- We are all repo traders now.

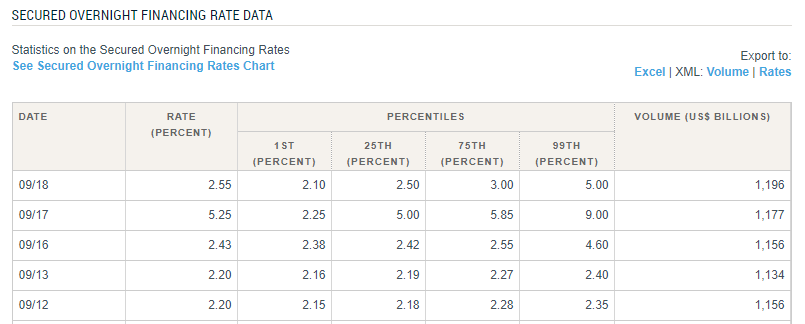

- SOFR has been volatile in the past week fixing from 2.20%, 2.43%, 5.25% (!) before back to 2.55% yesterday.

- We analyse the volumes that make up the fixing and the SOFR IRS volumes.

For those that missed it, SOFR fixed at a scarcely believable 5.25% on 17th September. Surrounding this:

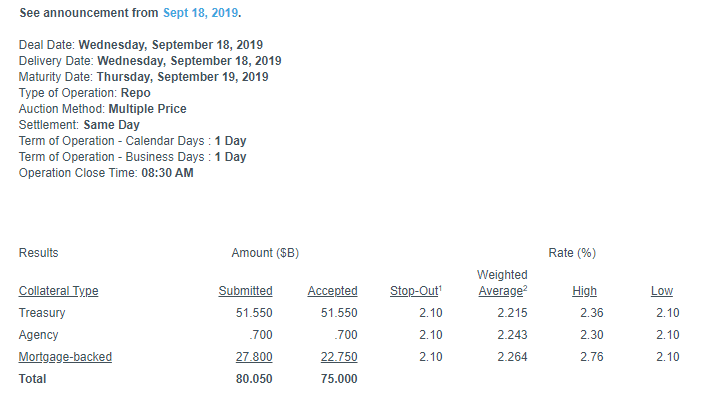

- The Fed has conducted two Repo operations for $75bn each (the Fed lends cash versus eligible securities). These were conducted on September 17th and September 18th.

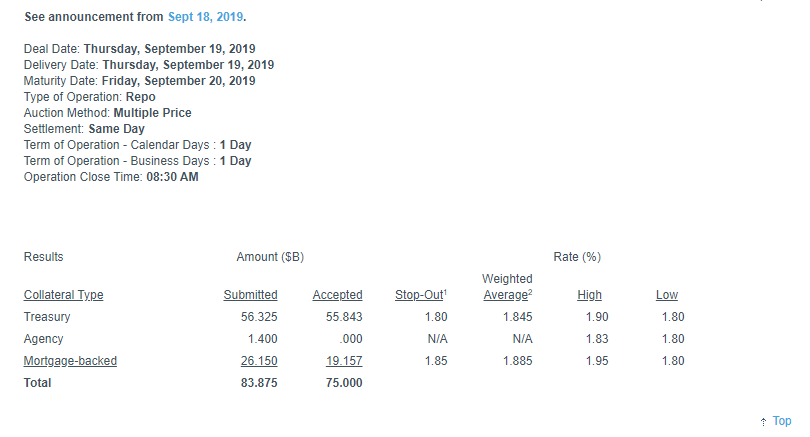

- There will be another repo operation today, September 19th.

The results of these Repo operations are available here, and show that the first operation was under-allocated (just $53bn was lent) whilst the second was over-allocated ($75bn out of a total of $80bn submitted):

Assorted news articles are available on why there is an acute shortage of cash right now – tax dates, net treasury issuance etc. See FT.com:

Analysing SOFR Volumes

All of which means it is a great time to look at the volumes that actually make up the SOFR fixing.

Armed with the research I’ve done for the recent blogs on the short end of USD funding markets (Four Things to Understand about SOFR, USD Fed Funds and the FHLBs) I decided to analyse the SOFR volume data from the New York Fed.

Little did I realise when I wrote my original draft last week how topical that analysis would be!

