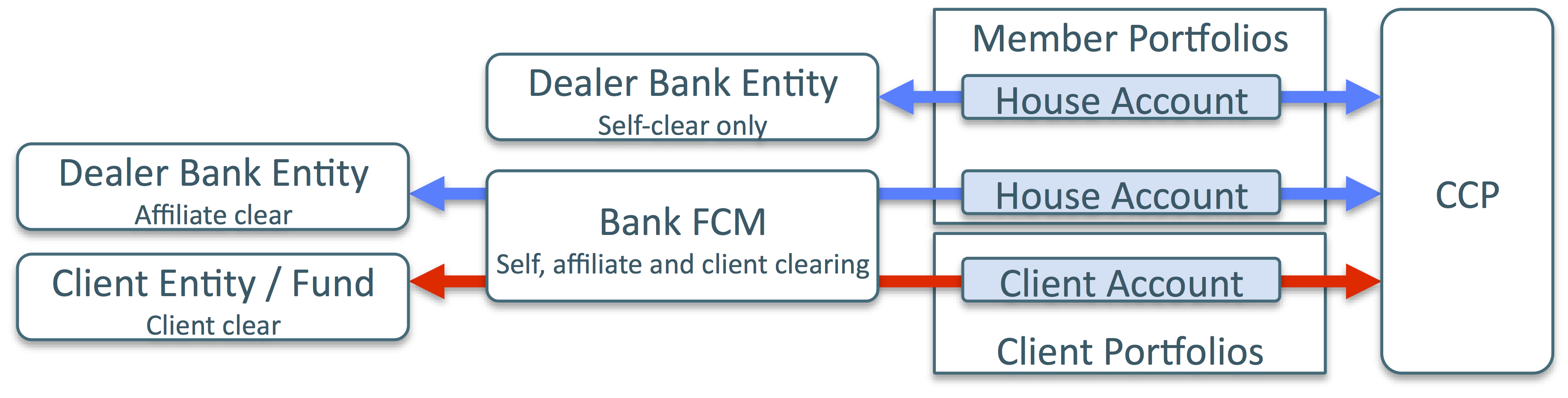

For this piece I want to distinguish client CCP portfolios from member CCP portfolios. This will form a basis for discussion of the risk inherent in these two different types of portfolio. The two cases are illustrated in the diagram below.

“Client portfolios” are the accumulation of the trades (red arrow) of a client entity or fund cleared via a clearing broker or FCM in their client account at the CCP

“Client portfolios” are the accumulation of the trades (red arrow) of a client entity or fund cleared via a clearing broker or FCM in their client account at the CCP

“Member portfolios” are the accumulation of the trades (blue arrows) of a dealer bank entity cleared via either it’s own house account (it is a direct member) or that of an affiliated clearing broker or FCM (it is not a direct member).

So now let’s see what general statements we can make.

A. Member portfolios will always dominate CCP notional outstanding

We know that member portfolios dominate notional today since clients only got going recently whereas members have been clearing for more than a decade. I believe though that this will always be the case. To see this it helps to make a few simplifying assumptions and model things simply:

- Dealers are the only market makers (every client trade is with a dealer / no client market making or client-to-client trading)

- Dealers are the only clearing members and FCMs (no dealer uses client clearing)

- Each client trade results in a side in the client CCP portfolio and a side in the member CCP portfolio

- Each dealer trade results in two sides in member CCP portfolios (top two blue trades in the diagram below)

- Each client trade is hedged by one dealer trade on average (red trade and last blue trade in the diagram below)

So each client trade results in four trades in total of which three are in member portfolios and one in a client portfolio (see diagram below). It follows that in a mature state we would expect cleared portfolio outstanding notional will be split roughly 25%:75% client vs. member.

The real world is not so simple, especially on point 5 – macro portfolio hedging with ongoing hedge adjustments is the norm (i.e. macro hedging involves fewer trades than one per client trade but hedge adjustments happen every day). In addition there is prop trading (more dealer trades) and clearing of hedges of exempt client trades (more dealer trades). Also some clients trade more like market makers or a hybrid of a market maker and a buy side firm (banks which use client clearing to avoid CCP membership, hedge funds / independent broker dealers which intend to expand market making). For now let’s assume these effects balance out in mature state and that volumes fit the split 25%:75% as above.

