- USD can be funded domestically or in international funding markets.

- These two funding markets create natural links between Libor-OIS spreads and Cross Currency Basis.

- We saw record volumes in USD Libor-OIS trading over the past three months.

- We also saw record notional volumes traded in Cross Currency Basis during Q1 2018.

- However, when we look at the amount of risk traded (in DV01) and the price action, there is no sign of a stable link between these two important funding markets in 2018.

The Theory

Conventional wisdom (as much as it ever applies to basis trading…) states that if USD funding becomes more difficult to get, then Cross Currency Basis should widen – i.e. move more negative. This implies that USD funding is more expensive relative to other currencies. Over the past ten years, this has traditionally meant that:

- Libor-OIS in USD and Cross Currency Basis (particularly in EUR-USD and USD-JPY) have moved in the same direction. That is to say that when Libor-OIS widens (which is “long-term” unsecured USD Libor funding getting more expensive versus overnight funding), then the Cross Currency Basis also widens – i.e. moves more negative, as USD funding collateralised with foreign currency replaces domestic USD funding sources.

- In a RORO World, that meant that “Risk Off” moves in global asset markets would lead to widening USD Libor-OIS and widening cross currency basis.

- The Cross Currency basis as measured by XOIS (USD OIS vs foreign currency OIS) has therefore tended to be more stable/less volatile than the Libor-based equivalent.

The Present

Basis has been a very popular subject this year. We’ve already looked at “All time records in cross currency basis volumes” as well as all time records in Libor-OIS volumes. Of these two observations, the volume increases we’ve seen in Libor-OIS are by far the more significant.

Let’s therefore update our Cross Currency volumes in light of these huge volumes that we continue to see in Libor-OIS basis trading.

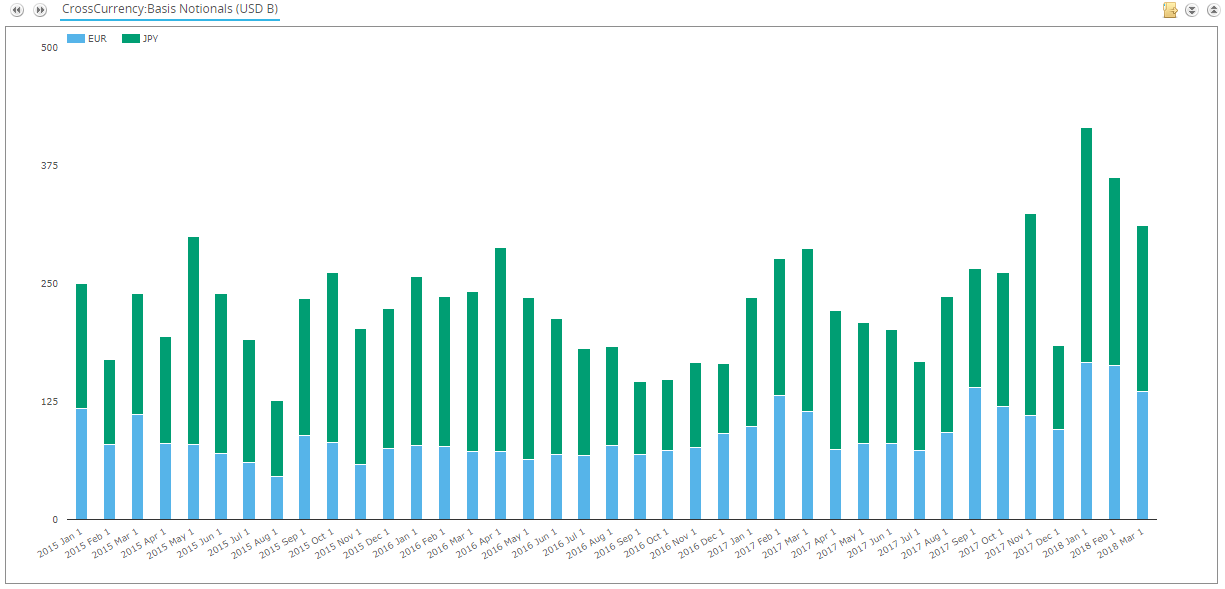

Cross Currency Notional Volume update

The last time we looked at volumes in Cross Currency, the increase in trading activity had been in the short-end. That means that whilst we see record notional volumes, the amount of risk being traded (as measured by DV01) remains short of the peaks we saw back in 2016.

Updating the Notional Amounts traded in EURUSD and JPYUSD from SDRView:

Showing;

- 3 out of the 4 highest ever months in notional terms have occurred in the first 3 months of 2018!

- Notional volumes were massive in January 2018. They have since reduced by about 15% each month.

