MIFID II Data is Here!

Happy MIFID II day everyone. And happy New Year.

We thought it would be a great way to welcome in the dawn of added transparency in European markets with a live blog this morning to see what transparent trade reporting in Europe will deliver to us.

Remember to refresh throughout the day (hit F5 in your browser).

Update

We are now on DAY TWO of MIFID II. Head over to the latest blog to keep up-to-date.

8:20pm London

As you’ve probably guessed, that is it for today. It’s been interesting to see the data coming through. My gut reaction has been:

- There are a lot more quotes available for pre-trade transparency than I expected.

- There were far fewer actual trades reported in both EUR and GBP swaps.

- The data makes the SDR data in the US look very good.

- There are some tantalising snapshots of Compression data coming through.

All being well, we will be back tomorrow with a fresh mind to look at more data. Stay tuned.

5:10pm London

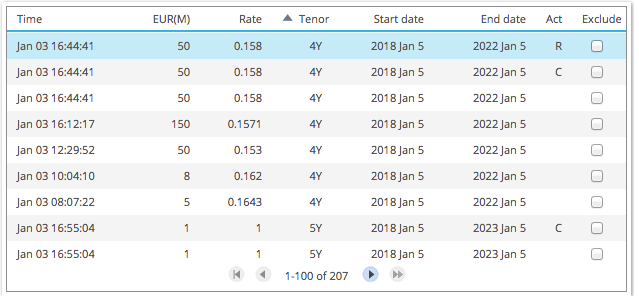

And to show we are in a global market, at 16:44 we see a 50M 4Y EUR IRS at 0.158% reported to US SDRs as an Off venue trade; so the price is exactly the same as the trade on the Tradeweb MTF (see 4:50pm).

(Lets hope these time stamps are both UMT).

4:50pm London

We have a trade! The number of EUR IRS that are being reported is startlingly low. So much so that we’ve tended to shout a bit about actually seeing a trade. For context, over 450 EUR IRS trades have been reported to the US SDRs today.

The trade was in EUR100m at 0.1580% – so close to normal market size! It looks like a spot starting 4 years. Tradeweb were the lucky venue.

4:45pm London

As at (nearly) midday in New York, we’ve only seen ~600 USD swap trades reported to SDRs. I know we are only half way through the day (and it will have been a slow start to the year for some), but that seems like a lower number than I would expect. A busy day typically sees 2,000 plus USD trades, a slow day ~1,000 in total.

4:40pm London

Uh-oh what did I say at 3:20pm?! Now we don’t even have a working ESMA registers page at all. I hope this means an imminent (ish) update to the registers. How long can it really take though?

4:25pm London

I should have started this blog yesterday as I could have seen these Credit trades coming through. I rescind the 09:20am comment….these were even earlier, but have Agreement times AFTER the Publication times. Really?

4:15pm London

More quotes, more data – this is all good stuff. The only thing I am scrathing my head over is the venue code. UBSI and UBSY shout a UBS MTF with a MIC code. But the UBS MTF is XUBS according to the ESMA register. Did they register two new ones at the last-minute? Are Systematic Internalisers also using 4 letter MIC codes instead of the BIC-like codes we saw earlier? This data is presenting a LOT of questions today….

4:00 pm London

Well, at least we don’t HAVE to report ISINs. Some APAs provide some meaningful descriptions. And there is a lot of seemingly illiquid stuff being reported here too!

However, after my previous moaning about ISINs I am now even more confused. How do I start to decode this “OTHER” format! One for a later day.

Interesting to see currencies such as ZAR, TWD etc being reported. And this data happens to be easier to find and easier to work with than a vanilla ten-year EUR swap at the moment!

3:20pm London – Calling ESMA!

I’d like to remind ESMA that they promised an updated list (it’s only an Excel file!) for all APAs, ARMs, CTPs on the 3rd Jan 2018. That day is today….and it would be really bloomin’ useful right now! Anyone seen it?

3:00pm London

A quick update for those just joining.

- MIFID II date is live!

- We now see pre-trade quotes.

- And post-trade reports.

- The sources of data are varied, and usability of the tools varies.

- We’ve seen more transparency for even US Treasury markets than previously.

- We’ve seen quotes in Swaptions and Inflation swaps.

- We’ve only seen two pre-trade quotes for vanilla swaps so far…but remember that not all data is persisted.

- ISINs are, predictably, terrible things.

2:40pm London – An Open Access Aside

As I take a break from downloading yet more empty zip files (just tell us “no trades” please!), I noticed a big MIFID II story overnight (on Reuters here). Open Access for futures contracts has been given a reprieve until 2020. I was always a little bit unclear (pardon the pun) how this would actually work, but it seems like the exchanges now have a couple more years to work it out.

2:35pm London

Do these new sources of data feel “polished”? Do they feel finished? I noticed an interesting facet of the data pages – only TP-ICAP remembered to include their logo on the tab of the webpage. It is a simple thing but gives the impression these are far from finished solutions that have been put into the wild.

2:30pm London

Well, one APA at least provides a list of ISINs that have traded so far. I’m not sure if this helps to improve transparency or highlights how useless an ISIN is?!

2:20pm London – Where is EZ90V61F3M53? I’m a point 9 offer….