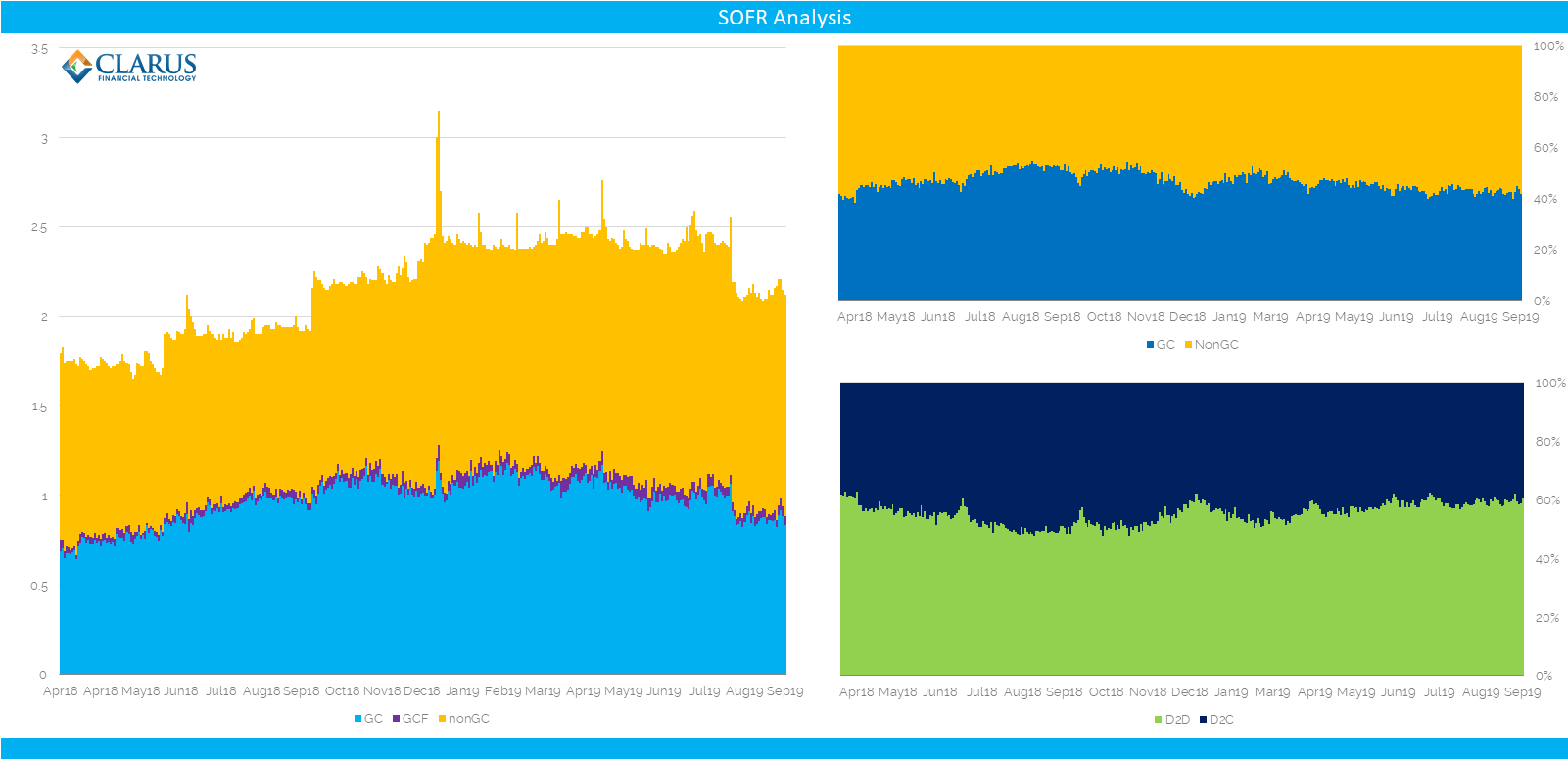

SOFR Dashboard

First off, let’s look at a Clarus SOFR Dashboard:

Showing four charts:

