Last week we covered SOFR Market Developments covering the comparison of SOFR derivatives volumes vs Libor and FedFunds, which highlighted the massive growth that needs to happen for SOFR to surpass Libor as the primary interest rate reference index.

Every firm active in Futures and Swaps should be tracking the uptake of SOFR trading and comparing their own trades with the market, to answer questions such as are we lagging, leading or in the middle of the pack for the upcoming disruption that is going to hit Libor derivatives.

In today’s article, I want to highlight how Clarus Data Products can provide this insight.

So rather than rely on our periodically irregular blogs (is that an oxymoron), you can do this analysis yourself on a daily/weekly/monthly basis for your own firm. After all actual metrics to inform your Libor Transition program are much better than gossip and rumour, or even irregular blogs!

Let’s look at some of the data.

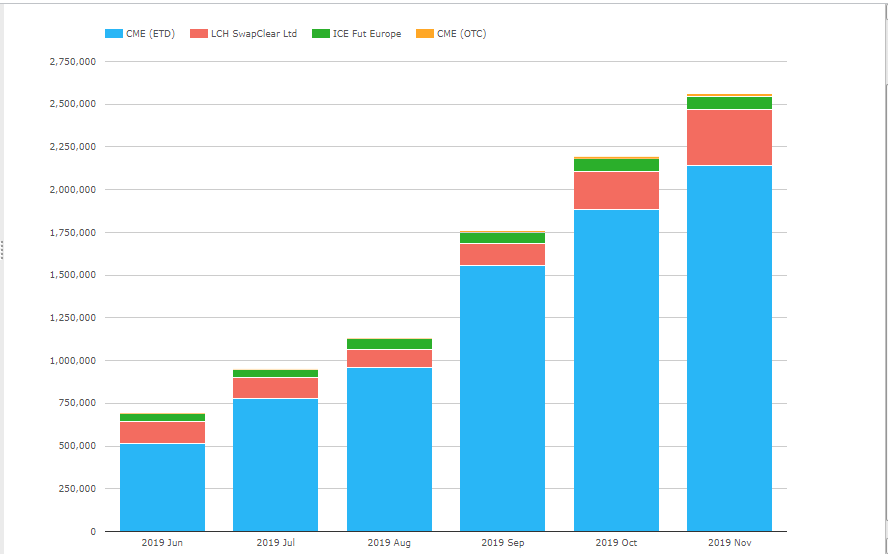

Global Cleared Open Interest

In CCPView, we collect information on all SOFR Futures and Swaps reported by CCPs.

- Showing strong month on month growth

- While not exponential, certainly higher than linear, as evidenced by the jump in Sep 2019.

- CME SOFR Futures have by far the largest OI with $2.15 trillion on November 29, 2019

- LCH SOFR Swaps are next with $330 billion of OI (single-sided notional)

- ICE SOFR Futures with $77 billion of OI

- CME SOFR Swaps with $16 billion of OI

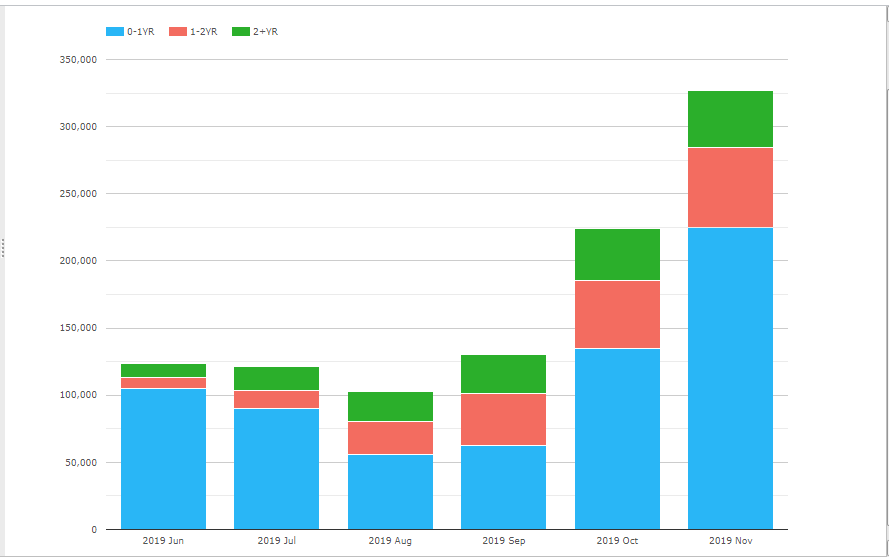

It is also important to get an insight into the tenor, which we can easily do.