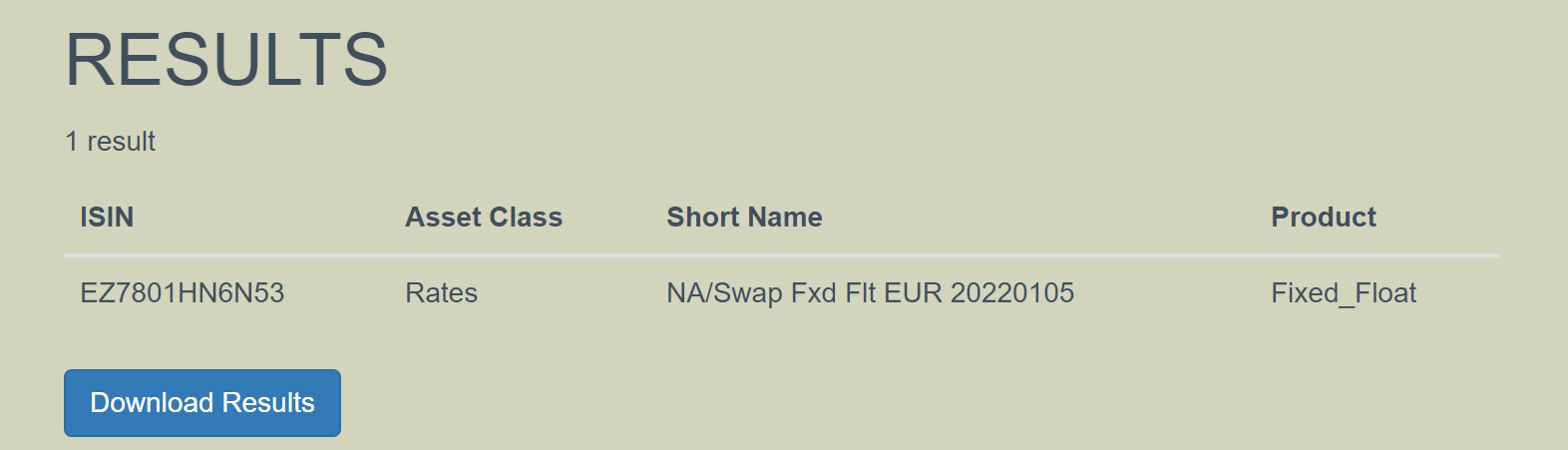

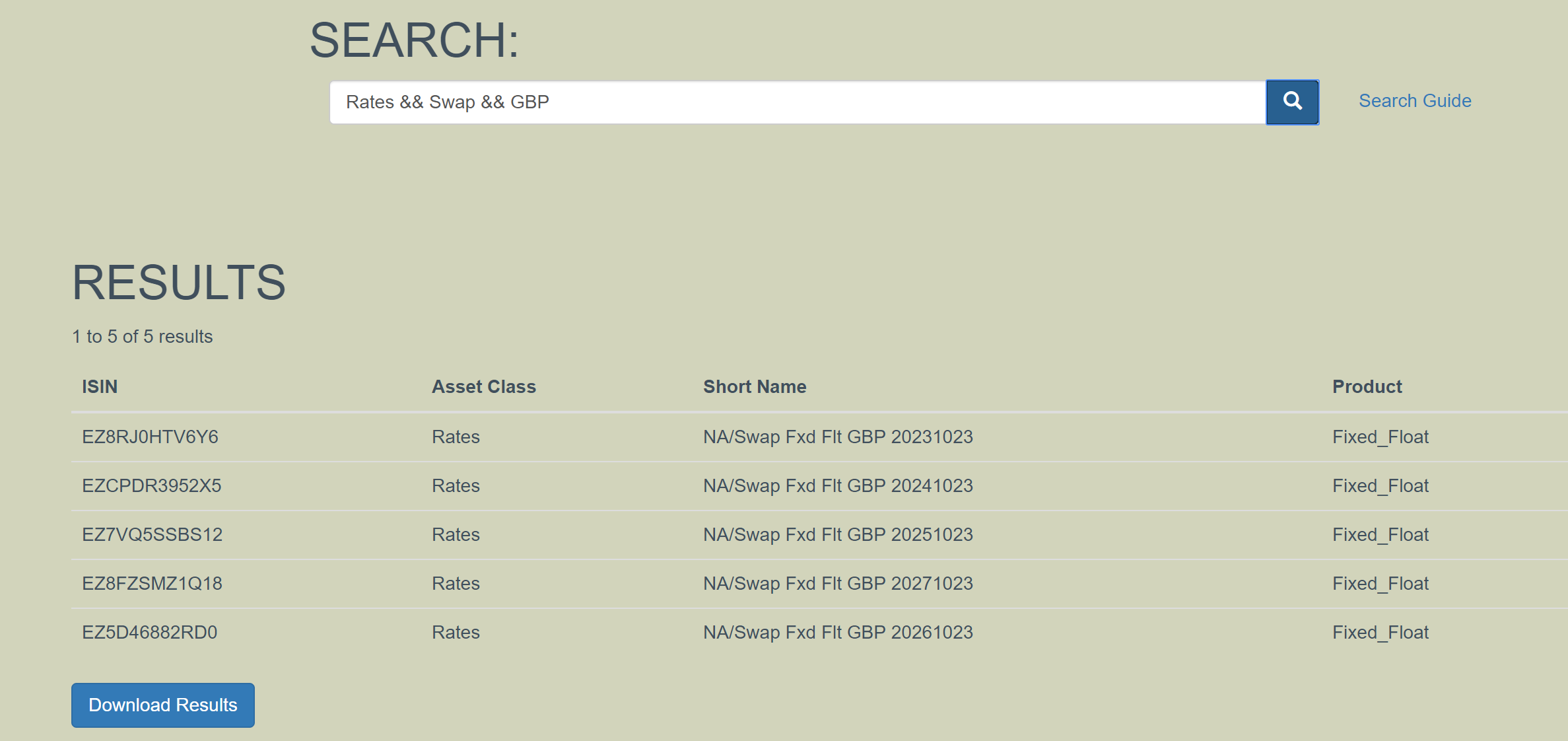

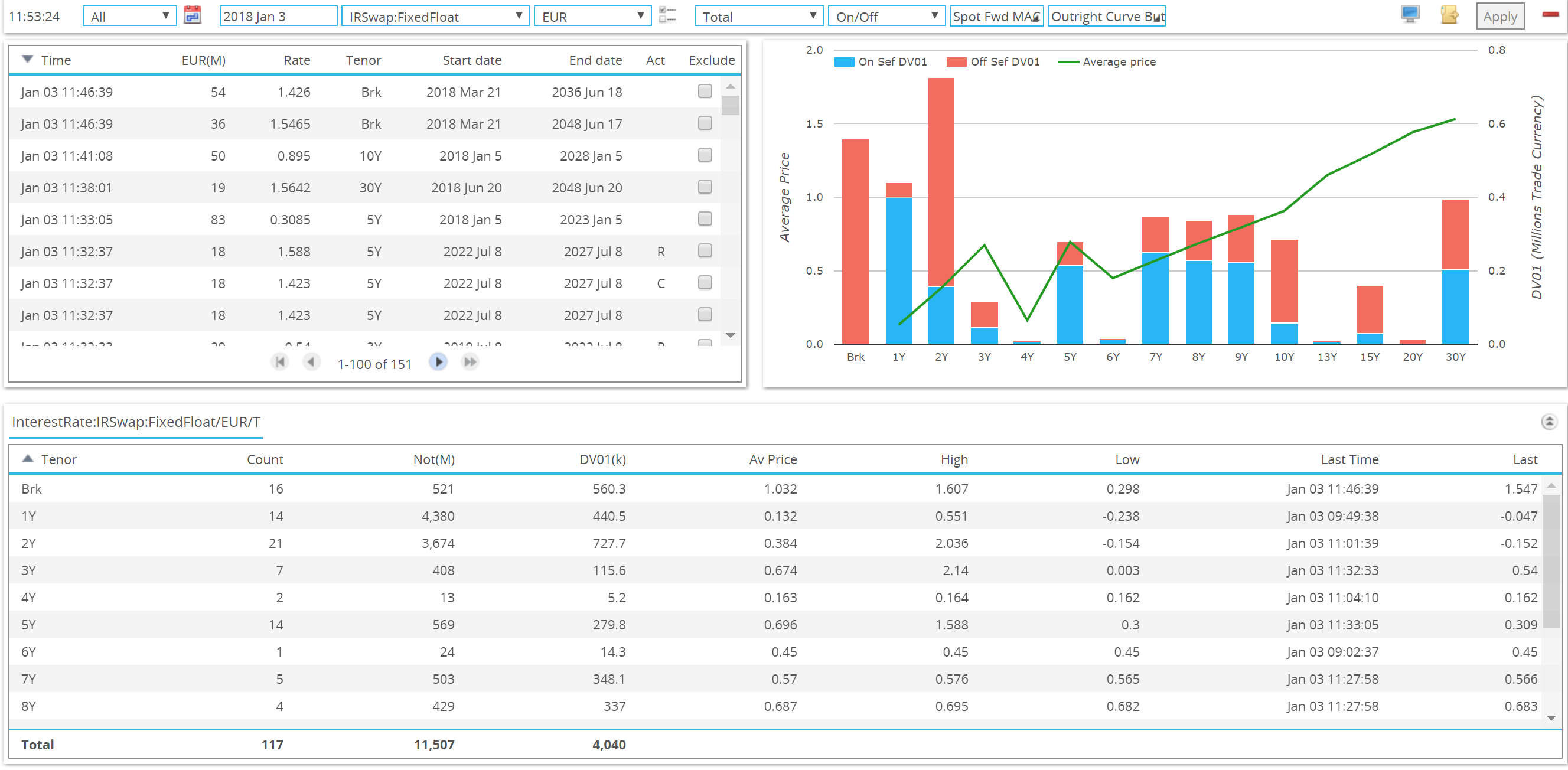

We have a 10y EUR quote! My mistake previously, the 5 years was being quoted vs 3m EURIBOR. This one, however, is a nice plain vanilla (assume spot starting) 10 year EUR IRS versus 6m Euribor. ISIN is EZ90V61F3M53. Not quite as catchy as “where is 10 years?” is it?

I make that TWO pre-trade quotes for interest rate swaps so far today….quiet