Ten years after the Great Financial Crisis of 2008, we may interpret figures such as only 18% of new trades in OTC interest rate derivatives are now uncleared, to mean that uncleared derivatives now represent a small amount of counterparty risk. However as I will show in this article, this is not true and there remains some way to go to reduce risk.

Summary

- Uncleared IR derivatives are now only 18% of volume, 24% of outstanding notional (other asset classes are higher)

- Cleared derivatives benefit from multi-lateral netting and are generally linear in risk

- Uncleared derivatives gross-up risk across counterparties and usually contain linear and non-linear risk (gamma/vega)

- So a lot of counterparty risk remains – we estimate two thirds is uncleared and half is uncleared delta alone

- New techniques are emerging to reduce this risk rather than collateralise with IM

- These will need to work alongside the clearing mandates to be effective

Regulatory recap

A key aim of post-2008 G20 consensus to regulate OTC derivatives was to reduce systemic counterparty risk and we are now live with bank capital incentives, trade reporting and clearing mandates. With respect to counterparty risk reduction and mitigation, much is already live and bedded in. Over the next 2-3 years it remains to fine-tune leverage ratio (with SACCR) and add smaller banks and all buy-side firms to uncleared margin rules (UMR 4&5).

Counterparty risk breakdown by product linearity

We can look at the uncleared portfolios by product linearity:

- Linear products (i.e. vanilla swaps) only contain linear risk. These may remain uncleared either because they were traded before the clearing mandate started (e.g. IRS can be 30-50 years) or are not clearing-mandated (e.g. NDFs, FX forwards, single name CDS, commodity swaps) or no clearing is available (e.g. equity swaps).

- Non-linear products (i.e. options/exotic swaps/structured trades) contain both linear risk and non-linear risk. e.g. swaptions contain exposure to the underlying swap as well as the option volatility. Of these only FX options show a recent promise of being materially cleared, so far at LCH ForexClear.

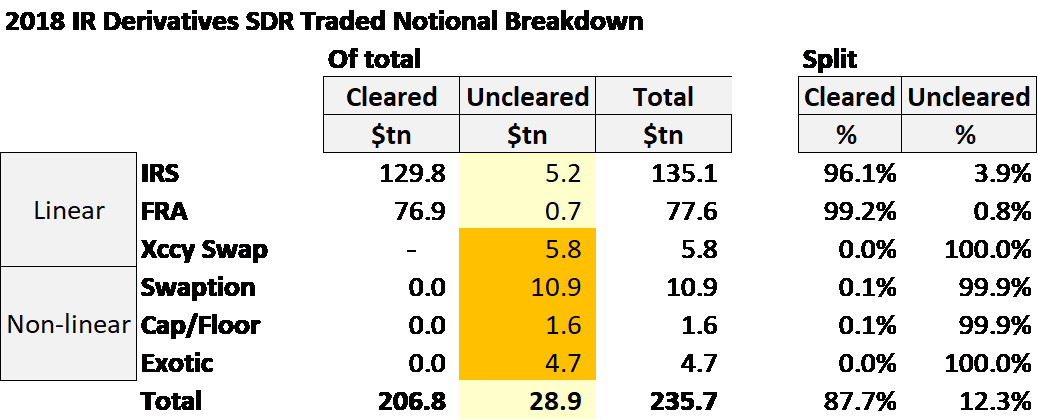

Though traded notional doesn’t equal counterparty risk, we can get a clue to the uncleared portfolio product split from US SDR reported traded notional over a period of time.

Of the uncleared activity, I’ve highlighted in orange that the bulk cannot clear, or in the case of Swaptions is not clearing materially despite CME’s available capability.

Counterparty risk breakdown by risk linearity

We can also look at the portfolios by the risk linearity:

- Non-linear risk (i.e. gamma/vega). For IRD, from above we can interpret that the bulk of this is IRO (interest rate options) volatility risk.

- Linear risk (i.e. delta). There is delta in all products. Non-linear products contain the linear risk of the underlying. Non-IR products contain funding risk i.e. linear IR delta.

Since half the uncleared trades are linear swaps and the other half contains linear risk, it’s pretty clear that delta risk dominates over gamma and vega risk in uncleared risk.

Public information on systemic uncleared counterparty risk

Gross notional volumes of new trades are not a good indicator of counterparty risk. To illustrate we just need to note that I can trade a $100m notional swap and the equal and opposite swap 30 minutes later versus the same counterparty. Now I have zero counterparty risk but $200m traded notional. We need to look at outstanding portfolio net risk denominated in risk metrics such as risk factor sensitivities.