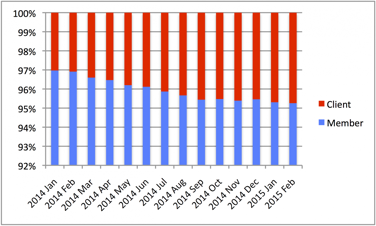

Today we can observe the split is approximately 5%:95% (see table below).

Global Rates CCP Uncompressed** Notional Outstanding by Portfolio Ownership (% share)

(Source: CCPView, SwapClear website)

Notes: The scale is from 92% – 100% ** “Uncompressed” refers to the fact that I have added back in CCP compressed notional given that compression doesn’t impact actual risk but is largely focused on member portfolios and therefore would distort the split to the extent we use the split as a proxy for risk.

So we expect an increase of approximately 5x in client share of notional over today (25% vs. 5%). A large increase is intuitive given EU and Asia client clearing mandates are not yet live and Rates portfolios have a typical half life of 5-7 years vs. 1.5 years so far of the US mandate.

B. Client portfolios are much higher risk per notional than member portfolios

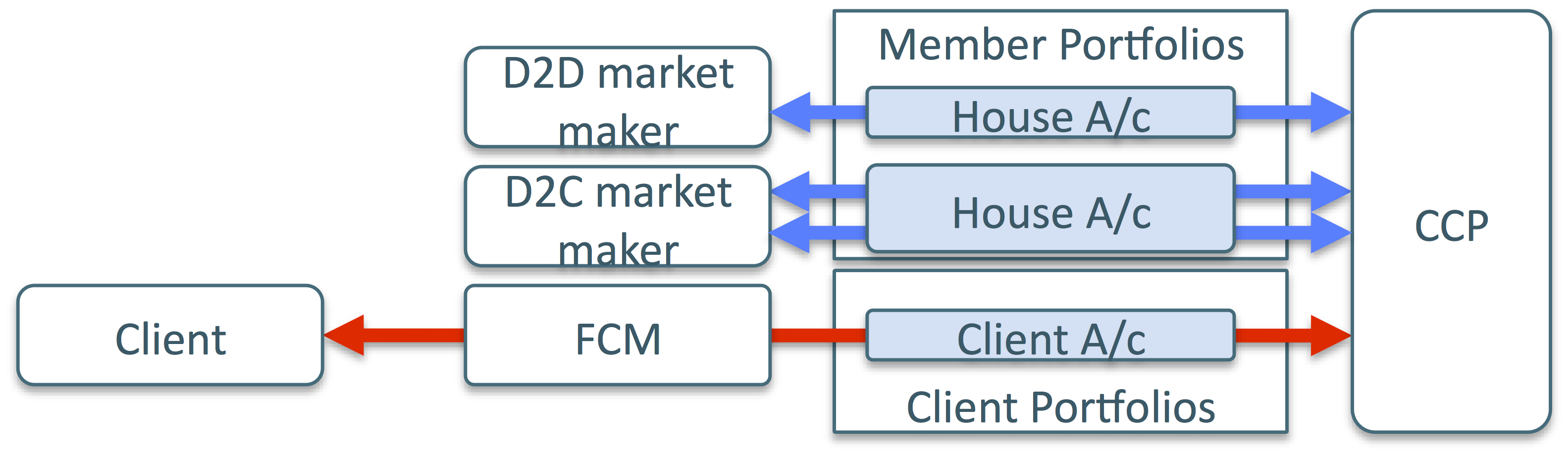

Firstly clients are higher risk per notional simply because in our basic flow trading model the market makers usually hedge the trade. If we extend the above flow model slightly by using an example where a trade makes the client long 3 DV01 from $1 of notional

- The D2C market maker is hedged and so has zero DV01 on $2 of notional (2 trades).