day everyone? Even APAs that allow an ISIN search don’t provide any pre- or post-trade transparency reports on this ISIN. Is this possible? 10y EUR swaps haven’t traded yet? Does it have a funky start date? Oh, so close to transparency and yet so far away….!

2:05pm London

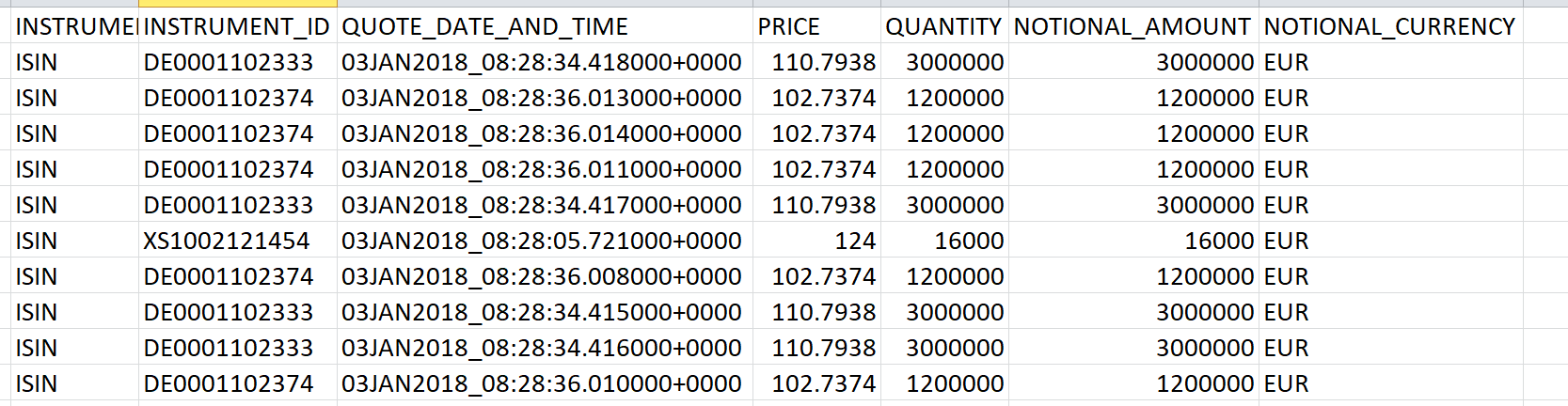

For those of you banging away at the DSB ISIN searches, I think searches are limited to five results. So best to know your exact expiry date!