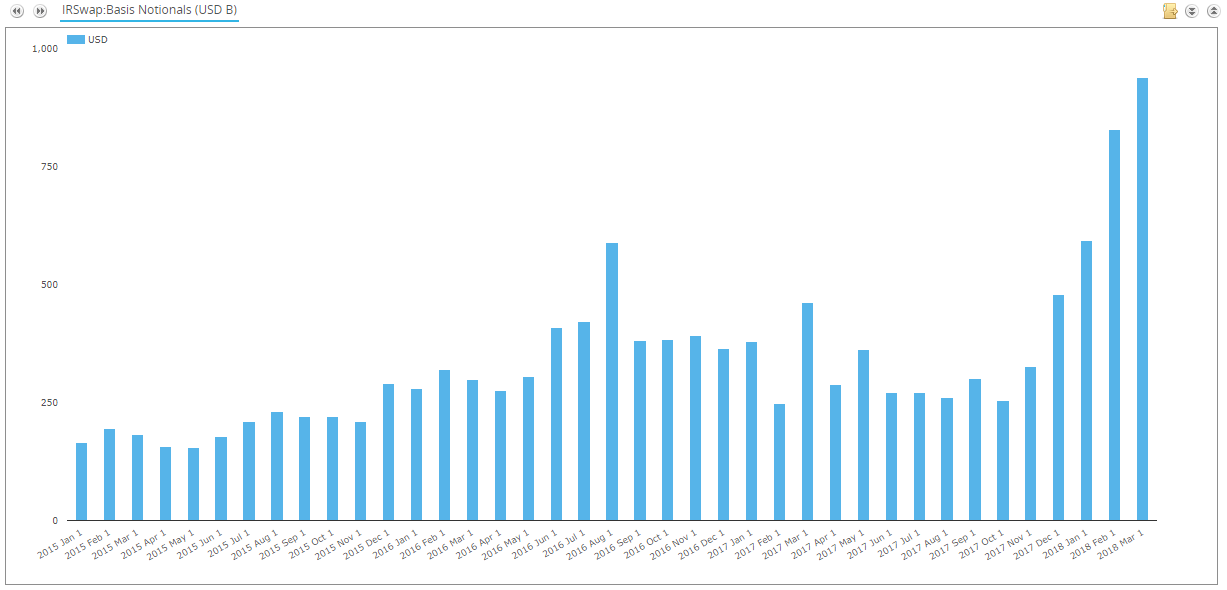

- That is in stark contrast to the volumes trading in USD Libor-OIS which keep on increasing month-on-month:

- March 2018 was the all-time record month for volumes traded in USD Libor-OIS basis.

- March 2018 volumes were 2.9 times larger than the 2017 monthly average.

- Volumes have basically doubled since December.

As we saw last week, this is not just short-end trading in Libor-OIS. Record amounts of risk (as measured by DV01) are trading in the spread. What do we see in Cross Currency Swaps?

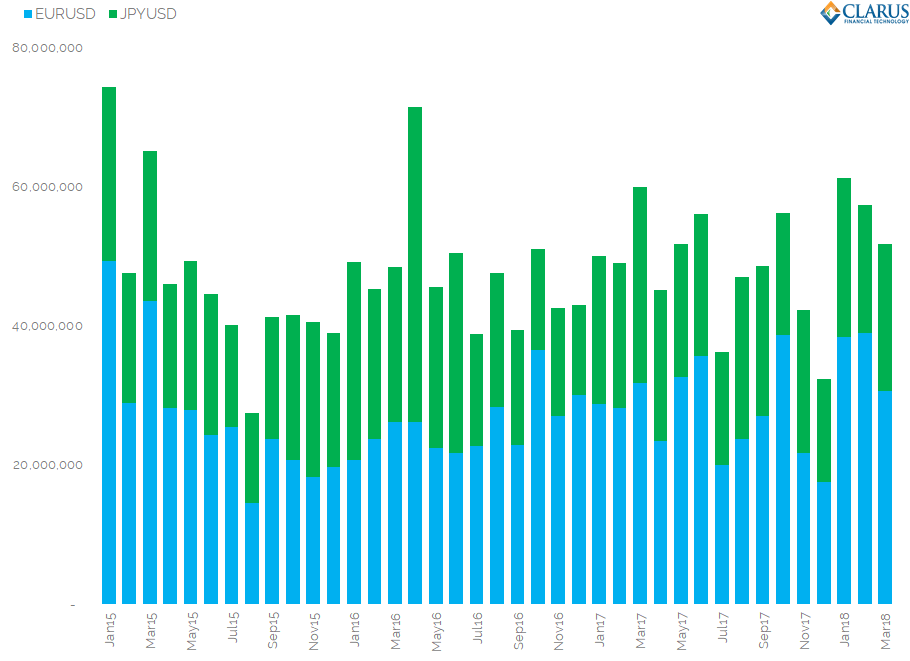

Cross Currency DV01 Volumes

Using our Microservices, I translated the Notional Volumes in Cross Currency basis into DV01 amounts:

Showing;

- As we found previously, the amount of risk being traded in Cross Currency remains below the 2015 and 2016 peaks.