Showing the dominance in gross notional terms of 0-1Yr.

As a Swaps Dealer, you should be able to produce the above aggregate views for your own trades and then compare if you are lagging, leading or in the middle of the pack.

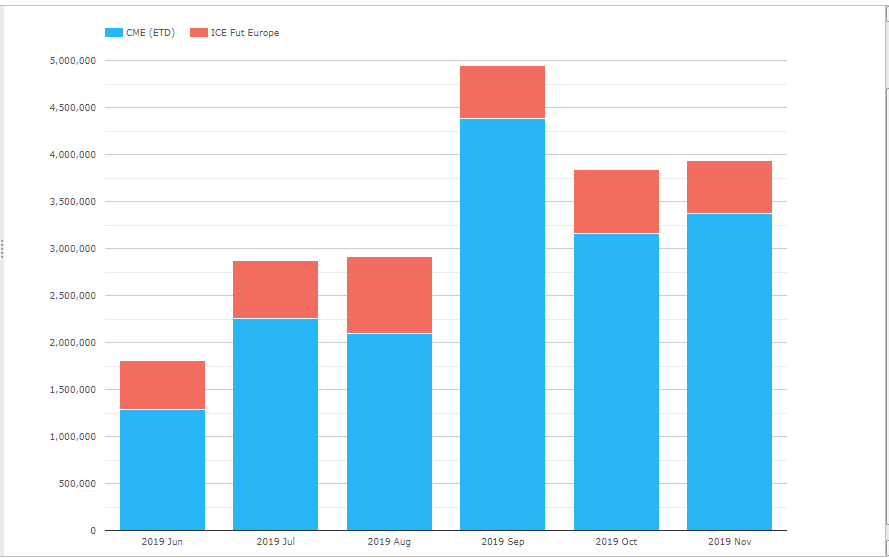

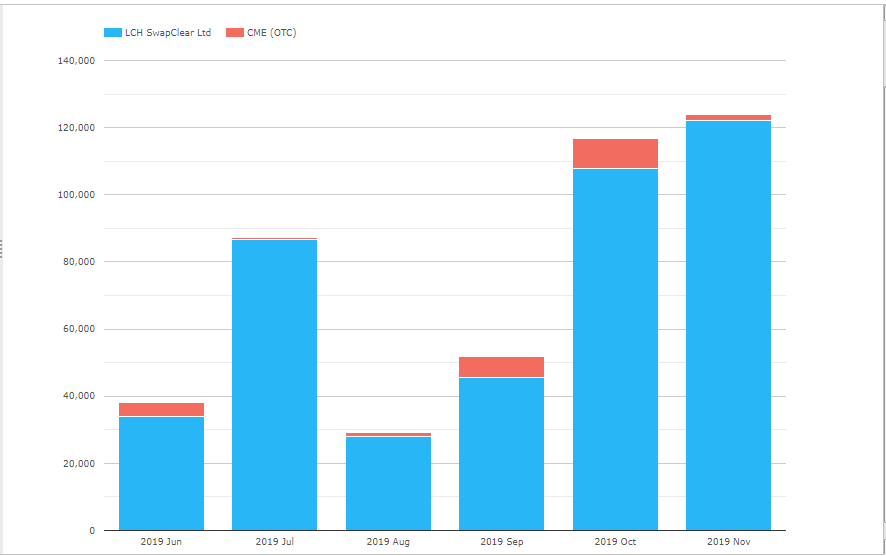

Global Cleared Volumes

CCPView also has monthly volume data, so rather than just open interest/outstanding notional, we can focus on how much is traded each month. Lets do that for Futures and Swaps in turn.