2:00pm London

Poking around and found an Inflation Swap quote from earlier this morning.

It is not easy to find orders or trades!

1:30pm London

We have trades in a German BOBL, African Dev Bank, European Investment Bank and a BTP going through.

Surely an bond instrument name field with “BTP 0.65% 1/11/20” would not have been too much to ask?

With all this money spent, I know ISINs are important, but so too are human understandable descriptions.

12:10pm London

We have an IRD quote! Forgive my excitement 🙂

5y EUR Swaps we are (were) 0.2188..bid? offer? Oh come on, you’ve got to be kidding me….is directionality really not a required field?!

Midday London

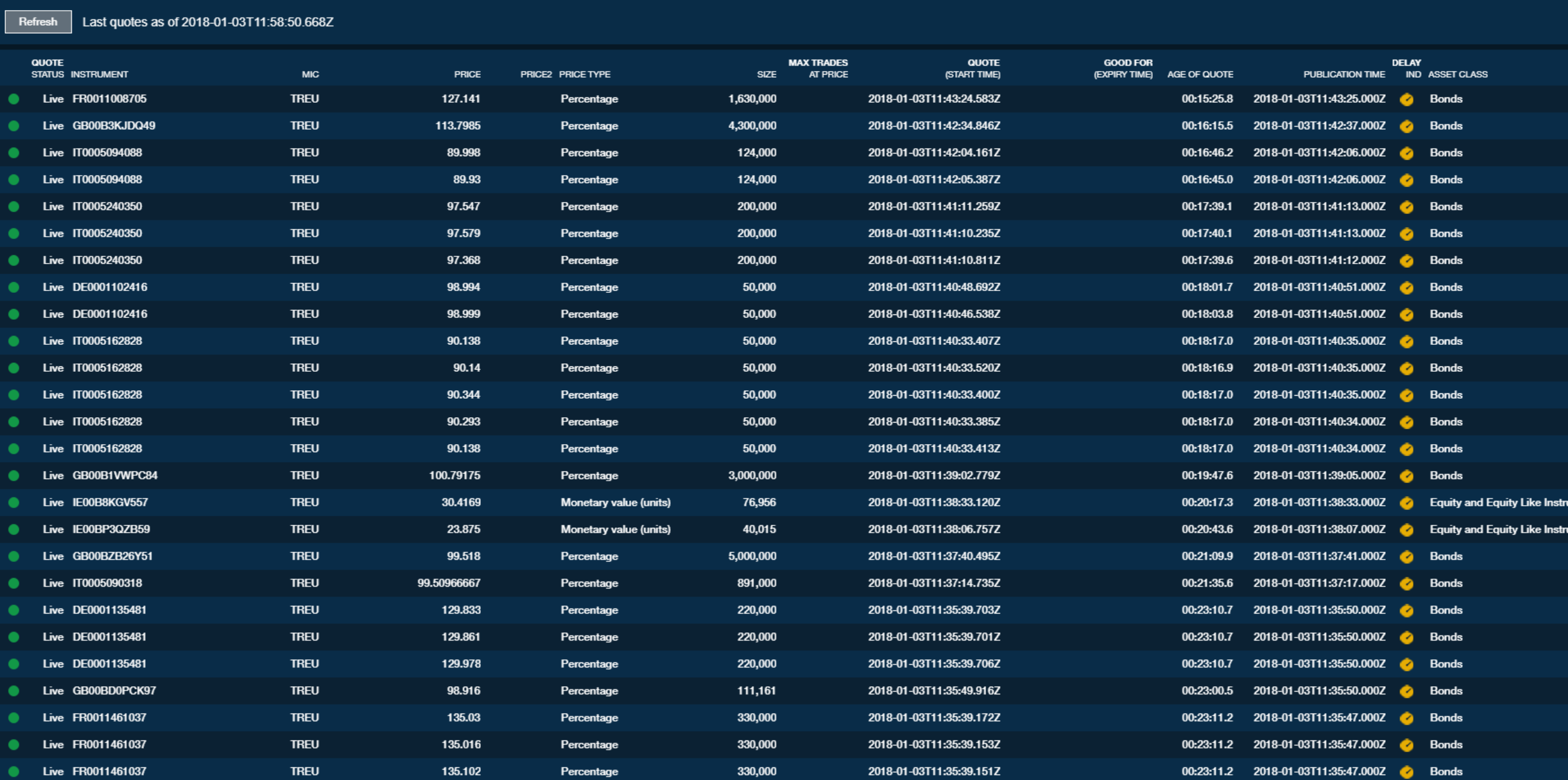

We finally have quotes! About an hour ago, somebody, somewhere flipped a switch. We’ve got quotes! Lots of pre-trade quotes. Remember – this is a time series of PRE TRADE information. Whoop whoop!

10:50am London

Before New York opens, I wanted to check if there has been any obvious impact on SDR reporting. With elements of equivalence, we could either see more trades reported to US SDRs – because we know the pipes work and it is safe – or we could see more trades reported under MIFID II because the post-trade transparency is lower (two to four-week deferral period).

