On October 22, the United States published its Final Rules to establish the minimum margin requirements for swaps transacted by insured depository institutions, which are not cleared by a clearing house.

The Joint Rules are the work of the Federal Deposit Insurance Corporation (FDIC), the Office of the Comptroller of the Currency (OCC), the Federal Reserve Board (FRB), the Farm Credit Association (FCA) and the Federal Housing Finance Agency (FHFA) in consultation with the CFTC and SEC.

The press release and full documentation are available here.

Having waded my way thru all 281 pages, at least three times, this is my summary and analysis.

Background

The rules apply to Covered Swap Entities, which are registered with the CFTC or SEC and require the daily collecting and posting of risk-based variation and initial margin for non-cleared swaps.

They are consistent with the international framework proposed by BCBS and IOSCO for Margin Requirements for non-centrally cleared derivatives published in Sep 2013.

Types of Counterparties

Four types of swap counterparties are defined:

- Swap entities

- Financial end-users with material swaps exposure (>$8 billion average daily notional exposure)

- Financial end-users without material exposure

- Non-financial end-users, Sovereigns and Multilateral Development Banks

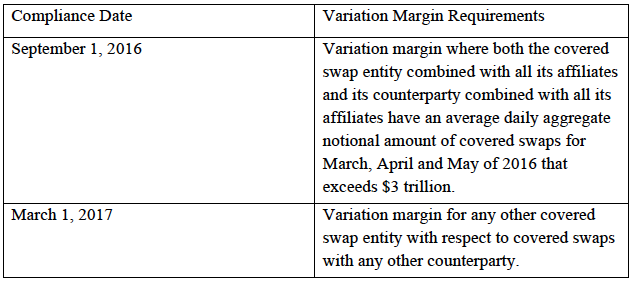

Variation Margin

Covered Swap entities are required to collect or post daily variation margin with a swap entity or financial end-user (so in above list only type 4 is exempt) in an amount that is at least equal to the increase or decrease in the value of the swap since the previous exchange of variation margin.

There is no threshold amount below which variation margin does not need to be collected or posted. Except if the combined initial and variation margin is less than $500,000.

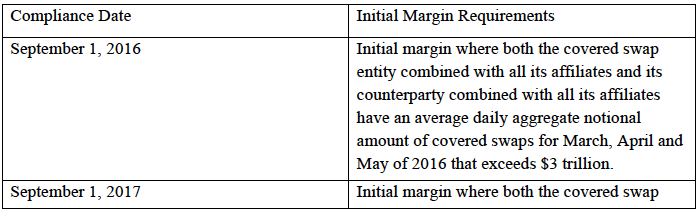

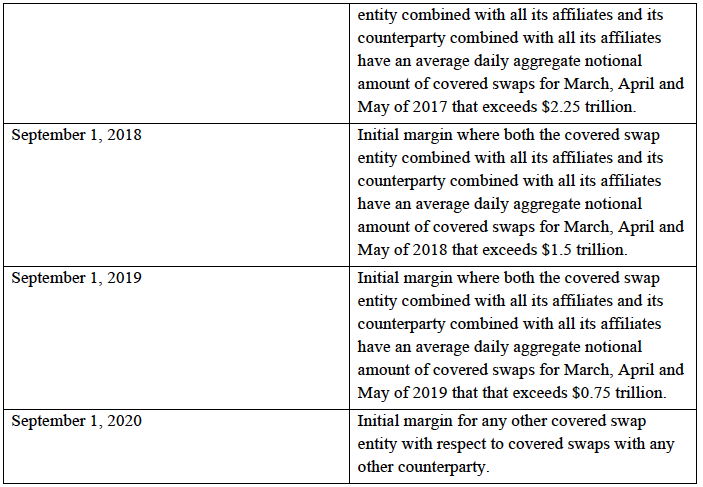

Initial Margin

Initial Margin may be calculated in one of two ways:

- Standardised margin schedule (given in the rule documentation)

- Internal margin model that satisfies specific criteria and has been approved by a prudential regulator

Initial margin must be collected and posted daily by a covered swap entity when its counterparty is a swap entity or a Financial end-user with material exposure.

A maximum threshold of $50 million is allowed, below which it is not necessary to collect or post initial margin.

Collateral

Eligible collateral for variation margin requirements between swap entities is limited to cash funds in US dollars, another major currency or the currency of settlement for the swap. While for financial end users the same forms of collateral as permitted for initial margin are permissable.

Eligible collateral for initial margin includes cash, debt securities issued by the US Government or US Government Agency, BIS, IMF, ECB, Multi-lateral development banks, GSEs, certain foreign government debt securities, certain corporate debt securities, certain listed equities, shares in certain pooled investment vehicles and gold.

