The CME have announced they are planning to clear Korean Won (KRW) and Indian Rupee (INR) interest rate swaps in the near future.

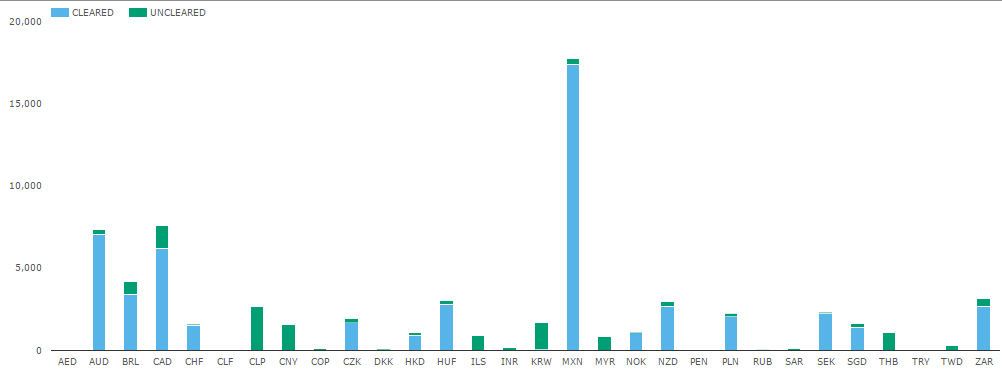

I wanted to have a look at what these markets look like. So first things first, I grabbed all trades for non-G4 swaps on the US SDRs, year-to-date. Did this for both Fixed/Float:

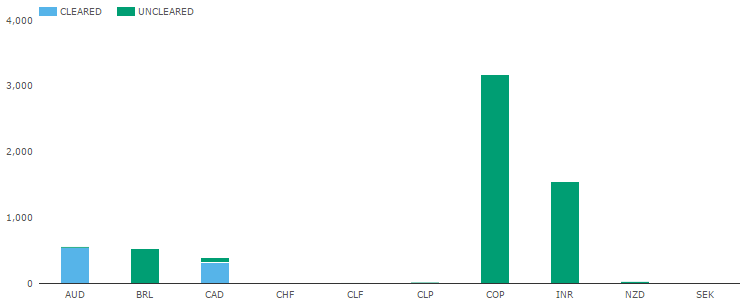

As well as OIS:

Few things jump out here:

- The most active non-G4 ccy on the SDRs is MXN, at about 220 trades/day

- Most fixed/float swaps are cleared (blue), with the exceptions being a handful of currencies that are not yet clearable by US-venues. Those currencies and their approximate ADV:

- CLP – 33 trades / day

- CNY – 20 trades / day

- ILS – 12 trades / day

- KRW – 21 trades / day

- MYR – 11 trades / day

- THB – 14 trades / day

- For OIS swaps, Colombian Peso (COP) tops the list with roughly 40 trades/day, and INR a close second. (20 trades/day).

So, from a trade count perspective, by choosing INR OIS and KRW IRS, CME seem to have chosen some of the more active non-clearable swaps.

Interestingly, the CME seem to say they intend to clear CLP, COP, and CNY perhaps later this year, so they are making their way through them all.

Let’s dig into these swaps.

INR

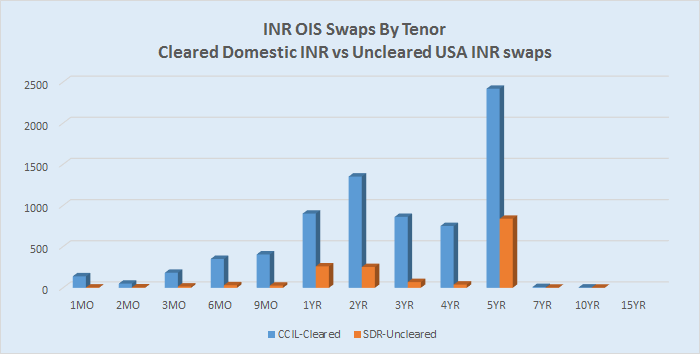

After examining the SDR data, the characteristics of INR swaps seem to be:

- Fixed vs Floating MIBOR OIS

- Predominantly pay/receive semi-annually. Though there are a handful of zero-coupon 5yr swaps in the data set.