- January 2015 was the month in which most risk traded for these two currency pairs.

- The higher volumes in 2018 are due to increased activity at the short-end of the curves. These are larger notional, but lower risk, trades.

Cross Currency Price Action

Our volume stats suggest that there isn’t much link at the moment between USD Libor-OIS trading (which has volumes at all-time records) and cross currency basis volumes.

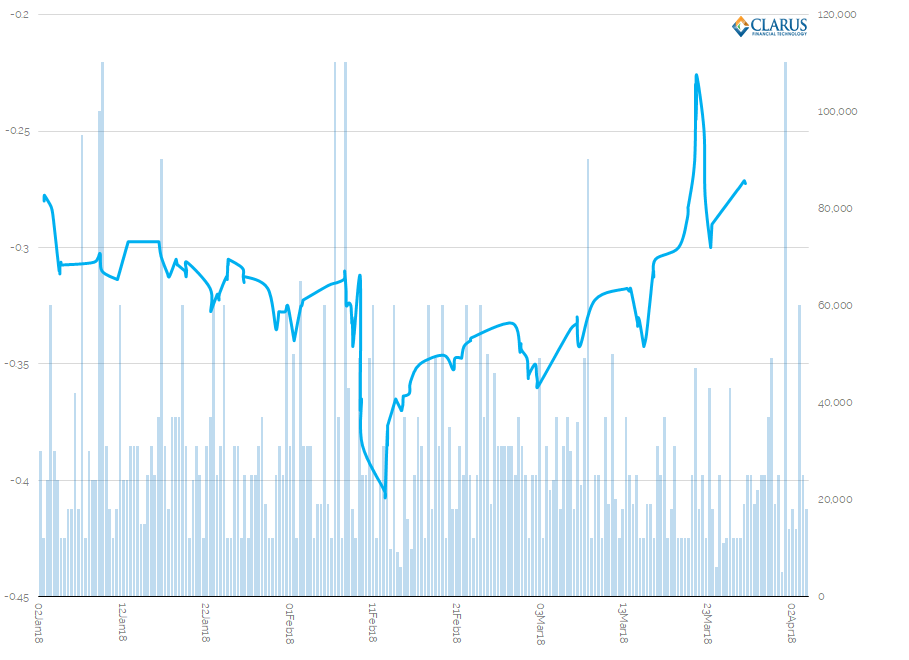

A simple price-volume chart of 1 year EUR-USD also suggests there is little link between their prices at the moment:

Showing;

- 1 year EUR-USD cross currency basis is now higher than where we started the year.

- The lows, below minus 40 basis points, were touched in the middle of February.

- Despite a substantial increase in USD Libor-OIS trading since the middle of February, we have seen the cross currency basis head higher.

- This price action is not only limited to one year. The average basis price across all tenors in 2018 has trended up from -31 in January 2018 to -24 basis points in March 2018.

- This is not reflective of stresses in USD funding markets.

In Summary – Volumes and Prices

The volume and price stories are consistent in 2018:

- Volumes in USD Libor-OIS trading have been huge in 2018 – as measured both by notional and DV01.

- Volumes are not elevated in Cross Currency basis when measured in DV01 terms.

- Even in notional terms, volumes in Cross Currency basis have been falling whilst Libor-OIS volumes have been increasing.

- USD Libor-OIS has widened substantially since the start of the year.

- Cross Currency spreads are now somewhat higher than where we started the year.

- With higher cross currency basis (i.e. less negative/tighter spreads) and no spike in risk-weighted volumes, we can rest assured that USD funding markets are functioning as intended and are largely stress-free.

- USD funding remains accessible, particularly if you can collateralise it with foreign currency.

The intricacies for the move are beyond the scope of our blog. But one explanation has captured wide-spread media coverage, from Zoltan Pozsar at Credit Suisse. For those interested, please see Bloomberg, FTAlphaville and the original research here.

Love your work. Great analysis. Nice that you cite Zoltan’s work also. Beat tax might be an important part of this. Hong Kong dollar and Saudi currency affected by rising Libor.

Thanks Peter, many thanks for reading!