- CME SOFR Futures with $3.4 trillion notional traded in November and a high of $4.4 trillion in September

- ICE SOFR Futures with $560 billion in November and a high of $810 billion in August

- LCH SOFR Swaps (OIS and Basis) with $120 billion gross notional (single-sided), a new high

- CME SOFR Swaps with regular volume, $1.9 billion in November and a high of $8.8 billion in October

As a Swaps Dealer, you should produce the above for your own trading and compare with the market.

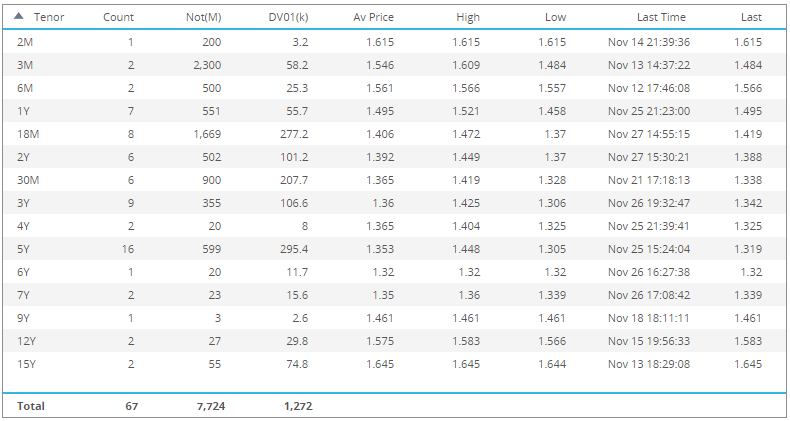

SOFR Trades and Prices

As important are insights into actual transactions; what trades, in what size, at what price, with what t&cs?

In SDRView, we provide such information for the US derivatives market, creating views such as the below.

- An aggregate view by tenor, showing the trade counts, notional, dv01, prices and times of trades

- 5Y with 16 trades, $600 million notional, $295k DV01 (the largest risk tenor), an average price of 1.353%, a high of 1.448%, a low of 1.305% and last traded at 1.319% on Nov 25 15:24.

- 18M, 30M, and 3Y are the next largest tenors by risk traded

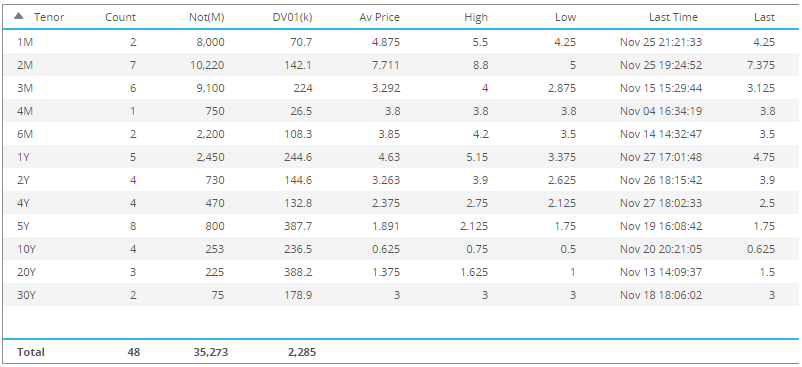

And a similar view for SOFR vs FedFunds Basis Swaps.

As a Swaps Dealer, you firm needs to monitor this transaction data, daily/weekly/monthly to understand what is trading and how your own pricing and trading compares with the market.

Not doing so, could leave you behind the game when dollar swaps liquidity switches from Libor to SOFR.

Execution Venues

Next is is important to how these trades are being executed?

Are they on Swap Execution Facilities (SEFs) or Off venue and if On venue, which SEFs have liquidity in which products and tenors.

We collect this information in our SEFView product, please see my blog SOFR Swap Volumes, for a recent analysis of On SEF vs Off SEF and volumes by SEF venue.

Your firm should analyse this data, decide which SEFs to execute trades on and specifically monitor metrics on your own SEF trading.

Conclusion

Clarus Data Products provide insights into SOFR derivatives, both Futures and Swaps.

For Libor Transition Planning, each firm should collect data on its own trades.

And track if they are lagging, leading or in the middle of the pack.

Not doing so, could result in a missed opportunity or an expensive mistake.

Please contact us to learn more about how we can help you.

Information, analysis and insights are crucial to success.