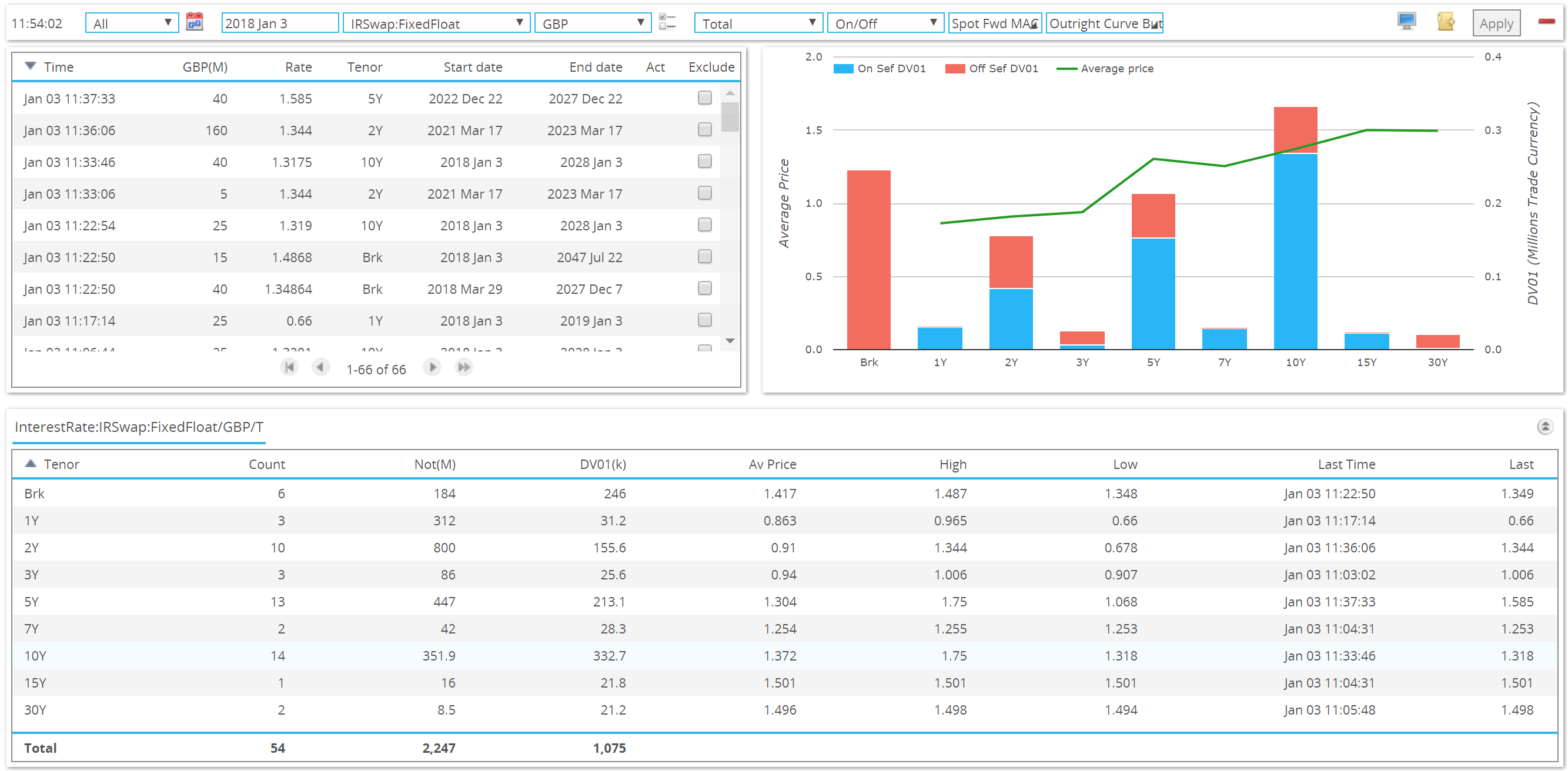

So far, we’ve seen decent numbers of both EUR and GBP swaps reported to US SDRs, so no obvious impacts either positive or negative. We need to wait for USD markets to open, and we can make a call on the end of day data later.

10:20am London

Some AUD transparency for you. Interesting to see the time-gap between trade date time and publication date time of nearly two hours. I thought we only had options of 15 minutes, two days or four weeks….

In case anyone is interested, the ISIN was EZ2D72DRSPT4 for that trade. Just to be thorough….