- Average trade size about 3bn INR (or about $45 million)

- More than half of the INR swaps are 5Yr, and nothing past 10 year.

More on that last point. We also have data from local Indian clearing house CCIL for these OIS swaps. So if I take both SDRView data for bilateral INR swaps, and combine with CCPView data for cleared onshore (Indian) INR swaps, the maturity profiles look similar. Once again, nothing past 10 years.

KRW

Pulling KRW data, we find:

- Fixed vs Floating KRW CD-KSDA Index

- All resets and payments are 3M

- Average trade size about 64 billion KRW (or about $56 million)

- Active tenors are 2, 3, 5, and 10, but with activity up to 25 years.

NON DELIVERABLE

And of course, the CME will treat the settlements from these swaps as non-deliverable, so they will use local FX fixings to convert KRW and INR to USD.

JUSTIFICATION

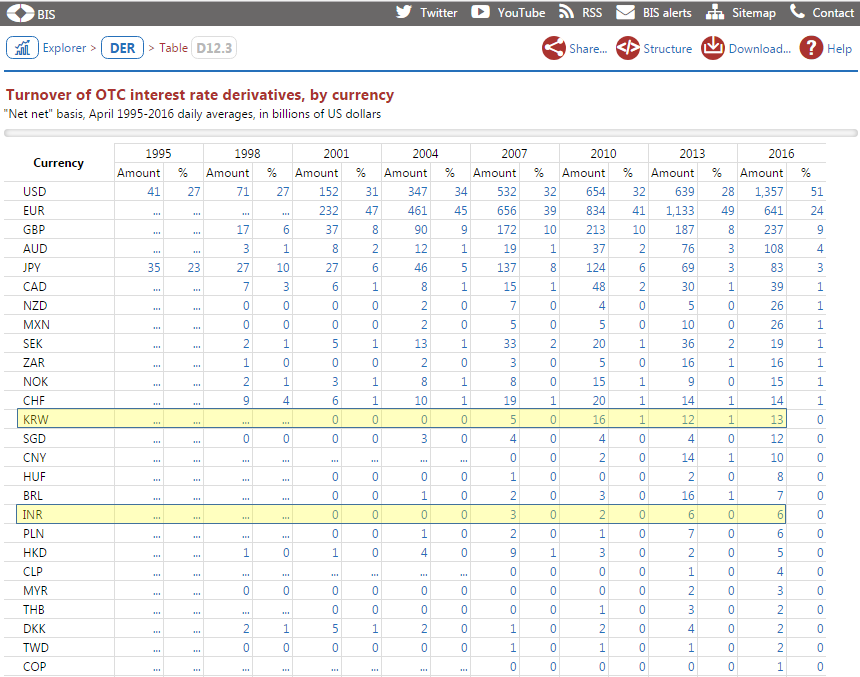

So it seems we see, on the US SDRs alone, about 40+ trades per day in these swaps, totalling about $2 billion notional per day. Not a heck of a lot, but viable. I thought I’d pull BIS data to see if we could get a global perspective. Here is the BIS table from the 2016 Triennial survey:

Which tells us:

- Total Single-counted KRW daily notional volume in April 2016 was US $13 bn.

- Total Single-counted INR daily notional volume in April 2016 was US $9 bn.

- Generally about 10x what we see on US SDR. That seems believable.

BENEFITS TO USERS

Of course, now that we live in the world of uncleared margin rules (UMR), banks should be incentivised to reduce their number of counterparties, presumably to central counterparties.

While we don’t know (yet) how large the CME Initial Margin will be for KRW and INR swaps, we do know that all phase 1 banks need to support these swaps with SIMM margin. I wont go into any more detail than we’ve done in various blogs on this topic – but I do want to point out that the risk weights used for the delta component in SIMM places KRW in the same risk-weight table as USD (“Regular Volatility”), while INR would fall in the “High Volatility” table, which is generally 2x the size of “Regular”.

SUMMARY

- CME Is due to launch clearing for both KRW and INR swaps.

- Both are non-deliverable currencies, like BRL swaps, so will fix to, and settle in USD

- We are able to find about 10% of the global data on the US SDRs

- INR OIS trade off of MIBOR index and are <= 5yr

- KRW IRS trade off of a 3M domestic CD index and are primarily up through 10 years.

We will of course keep an eye on things as it rolls out.