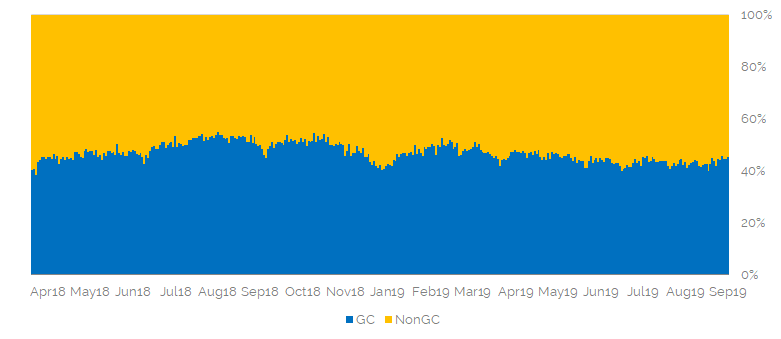

- The main chart shows the volume-weighted components of the SOFR fixing – Tri-Party GC repo, GCF Repo and FICC cleared non-GC repo. If you need a refresher on what these are, check out my previous blog, Four Things to Understand about SOFR.

- We show the portion of the fixing that is made up of GC and how much is non-GC.

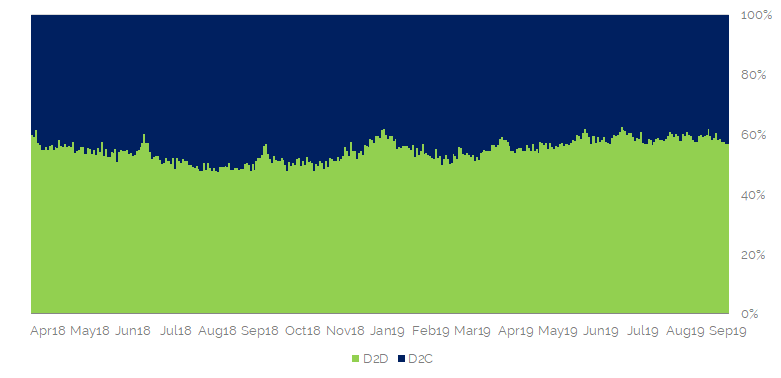

- We also show the portion of the fixing that is made up of interdealer (D2D) and dealer to customer (D2C) trades.

- Finally, we present a time series of the price differential (“basis”) between GC and non-GC components.

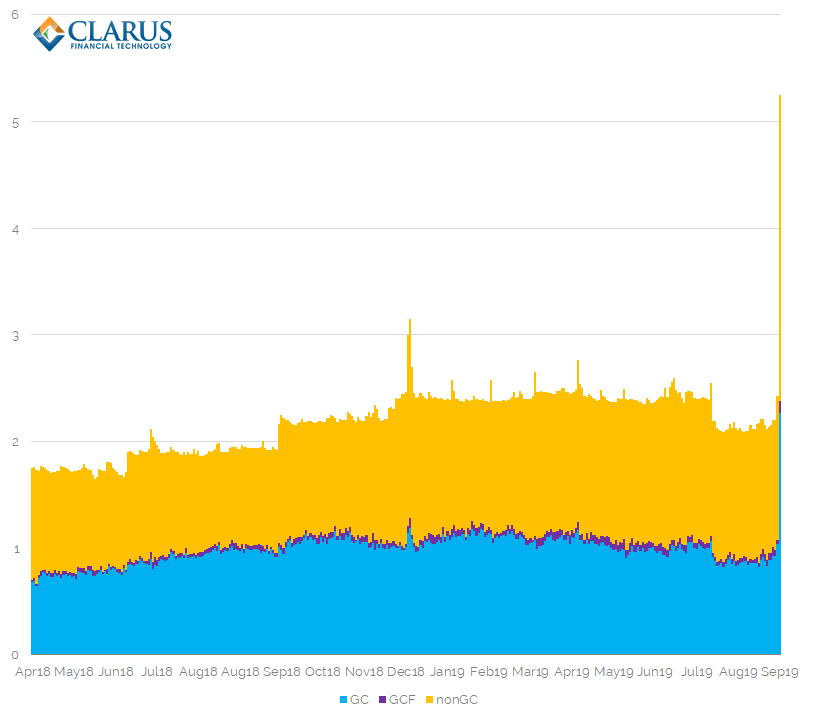

SOFR at 5.25%

Let’s take a look at the fixing itself:

Showing;

- GC and nonGC make up the vast majority of the SOFR fixing on normal days. GCF is a tiny component.