10:15am London

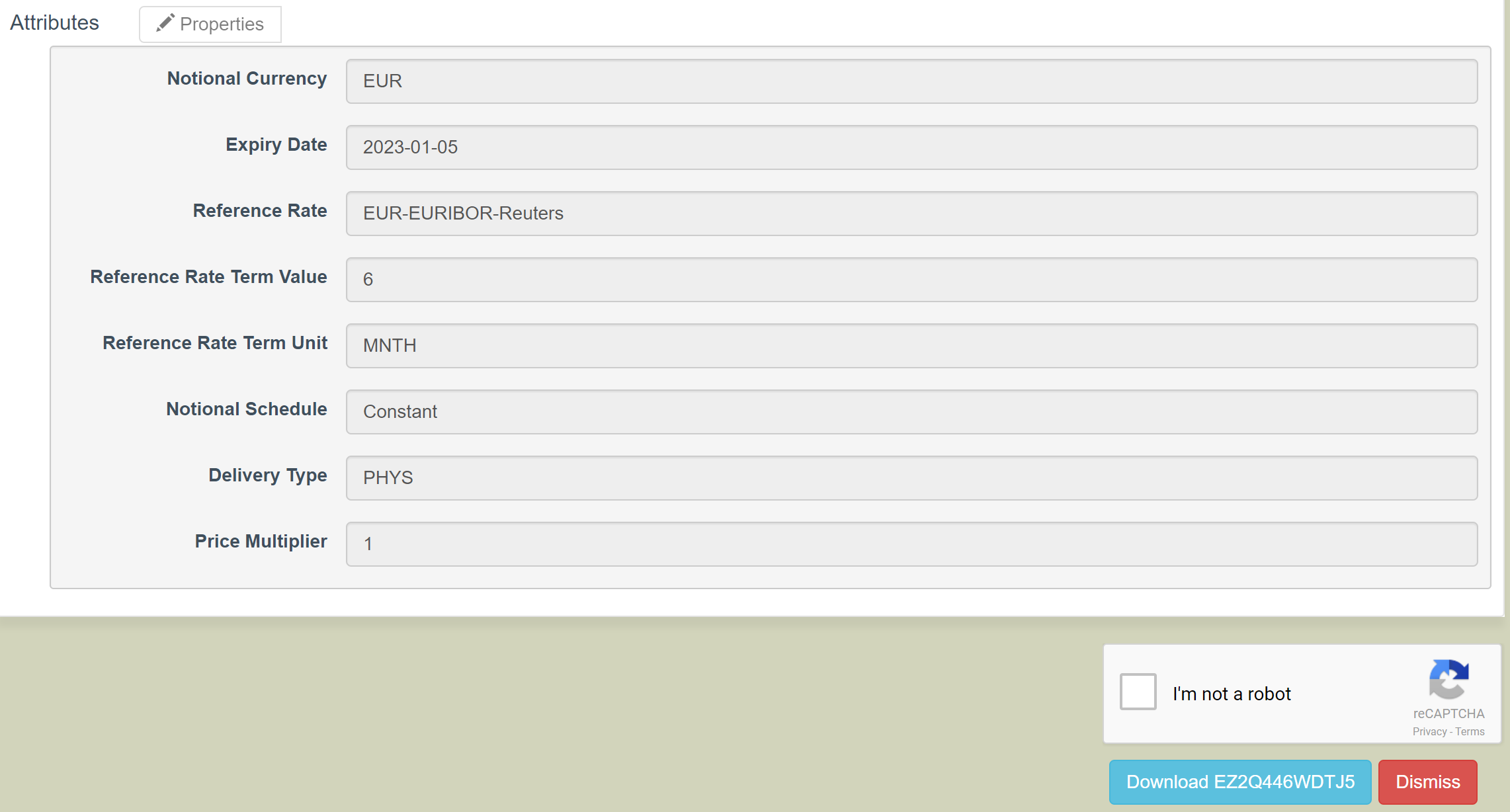

There appears to be no start date field for Interest Rate Swaps in the ISIN fields. Now THAT’s an interesting approach to transparency….

This ISIN was from the most recent IRD I saw reported:

09:45am London

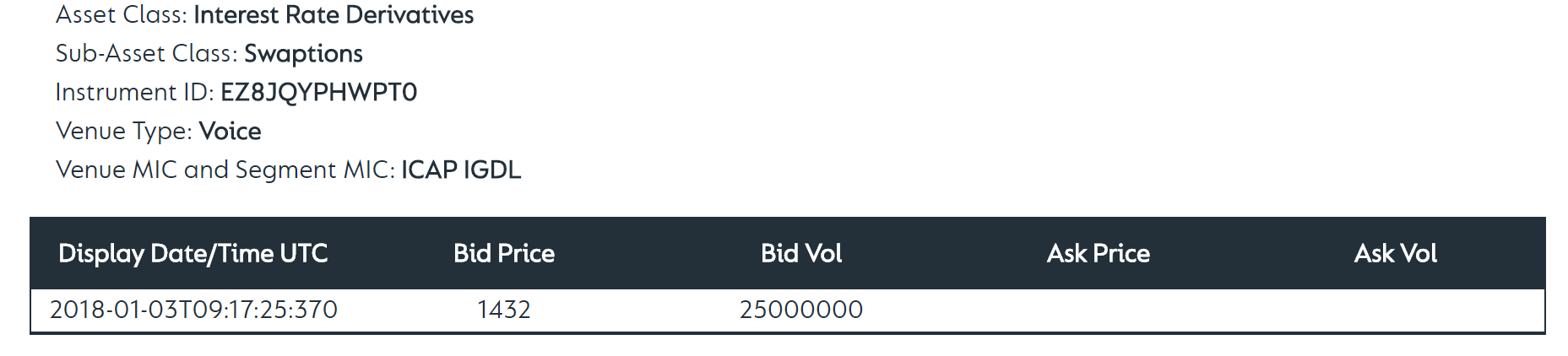

We have Swaptions data! I didn’t expect that to be one of the first quotes I ran into for pre-trade transparency. Here we go:

Fans of pre-trade transparency will appreciate that I now have to do an ISIN look-up on the Swaption….

Oh great, so I have to do TWO look-ups for each Swaption. Oh joy. The underlying is hence:

Exactly as we feared, these ISINs do not include the start date of the instrument….

Fortunately, we have to assume that the expiry is done out of spot from the Swaption expiry data. It will be interesting to interrogate the swaps data a bit more on this start date issue however….

