This week, we go south of the border to look at Latin American Interest rate swaps.

Over the past few years we have looked at MXN (Mexican Peso) and BRL (Brazilian Real) swaps in some detail, particularly around their launch of clearing:

- Sizing the MXN Swaps Market (Dec 2013)

- A Year of MXN Swaps data post-CME clearing (Dec 2014)

- Defining and Sizing the BRL IR Swap Market (Aug 2015)

- April 2016 Mandatory Clearing in Mexico (Jun 2016)

Its been a while since we’ve looked at any progress here, so lets catch up on BRL and MXN, and take the opportunity to look at other Latam currencies as well.

Swap Types and Currencies

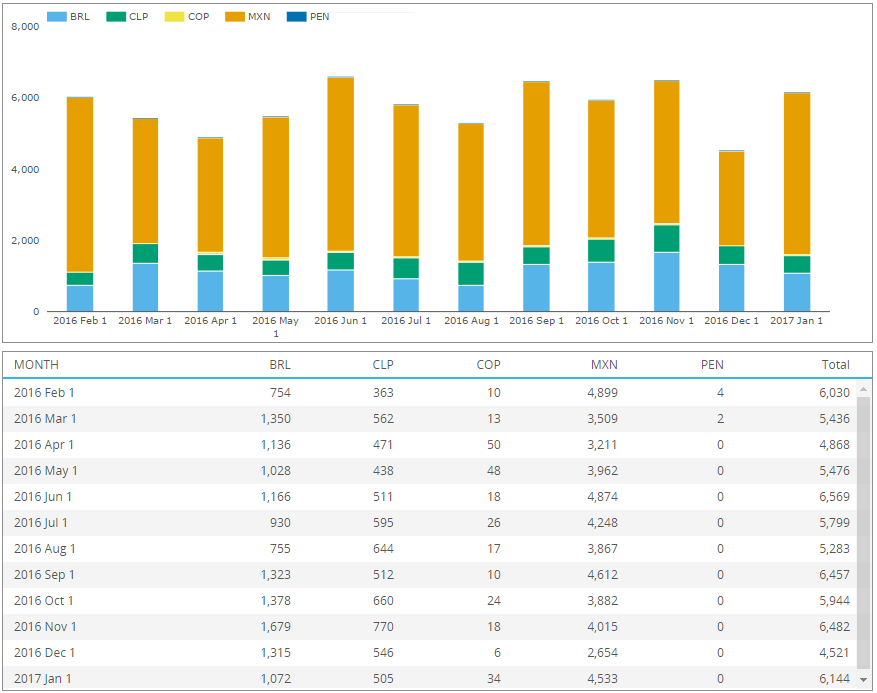

We use SDRView to look at Latam swap data traded by US names. Activity can be seen in BRL, MXN, COP (Colombia), CLP (Chile), CLF (Chile Inflation index), and PEN (Peru). We’ll start with vanilla Fixed/Float swaps:

The sizable trade activity appears to be MXN, BRL and CLP.

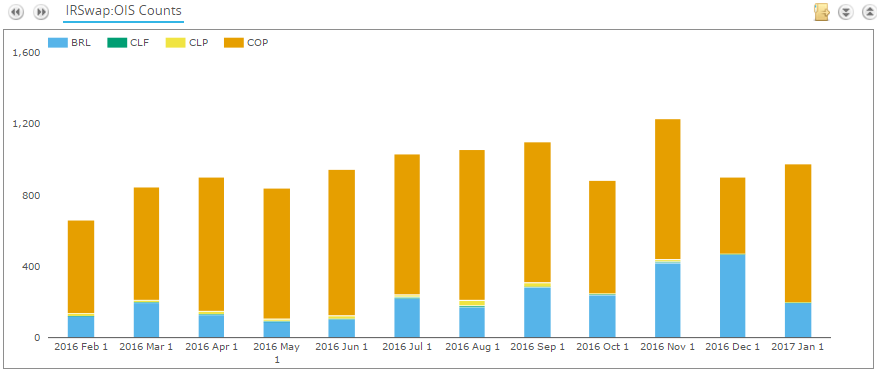

If you are wondering where COP swap activity is, this trades typically as an OIS vs their IBR index. All OIS shown below:

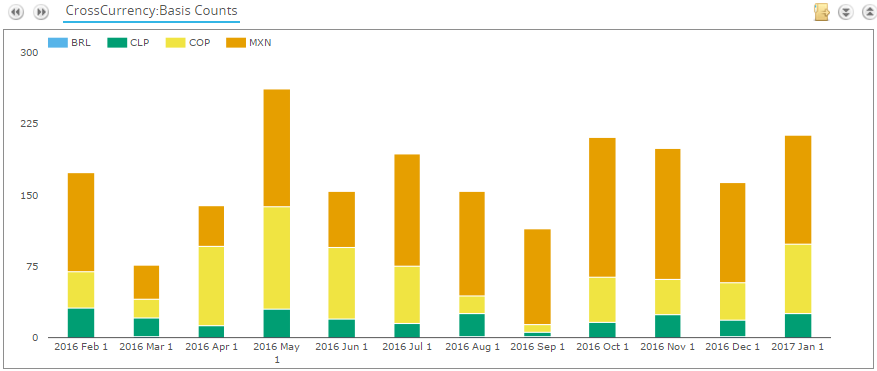

And my final chart of SDR data is Xccy Basis swaps (float vs float), where we see a decent amount of MXN and COP:

To round out other IR products for Latam swaps, we see:

- Options. Maybe 20 or so swaptions per month in BRL and MXN. Handful of MXN cap/floors.

- Inflation. Only a handful, maybe 30 in CLP, which is almost certainly the Chilean CLF inflation linked index.

- FRAs. None.

So where is Peru? PEN trades pretty thin by US names, but it does show up as the most active XCCY Fixed/Float product. That is, fixed PEN vs floating USD Libor. Maybe 20 or so trades per month. You can check it out yourself on SDRView.

Intraday Market Data & Aggregation

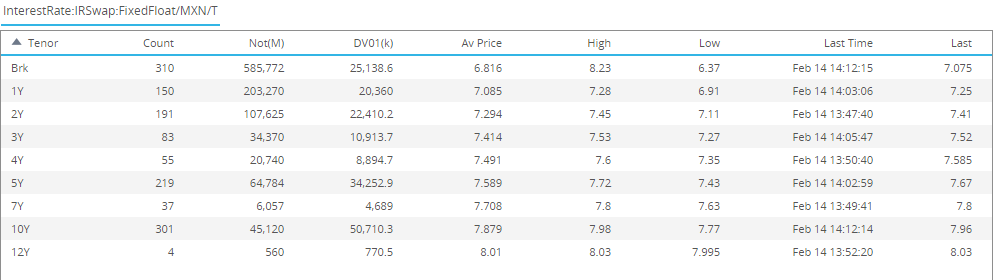

We’re also able to get some nice intraday market data on each of these currencies using SDRView. Across all of the Latam currencies, we see similar results as we do below for MXN – that the vast majority of Latam swaps are relatively short dated, generally only up to 10 years. For example, here is the most recent week of MXN swaps, by tenor, with total notional and DV01:

Clearing Data

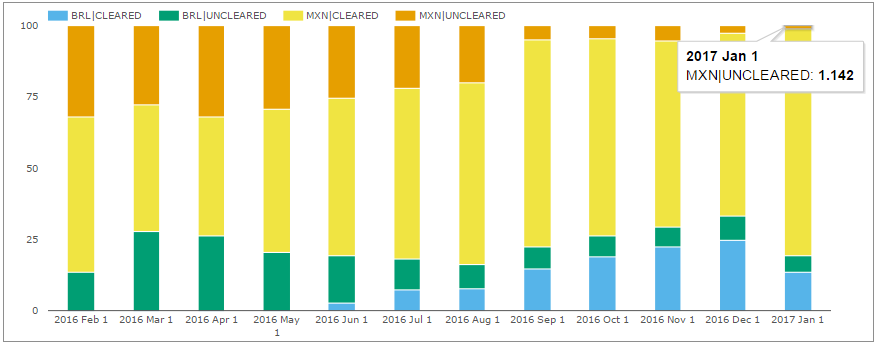

If we whittle down the SDR data to only the clearable currencies MXN and BRL, we can see how, over the course of the year, nearly all of the MXN market is now cleared, as is well more than half of the BRL market. The sliver of orange is uncleared MXN, and the green uncleared BRL. So very good progress on Latam clearing in the Americas:

There are 3 clearing houses globally that clear MXN, one for BRL:

I should note that BM&F Bovespa clear massive amounts of listed IR products for BRL, and have OTC swap registration services, but I don’t believe they are actively clearing IR swaps. If anyone knows differently, please get in touch.

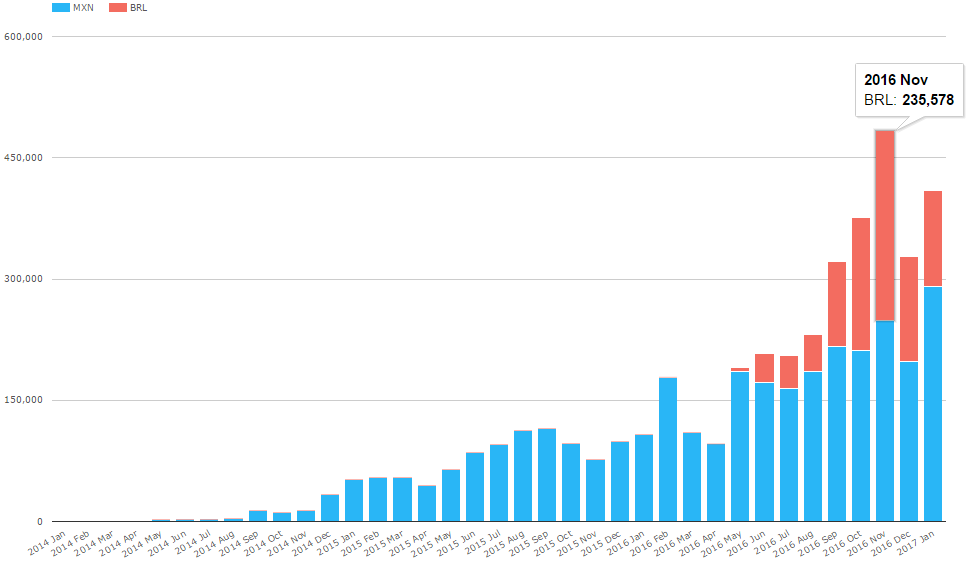

Turning to CCPView, we can see this cleared activity picking up in the past 12 months. It’s quite striking the volume of BRL is now nearing the same sort of magnitude as MXN. This in millions of USD equivalent:

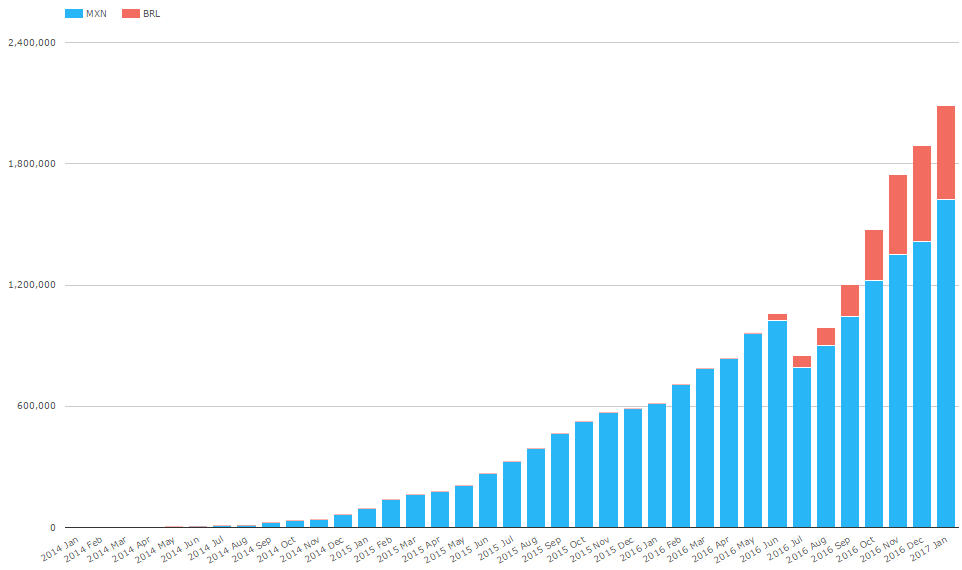

And Open Interest:

Which shows a significant MXN compression run in July 2016.

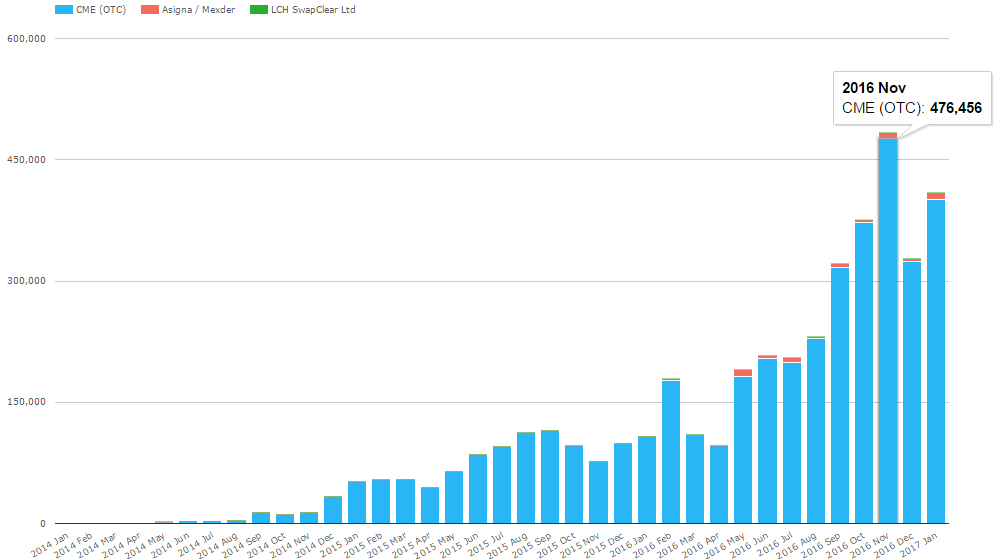

And now back to volume, this time by CCP, showing the bulk of everything above is CME cleared at the moment.

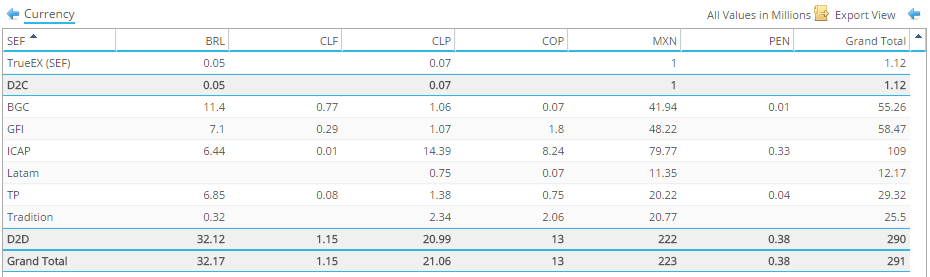

Execution (SEF) Data

So which US venues do these swaps trade on?