- The D2D market maker who hedged is short 3 DV01 on $1 of notional.

- In aggregate, clients as a whole have 3 DV01 per $1 of notional and members as a whole have 1 DV01 per $1 of notional

So far then, clients are 3x more risk per notional than members.

Secondly it’s easy to believe client portfolio (uncompressed) risk per notional (RPN) will be higher still given:

- Much greater portfolio fragmentation: There are tens of thousands of clients at fund level vs. hundreds of members / dealer entities

- Greater inherent directionality: Clients are either hedging non-OTC risks or taking OTC risk positions. Most member trades are flow trades in which case they will actively hedge out risk. Even the un-offset dealer hedges of client trades with mandate exempt clients will be partly optimized away by offsetting against other trades and will shrink in proportion as the mandates expand to EU and Asia.

- Basel III dealer incentives: Banks have much more to gain than clients from reducing their own CCP risk to lower self-clearing RWA and default fund capital

From experience combined with anecdotal evidence, I would like to propose a conservative range of multipliers on average of 5x – 15x for purpose of discussion.

C. At maturity client portfolios will dominate CCP portfolio risk

This perhaps counter-intuitive view can be reached by combining the first two points.

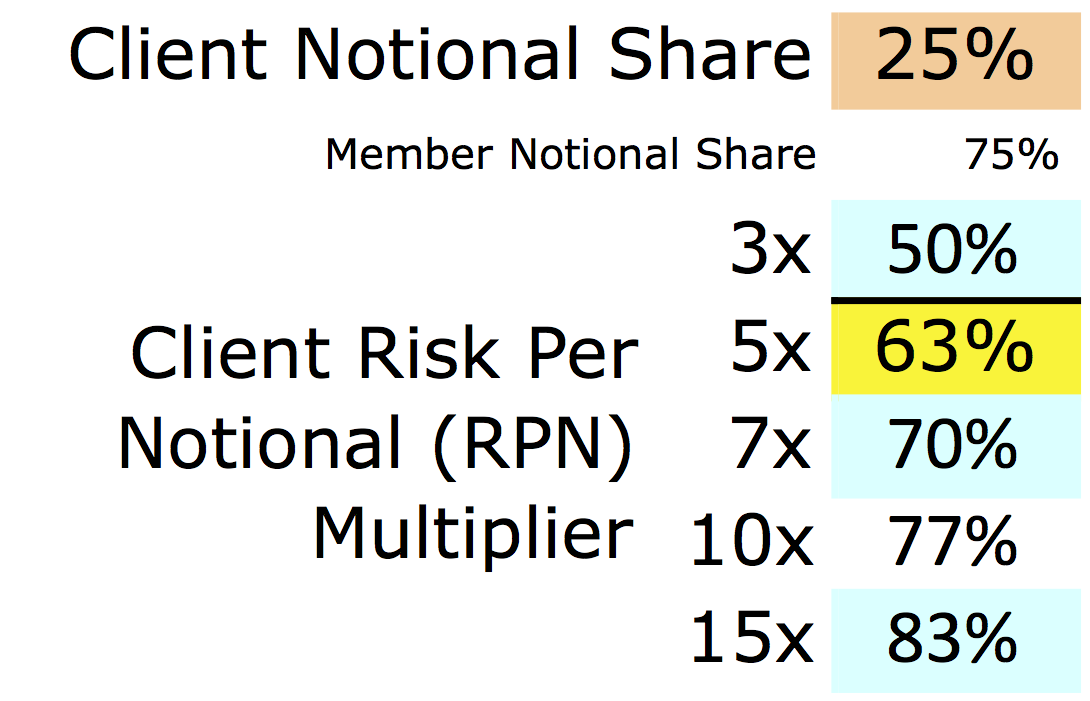

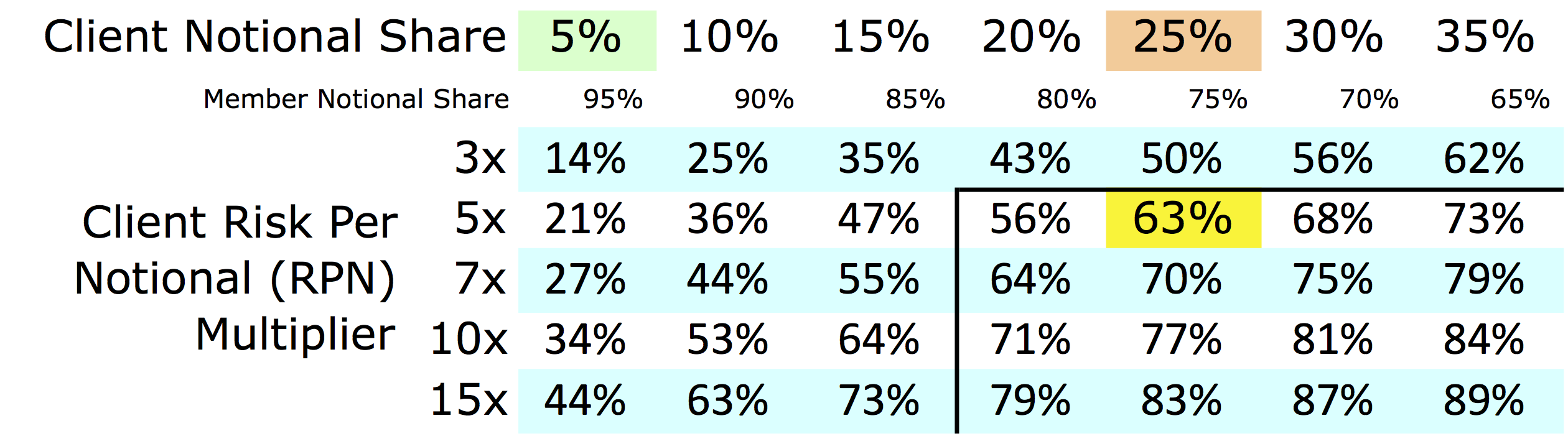

Let’s apply the 5x risk per notional multiplier to our 25% client notional share. We multiply 25% x 5 = 125% to give us 125% vs. 75% and then rebase to 100% (by halving both numbers). This gives us a client risk share of 63%. Repeating the same process for 3x, 10x and 15x we get the numbers below.

The interpretation: client risk will be at least 63% of CCP risk if we are right in our input assumptions.

Client CCP Risk Share by Multipliers of Client Relative Risk Per Notional

(Note: client notional share 25%, client risk per notional at least 3x, uncompressed notional)