09:20am London

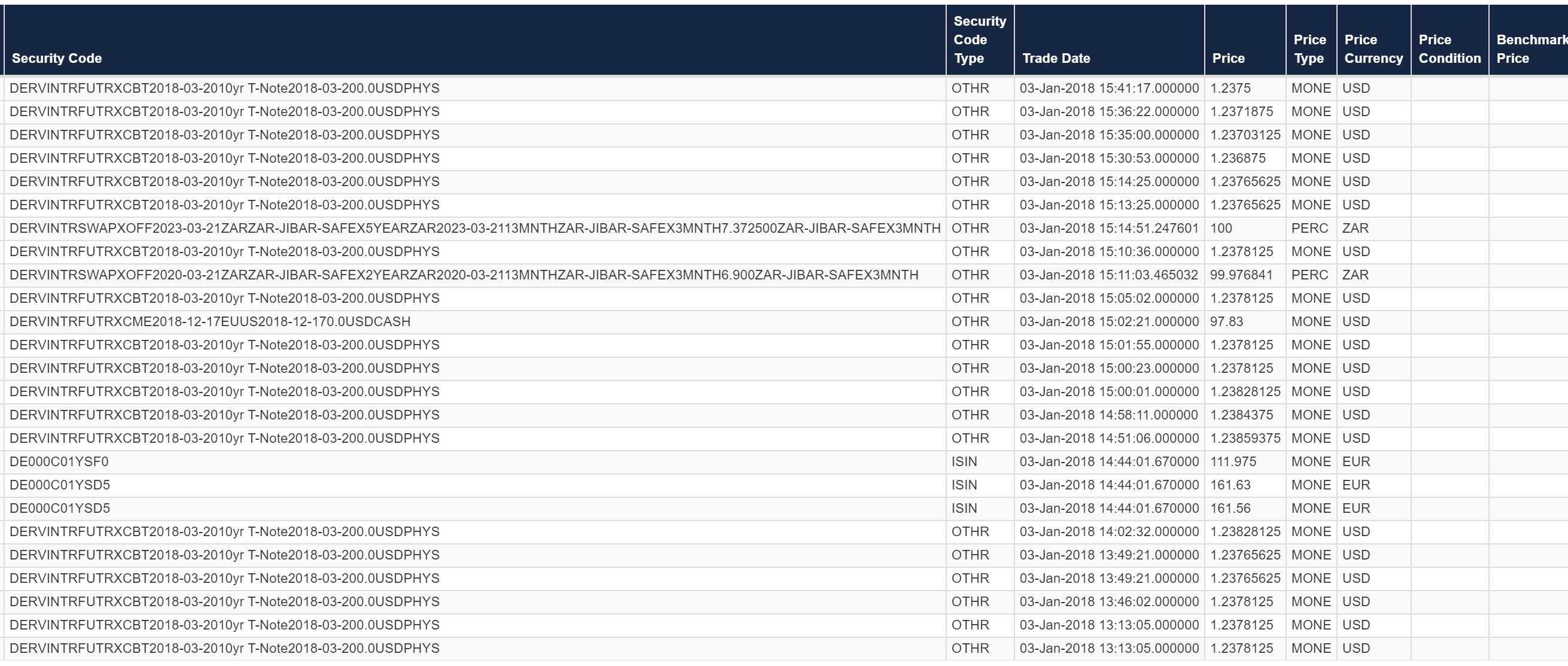

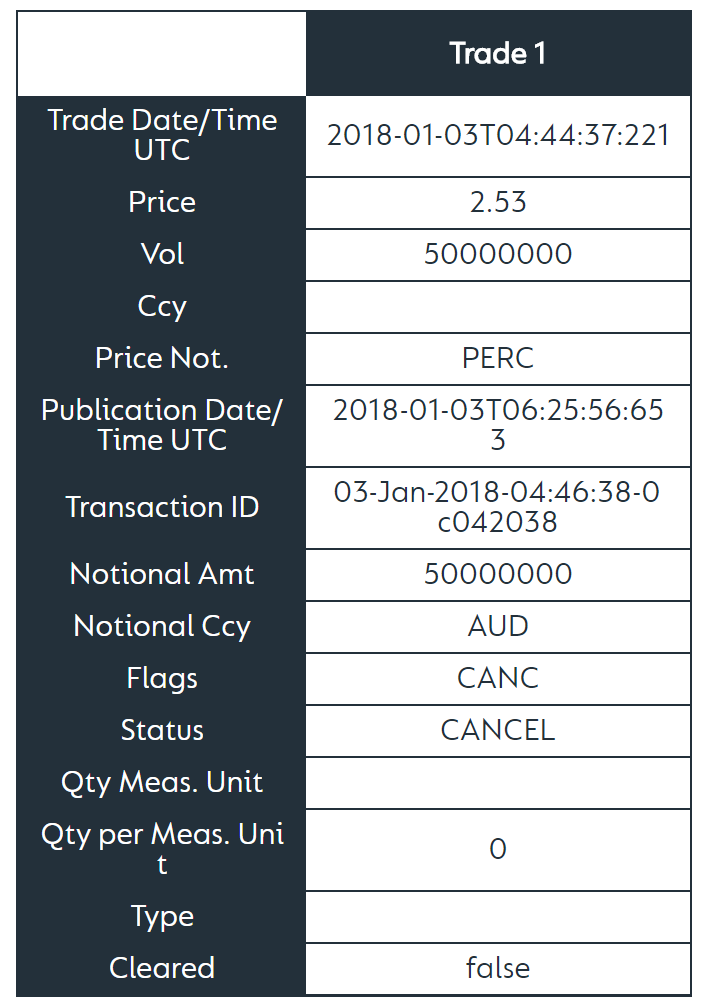

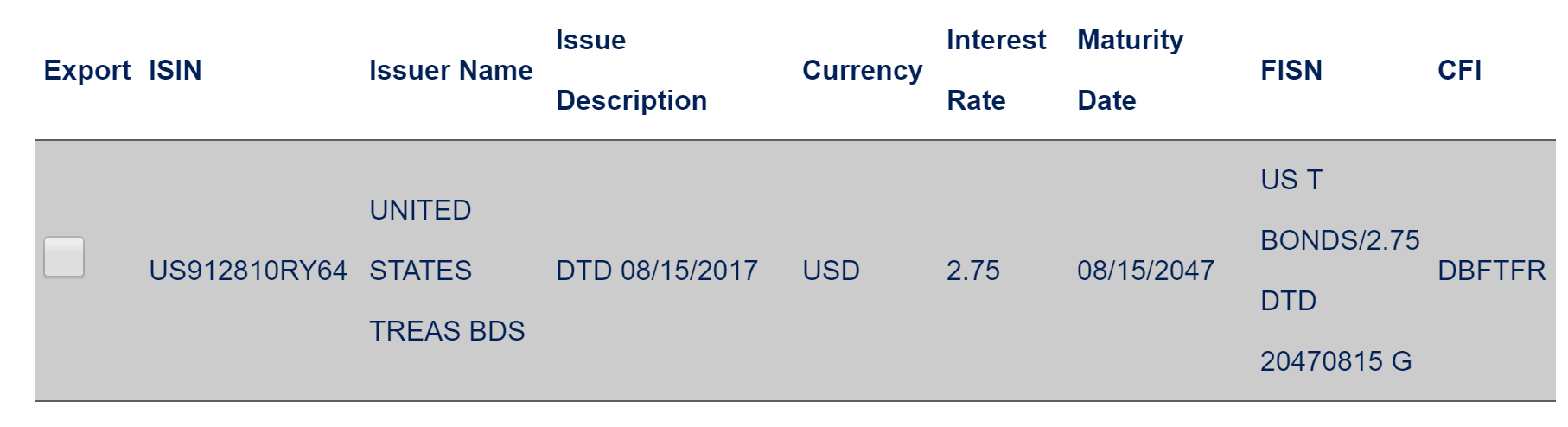

It’s not just OTC derivatives that we’ll see post-trade transparency for. I remember reading long ago this article on Tabb that pointed out the transparency requirements would also apply to US Treasuries. And lo-and-behold, what I think are the first ever trades reported under the new MIFID II transparency requirements were indeed US Treasuries (okay, one was a T-Bill).

I was expecting to see some test trades from banks making sure the pipes were working. But no, this bank just goes ahead and does nearly $5m in 30 years! We know it was a bank (or a “Systematic Internaliser”) by the SINT designation.

As I said, you need to look up each ISIN to know the details for the transaction. Here is the result of that first ISIN look-up:

And the second trade? That was more in-line with expectations of test trades as a nice short-dated T-Bill:

09:10am London

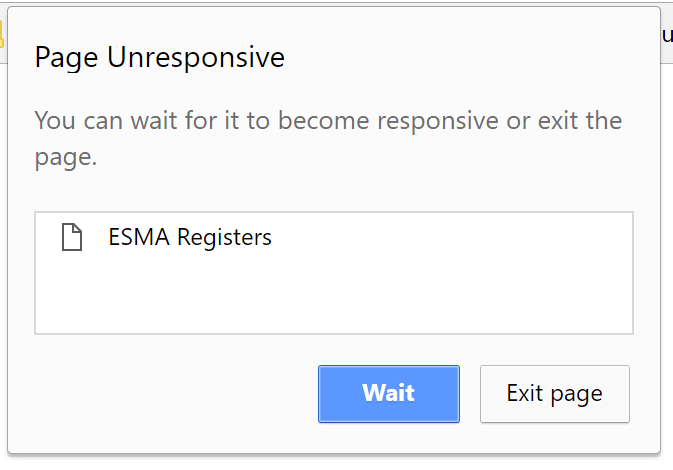

Phew, the DSB is back. I wonder how long it was unresponsive for? The time gap in emails was 57 minutes!