It appears all of the activity is on inter-dealer brokers, with the exception of TrueEx which has done some compression runs:

Mexican clearly the most active, with BRL and CLP a close second.

ICAP appears to handle about a third of Latam rate swaps, with BGC and GFI a close second.

Note Latam SEF, which is the US SEF version of IDB Enlace.

Leverage / Margin Required

As a last step, I thought I’d look at the amount of margin required to support a Peso swap. I began by keying in two 10-year vanilla swaps, one in MXN and one in USD. First port of call is to confirm the risk on these two trades (with notionals of ~280mm MXN and ~11mm USD) have roughly the same amount of risk. So I ran a DV01 to confirm they each have 10k USD equivalent of basis point risk:

Next, lets run initial margin assuming they were CME-cleared in separate accounts:

Which shows that for the same amount of basis point risk, we are required to post roughly twice as much collateral. I’ll save you the drilldown details for the time being, but the presumption has to be that the MXN position is more volatile and hence requires more margin.

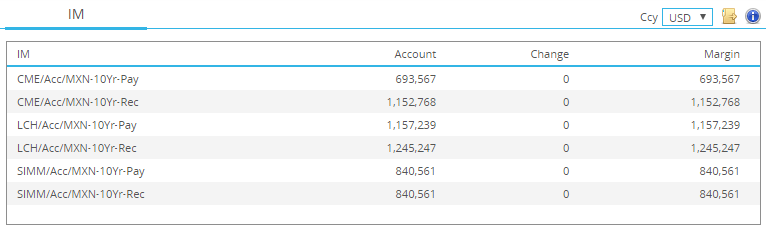

Shopping just the MXN swap around, lets see what it would cost elsewhere, be it clearing at LCH or keeping it bilateral and posting SIMM margin:

As we’d expect, the SIMM margin is higher than clearing at CME. The LCH number looks a bit high, until I decided to put in another account for a MXN fixed rate receiver for comparison sake. So here is the required IM now on both a payer and receiver in separate accounts, under the 3 separate methods:

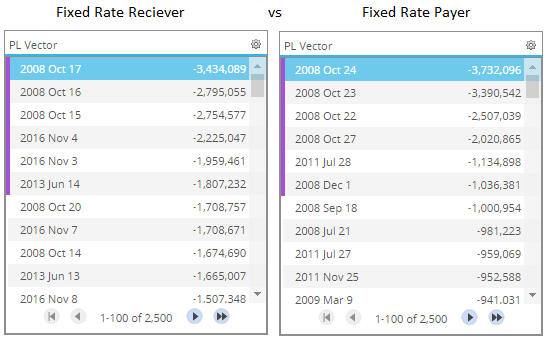

This highlights the asymmetry of CME margins (693k payer vs 1,152k receiver) and the symmetry of SIMM (always 840k). As to why this asymmetry exists, look no further than the simulated historical losses for each swap. I’ve drilled into the LCH margins below:

This shows us that the tail events for the Fixed Rate Receiver on the left are, in total, more significant (rate increase scenarios), versus the rate decrease scenarios for the Fixed Rate Payer on the right. You’ll find two US Election events in the top 5 losses for the Receiver, and is a good illustration of the asymmetry that you find in HVaR models.

Of course one big caveat when it comes to SIMM margins is you will have to gross up these margins across all of your counterparties, so its not a valid comparison – clearing should always be more efficient.

Summary

I learned a few things going through this:

- MXN and BRL swap markets are the two largest Latam markets traded by US names. Chile a significant third.

- Options markets for these are mostly thin.

- Both the MXN and BRL markets are predominantly cleared in America. CME has the first movers edge here.

- ICAP has brokered over a third of all SEF-executed Latam swaps.

- MXN swaps have larger tail events versus USD at least, giving rise to larger margin requirements.

- SIMM margin for MXN swaps, on the surface, looks generally comparible to cleared margins until you consider more than one counterparty.

Perhaps worthwhile to look at other Latam products such as NDFs, but we will save that for a later date.