But what if we’re not right in our input assumptions? We can look at a range of client uncompressed notional share (see below). Given we are at about 5% today it can surely only go higher. The D2D hedge trades are already cleared typically. So each new client trade comes with only one dealer trade – shifting the balance towards 25%. You can form your own view and see the effect using the grid below. Personally I can’t get comfortable below 5x risk per notional or below 20% notional share so my view is we’re in the bottom right quadrant outlined by the black line somewhere.

In other words it’s highly likely that at maturity client portfolios will dominate CCP portfolio risk.

Client CCP Risk Share Indicated by Notional Share and Multipliers of Client Relative Risk Per Notional

(Note: client notional share at least today’s 5%, client risk per notional at least 3x, uncompressed notional)

Summary

Using uncompressed notional allows us to skirt complications which do not materially affect risk.

Today clients are at approximately 5% uncompressed CCP notional share.

The inherent mechanics of flow trading puts clients at 25% uncompressed notional share and 3x risk per notional implying a significant relative increase in future of client notional share.

Additionally, clients are inherently more directional and fragmented than dealers / members and dealer flow books are usually inclined to hedge market risk and also have much greater combined regulatory, funding and capital incentives to reduce CCP portfolio risk than clients because of Basel III and Dodd-Frank Volcker Rule.

Hence we conclude that 5x-15x is a conservatively low estimate range for eventual client risk per notional multiplier over member risk per notional.

Combining these two factors together gives a high likelihood that at maturity client portfolios will be 63% or more of CCP portfolio risk.

In future I hope to look at the implications of this.

This article is authored by Jon Skinner.