- Yesterday, for the fixing at 5.25%, this was still the case. There are no discernable differences in the past few days in the make up of the fixing.

- Non GC has continued to make up 56% of the fixing.

- GC was still 42%.

- GCF makes up the rest (2-3%).

GC or nonGC?

Was there any change in the overall make-up of volumes between GC and nonGC segments of the market?

- No. The weighting of each market segment has been pretty constant.

- GC makes up 45%.

- nonGC makes up 55%.

D2D or D2C

Was there any change in the overall activity of different market participants?

- No. The activity has been pretty constant.

- D2D makes up 57%.

- D2C makes up 43%.

Did the Basis move?

Was there a large than normal pricing differential between GC and nonGC repos?

- Amazingly, no again.

- The price differential was zero between the two different components.

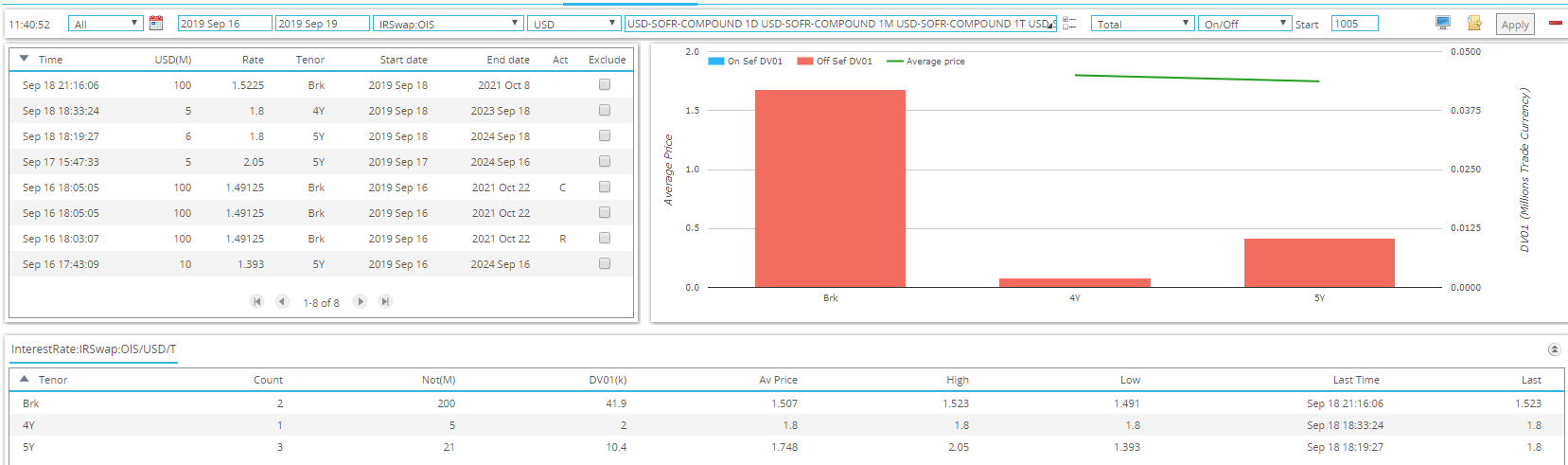

Did Anything Else Happen in SOFR?

There has been no notable uptick in SOFR-linked IRS trading, with just $226m in notional traded in outrights this week:

Showing;

- 6 trades.

- $54k DV01 in risk traded.

- Maturities from 2 years out to 5 years.

- There were also 2 basis trades done this week, totaling $90k DV01 in the 1y and 3y maturities.

And where will SOFR fix next?

Of course this 5.25% fixing should be a one-off event. The tightness in the cash market might last for a few days, but if all of the explanations are to be believed (and the data suggests it is a general shortage), then SOFR should revert back to more normal levels.

Et voila, the fixing was back down to 2.55% yesterday. And breathe:

However, the $75bn repo operation was still over-subscribed today, so expect SOFR to stay elevated for the time being:

Feel free to reach out to us if there is anything else you’d like to see about SOFR.