Week 9 was a short one here in America. The tryptophan hit the market as usual on Thanksgiving day, and lasted largely through the rest of the holiday week.

The Numbers

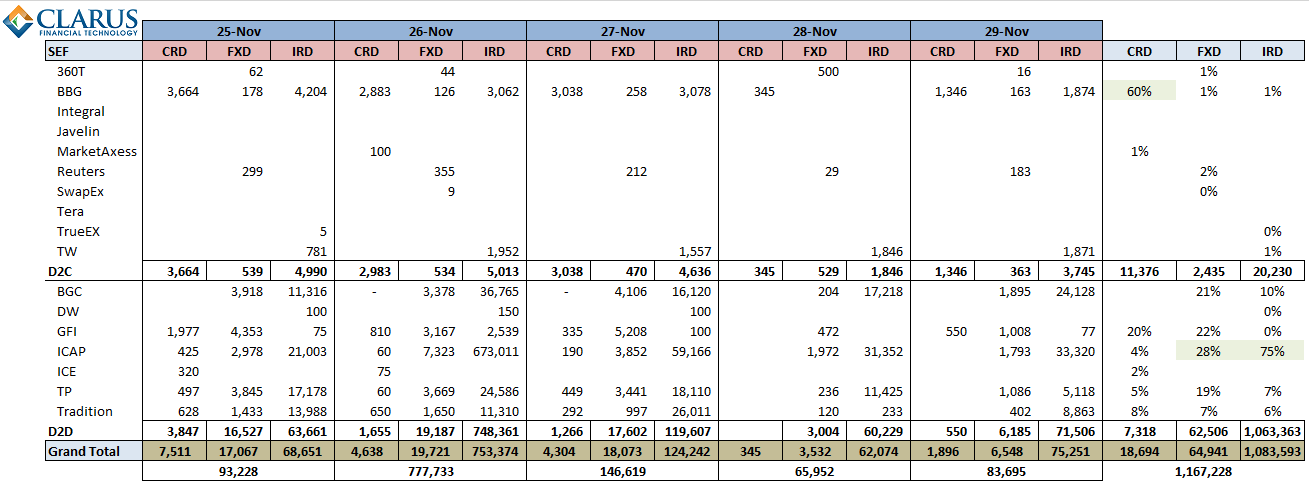

FRA la la la la……

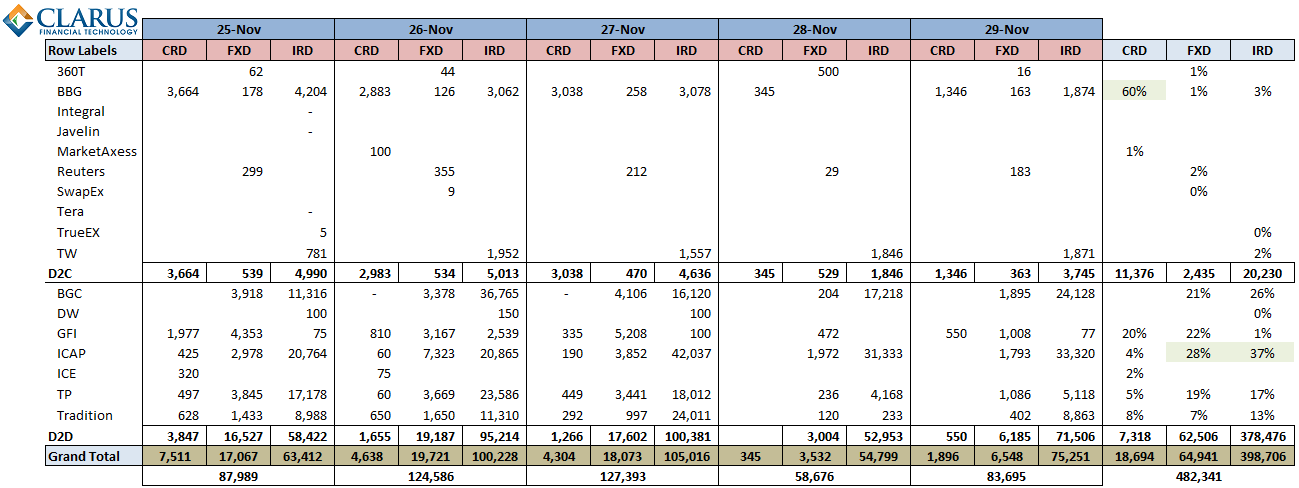

Normalizing to exclude FRA’s:

WE GOT THE DATA

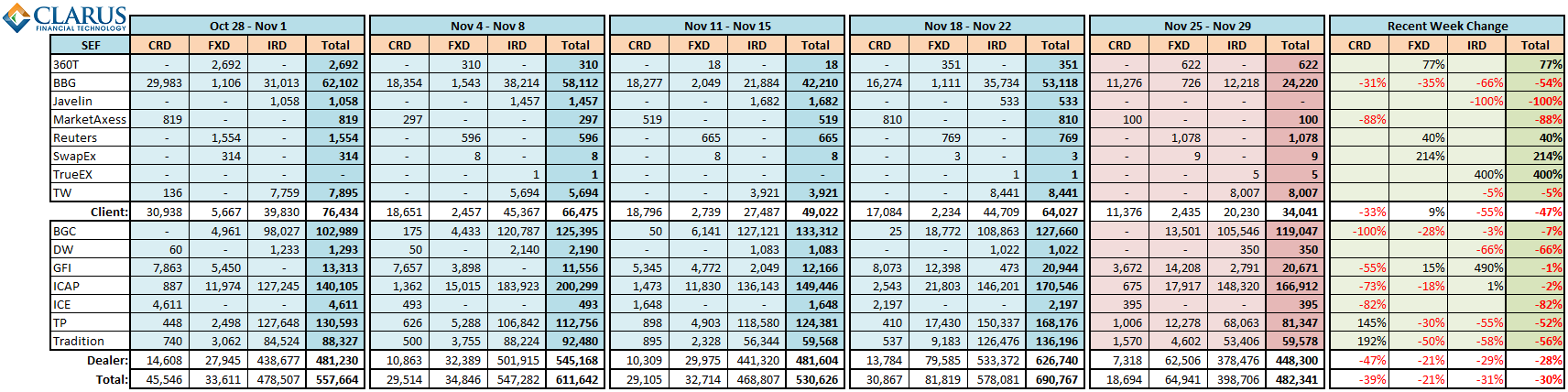

As we build up the week-on-week data, we can see some trends in each SEF as well as in each asset class:

Some notable observations

- Thanksgiving is a slow week. Seeing client volumes off nearly 50% and overall volumes off 30% seems about right. I dont think much credence can be given to even 100% drops for this holiday week.

- 360T volumes had trailed off week-over-week through the end of the no-action relief, but had a slight resurgence in week 9.

- Bloomberg continues to pound the credit market. Once again they do more business in credit than all of the D2D SEFs combined!? This would imply that any risk offsets from the banks are being done off-SEF? A quick look at SDRView tells us that roughly 2/3 of the Credit volume is indeed done off-SEF.

- GFI had a small resurgence in rates, from their non-existant start Oct 2. GFI’s Credit business still the tops among IDB’s, however both TP and Tradition showing some growth in IDB Credit.

- ICAP rates continues strong.

- FXD asset class had a second straight week of bunching up across the IDBs. We at Clarus intend to launch FX analysis in SDRView in the coming weeks, where will be able to drill into this a bit better.

Gensler pointing fingers

In his speech at SEFCON, Chairman Gensler spoke of many of the SEF’s not providing “Impartial Access”. He explicitly named Bloomberg, MarketAxess, and Tradeweb as culprits. I would think at least Bloomberg might have been said in error; and why not name the large IDB’s? Probably because they were buying his lunch that day.

In any event, it appears the doors are being forced open by the latest CFTC guidance. The interpretation is that SEF’s must not limit counterparties to a trade, specifically excluding things like requiring members to self clear or have pre-arranged breakage agreement in place. There is also guidance that the agency model is in play, which may enable SEF aggregators to operate freely, like what UBS is intending to do. Will that model work? And what will that mean for the SEFs, both large and small?

Time will tell. We’ll keep our eye on the numbers.

UPDATE

This weekly issue of SEF updates is not the most current. To see all SEF posts, including the most recent, please click through to the SEF Category.