09:05am London

This was predictable. You may notice that the data below has very little information about the actual instrument, save an ISIN code. So it means a lot of look-ups versus ISIN databases. The Derivatives Service Bureau provides/creates/maintains those ISINs for OTC derivatives (which we are mainly interested in). Guess what just popped into my inbox? Yup, you guessed it, the DSB database is down….

Anyone care to define “essential” here?!

08:55am London

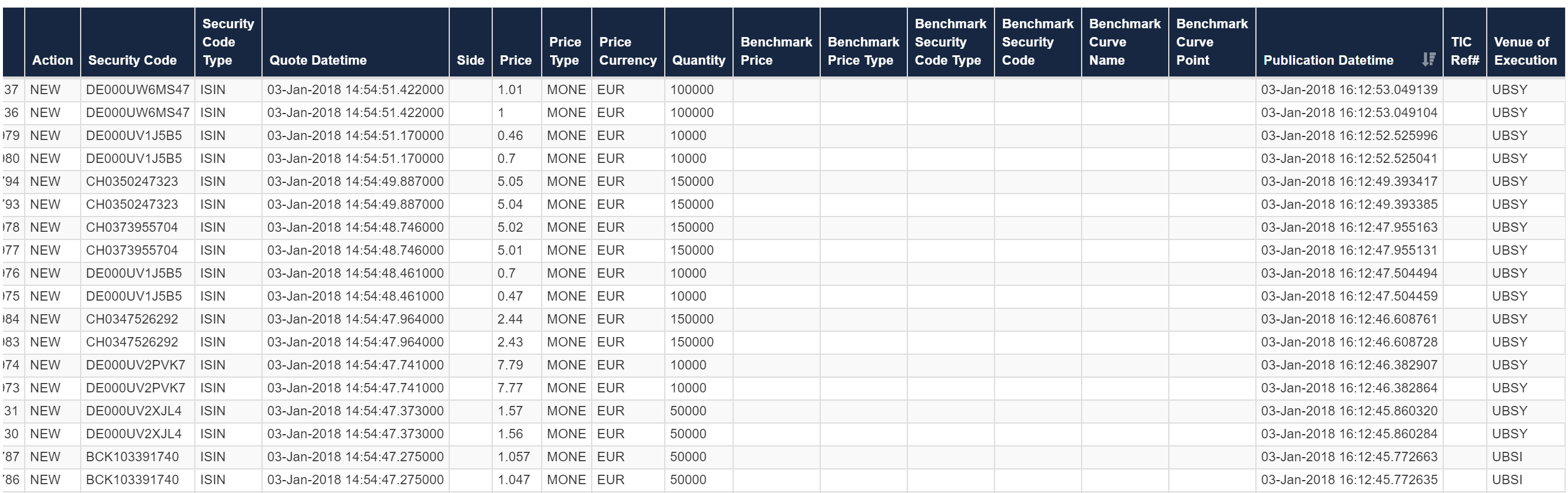

We have the first data! Well done to the large Dealer to Customer venues for providing us with simple, online access to both quotes and post-trade reports.

It looks like reporting didn’t actually come on-line until 6am this morning for all of the venues and APAs that I checked. But here is some pre-trade order transparency for bonds to whet the appetite:

And post-trade transparency is more in-depth:

Check back later for more data and thoughts as they come.

Any thoughts/comments, please add at the bottom of this blog or reach out to us.