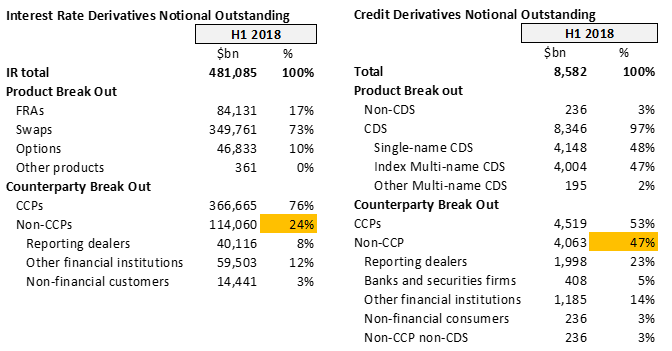

The BIS OTC derivatives outstanding reports (produced half yearly at about 3 months lag) shows global notional outstanding and gross market value. The BIS reports also show the cleared vs uncleared split (with a bit of spreadsheet extrapolation) of the tables: fx/rates/equities and credit/commodities. This results in the figures you sometimes see – the latest for end H1 2018 show uncleared notional outstanding at 24% of rates derivatives and 47% of credit derivatives.

The BIS report also shows gross credit exposure. This shows total gross counterparty portfolio NPV, so not directly a measure of potential future exposure which is the exposure directly related to counterparty portfolio risk factor sensitivities i.e. delta / gamma / vega which derivatives practitioners talk about as “the risk”.

Gross-up effects

Uncleared portfolios are many more in number and likely have much greater fragmentation than cleared portfolios. The ISDA/SIFMA July 2018 study on UMR estimates over 9,000 new UMR-caught relationships for dealers with UMR 5 counterparties.

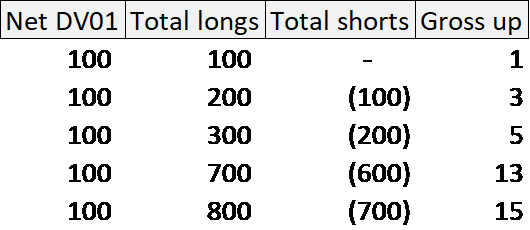

Counterparty risk grosses up compared with net market risk when there is a mixture of long and sort counterparties. If all counterparties are long (or all short) there is no gross up. This might happen for a particular risk factor sensitivity if the trader hedges his market risk position to zero in that risk factor with a trade with one counterparty whilst leaving on the pre-existing trades making up the position prior to hedging. Normally the desk is not fully flat risk however across all risk factors.

For CCP portfolios, given the consolidation of trading and a largely dominant CCP for each asset class it is likely there is not much gross up across CCPs or that this will be quickly optimized away by CCP basis trades. For uncleared portfolios, there are many bilateral counterparties per asset class / risk factor and it is much more likely there’ll be gross up.

Anecdotally the below is a reasonable representation of the range of gross up possibilities.

What can we glean from outstanding notionals?

To summarize what we know:

- Uncleared products are higher risk per notional

- Uncleared portfolios gross up counterparty longs and shorts

- Delta dominates gamma and vega in uncleared portfolios

- Clearing isn’t helping much to reduce this delta

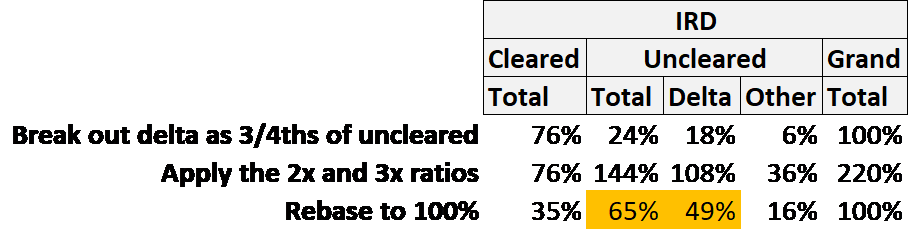

I think it’s conservative to conjecture that uncleared portfolios are 2x risk per notional and 3x counterparty risk gross up vs cleared portfolios. We can assume 3/4 of the uncleared risk is delta.

Putting these together should be self-explanatory in the table below.

This leads to the unscientific but inescapable conclusion that about two-thirds of the gross global OTC interest rate derivatives counterparty risk is uncleared and about half is uncleared IR delta.

We could apply the same approach to other asset classes which all have higher uncleared percentages than interest rate derivatives. These would show higher still uncleared risk fractions. So we can use these results as a conservative estimate for all asset classes.

All of this suggests that this is a lot more to be done to make OTC trading counterparty risk efficient.

What can be done?

Judging by traded and outstanding notional patterns, conventional central clearing approaches (new trade clearing, portfolio backloading) seem close to what’s achievable in reducing uncleared counterparty risk – with the possible exception of FX options.

New counterparty risk optimization techniques are emerging including delta hedged trading, risk compression and delta risk conversion. These actually reduce the gross portfolio counterparty risk as opposed to simply putting up margin under the new UMR rules. The techniques show promise provided they can co-exist with the clearing mandate

I intend to look into these in my next article.