We are 11 weeks on from the October 2nd start date of SEF’s. Bit of a quiet week, outside perhaps the TrueEx announcement of performing their first trade compression cycle, what TrueEx have called PTC (portfolio trade and compaction). Tradeweb had announced something similar towards the end of November, but I was excited to have a look at it in the SEF data. Unfortunately it raised more questions than it answered.

But first, lets have a look at the data.

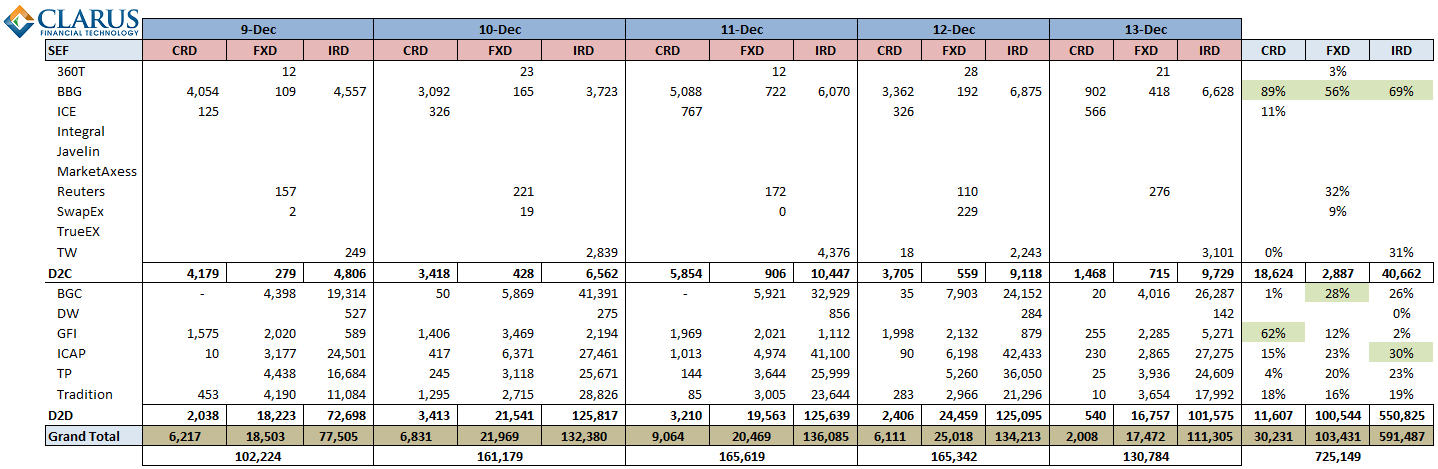

This weeks data

Lets start with daily activity by asset class, reported in USD Million equivalents. Excluding activity in FRA’s:

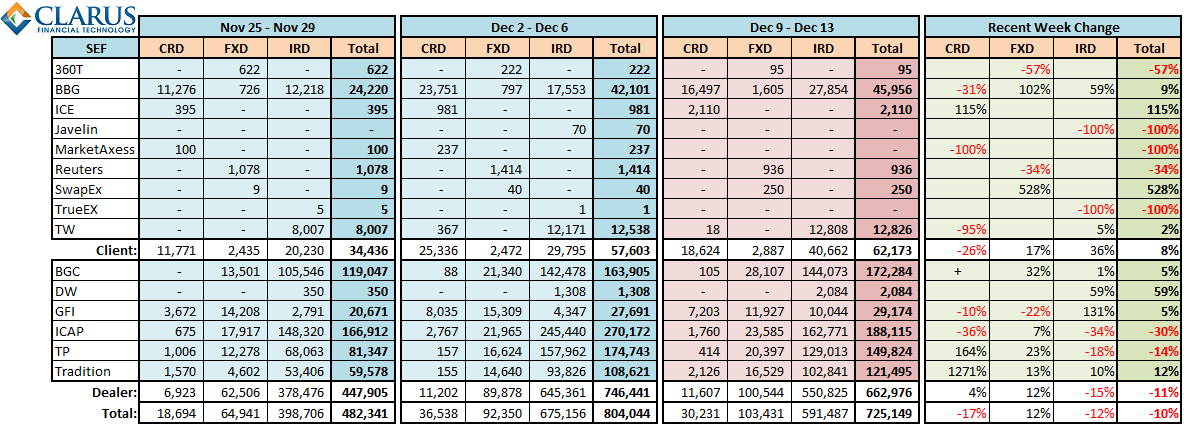

And now with all of the history, its interesting to look at weekly changes. Numbers for the last 3 weeks:

What To Make of It

Some commentary and observations on this weeks data:

- ICE have requested they be switched from D2D to D2C, so I have obliged. I had asked the question back in Week 6 and received some comments leaning towards D2D, but now its official. Moving them to D2C continues to tip the balance well in favor of most credit being traded on D2C SEFs, approximately 62% this week.

- SwapEx had a notable increase in their FX activity.

- Bloomberg continues to garner more than half of activity across all asset classes for client activity.

- Some notable increases in the D2D space:

- GFI’s presence in IRD has grown from very little in November to significance

- Tradition’s presence in Credit has grown, particularly if you look back to previous weeks in November

The Truth in TrueEx

I’ve confirmed that I probably do not quite understand the intricacies of the portfolio compression being offered by SEF’s. When I think of trade compression, I often think of Tri-Optima’s service to the dealer community. However, I believe what the client community are looking for, and what the SEF’s are offering, are effectively trade offsets, which when cleared, can result in terminations, compression, or even trade transfers across funds (aka fund re-balancing). Hence packages of trades are priced up for equal and opposites, and when executed and cleared, the DCO’s do what they do on a nightly cycle and compress exact equal and opposites. In my mind, a client could even price up a “location swap” / “DCO swap” – to move from CME to LCH, or vice-versa.

So in other words, the SEF’s are the facilitators of execution for these compressing/terminating/transferring trades (offsets), and the DCO’s are the actual compressors. Importantly though, these trades are NEW trades.

Right?

Well, then why can we not see this reflected in the TrueEx activity for the week?

After reading some documentation on TrueEx’s service, I can only surmise that everything I have said above is true, but is focused only on cleared trades, and that the SEF’s are offering similar services for trades that remain bilateral. TrueEx’s literature indeed mentions both cleared and uncleared. Hence SEFs are also offering the same service of arranging terminations, but instead of leveraging the DCO’s for compression, are also doing old-school fee-based tearup terminations. Just in the new age.

Cool.

Unless I’ve still got it wrong. Comment if you can confirm or explain otherwise.

Cleanup on Aisle 11

While I have complained in the past of the poor data formats and inconsistent standards across SEFs, I have spot-checked various SEF’s and confirmed that they are reporting one-sided, in the right currency notionals, etc. However one continues to cause grief on a weekly basis. I wont name any names. However I will say this particular SEF needs to do a complete 180 with their reporting.

Take these two trades, reported on the same day:

Given the Notional Currency of USD, one might think the first trade (or position) was 648 million USD of USD/INR transacted. However when looking in our new FX analysis in SDRView for this trade, I find that it was, surprise surprise, a 648 million INR notional trade. OK fine, so that means that the notional is always in Cur 2, right? Bzzzz. Wrong. Again, using SDRView, I was able to confirm the second trade was in fact a USD notional. Dont worry though, I’ve done enough homework on this to make sure these are not skewing the numbers, we are adjusting appropriately for this particular SEF.

By the way, I mention our new FX analysis in SDRView. Please note that FX is still only in beta, so not available to the public yet. If you have interest to be a beta tester, please get in touch with us!

Next Couple Weeks

Like many of you, we intend to take a few days off over the holiday period. Please check back for the blog. We’ll keep the data around, and should we get time away from the Egg Nog, we intend to keep providing updates.

UPDATE

This weekly issue of SEF updates is not the most current. To see all SEF posts, including the most recent, please click through to the SEF Category.