Non-cash collateral is subject to haircuts as detailed in the rule documentation e.g. 15% for gold.

A cross-currency haircut of 8% is specified for non-cash collateral denominated in a currency other than the currency of settlement.

Collateral to meet the initial margin requirements collected by a covered swap entity must be segregated and placed with a third-party custodian.

And collateral other than variation margin that it posts to a counterparty must also be segregated at one or more third-party custodians.

Cross-Border

Foreign swaps of foreign covered swap entities are not subject to the margin requirements of the rule, while covered swap entities operating in a foreign jurisdiction and those organised as US branches or agencies of foreign banks, may chose to abide by the requirements of foreign jurisdiction if the Agencies determine these are comparable to the final rule.

Affiliates

A covered swap entity is required to collect margin from its affiliates, however it is not required to post initial margin to its affiliate (that is not also a covered swap entity) but must calculate the amount of initial margin that would be required to be posted and provide such documentation to the affiliate on a daily basis.

Each affiliate may be granted an initial margin threshold of $20 million.

Compliance Dates

The rules will apply to non-cleared swaps entered into on or after the applicable compliance date.

There are separate dates for variation and initial margin with phased compliance.

Netting Agreements

The rule permits the calculation of margin on an aggregate net basis across swaps executed with a counterparty under an Eligible Master Netting Agreement (EMNA). Either sperate netting portfolios can be maintained for new swaps subject to compliance and old swaps not subject to compliance, or an entity can choose to include old pre-compliance swaps in the netting portfolio subject to the final rules.

Standard lnitial Margin Models

The Standard Minimum Initial Margin is a simple method using looking tables of Asset Class and percentage of notional (e.g. 4% for IRS > 5Y) and then a calculation that gives some netting benefit, specified as 0.4 * Gross Margin + 0.6 * Net to Gross Ratio * Gross IM.

Very similar to the standard method for market risk capital.

This method will produce very high margin requirements for a portfolio of swaps and as such it’s use is expected to very limited.

Meaning that approved internal models will definitely be the way to go.

Approved Initial Margin Models

The final rule specifies criteria for these models:

- one-tailed 99% confidence level

- 10-day close-out period (not scaled from 1d)

- must include material non-linear risks

- calibrated to a period of financial stress

- the period to be at least 1 year and not more than 5 years

- the data in the period to be equally weighted

- a product must be assigned to one asset class (fx, ir, cr, cm, eq)

- no risk offset is allowed between asset classes (so sum of each)

- be approved by the entities prudential regulator

- annual review of model and other governance similar to risk-based capital models

And that just about covers the main points.

Approximately 1,100 words.

Much better than reading 281 pages.

Of-course if you really need the full detail, please click here.

Some thoughts

A few jump out at me.

First if both parties are swap entities then they will both need to calculate margin requirements, and for initial margin the calculation is asymmetric as the loss tail is not the same as the profit tail. Meaning for the same portfolio of trades between us, I will calculate how much to collect from my counterparty and they will calculate how much to collect from me and the two will be different even with the exact same data and methodology.

Naturally each party will also want to check the others calculation, using both its own internal model and perhaps also what it knows about the assumptions and data used by the other parties model.

Common utility I hear you say.

But that sounds too much like a clearing house.

A clearing house for non-cleared swaps, an oxymoron I think, though no doubt some will be launched.

But short of an actual and regulated clearing house, would a Swap entity trust an external body to tell it the amount of margin to collect and post?

I doubt it. More likely each Swap entity will calculate what it needs to collect and post, both will be using approved internal models, will disclose details to their counterparty, so we are just left with the need to resolve disputes. Something which will have to be covered under the Master Agreement between the firms.

To calculate the initial margin, firms will most likely leverage their existing in-house or vendor supplied Value-at-Risk systems. Assuming that these are up to the task of handling the new demands.

Many more thoughts come to mind, including ISDA’s proposed Standard Initial Margin Model.

But that is one for another day.

Roll on Sep 2016, Mar 2017, …. , Sep 2020.

Project “Blazer” – a joint approach between DTCC, AcadiaSoft and TriOptima, intends to provide a platform to meet all the requirements of the above rules. And as you point out – Blazer will become your trusted infrastructure to avoid the complication of each party using different models and having unreconciled economic differences between each parties portfolios. NetOTC also have a new service in development which provides an innovation bilateral approach to meeting the requirements. All this will be covered in an article from David Field in the forthcoming edition 5 of Rocket magazine. Bill.