This week, we take a look at the world of SOFR swaps and some of the intricacies associated with trading these OIS products.

Nuance 1: Reset Lag and Payment Lag (courtesy of the Clarus blog)

Overnight Index Swaps have a peculiarity concerning the fixing date (or publication date) of the underlying overnight rates. The fixing date can be later than the effective date of the rate.

This is in contrast to a classic LIBOR fixing.

For example USD LIBOR has a -2D fixing lag, whilst SOFR has a fixing lag of +1D. The need for this payment lag is pretty obvious for USD markets. For example, suppose the calculation period end date is 2022-04-08, in which case, the last SOFR rate in the calculation period is for the period (2022-04-07, 2022-04-08) and its value is not published until the morning of 2022-04-08. There may not be enough time on 2022-04-08 to compute and agree the compounded rate for the entire calculation period and make the settlement in time (particularly for counterparties outside the US).

Therefore, for practical reasons it is quite natural to require the payment on some day after the calculation period end date, hence a payment lag arises. The table below highlights the conventions in USD markets.

| CCY | ISDA/FpML Code | Fixing Lag (D) | Payment Lag (D) | BBG Ticker |

| USD | USD-FEDERAL FUNDS-H.15-OIS-COMPOUND | +1 | +2 | USSO* |

| USD | USD-SOFR-COMPOUND | +1 | +2 | USOSFR* |

Nuance 2: Day Count Conventions

As and when (if?) liquidity transitions from LIBOR-based swaps to SOFR-based swaps it will also impact payment schedules:

- Most USD LIBOR swaps are traded on a “Semi-Bond” basis. The fixed leg of the swap is transacted with Semi-Annual payments, calculated using a 30/360 day count convention (DCC).

- USD LIBOR swaps can also commonly trade “Annual Money”. The fixed leg of the swap is transacted with Annual payments, calculated using an Act/360 DCC.

SOFR swaps are different:

- A Fixed-Float SOFR swap trades with annual payments on each side. The annual payments are calculated using an Act/360 DCC.

Whilst existing LIBOR-based swaps utilising the ISDA fallbacks will not see any change to their payment dates, new swaps written against SOFR will look and feel different to your current LIBOR operations.

Nuance 3: Payment Frequencies

USD LIBOR swaps typically have different payment frequencies on each leg:

- A Semi-Bond trade has semi-annual payments on the fixed leg versus quarterly payments on the USD LIBOR 3M leg.

- An Annual-Money trade has annual payments on the fixed leg versus quarterly payments on the USD LIBOR 3m leg.

SOFR swaps are different – and in this case almost certainly better:

- Both legs of a Fixed vs Float SOFR swap have annual payments.

- This is great because, for uncollateralised trades, it reduces the credit risk of the swap. All of the accrued interest amounts are paid at the same time.

- Operationally, it is also a great thing. Assuming you are operating under a netting agreement, you only have to exchange a single cash-flow once a year. No need to gross settle the coupons.

- From a Variation Margin perspective, this is also a good thing. The big changes in mark-to-market associated with coupon drops will disappear, reducing your collateral in transit.

Nuance 4: Your Pricing Screens are about to change

I’m sure we are all primed and ready for the CCP discounting switch to SOFR on October 16th, aren’t we?

In case you need a refresher, both the LCH and CME materials (I’m sure other CCPs have them as well…) are very informative.

But have we all considered what happens on the morning of Monday October 19th?

- All USD swaps screens that you consume are no longer discounted at Fed Funds. They are now discounted at SOFR.

- Any cleared USD swap that you transact is discounted at SOFR (admittedly this has been the case for the future value of all cash-flows after 16th October in theory for a while now, but the change in October cements this).

- Any movement in the mark-to-market of your cleared USD swaps portfolio will now result in new SOFR risk being created each day. This is the “discounting risk” that is far from static and may need to be re-hedged after large market movements.

Nuance 5: Some Products Will Fundamentally Change

Finally, it is worth pondering the impacts to some particular products that are traded. What does a Spreadover mean if the floating leg is SOFR for example? Market participants have traditionally traded Spreadovers versus LIBOR-based swaps. A term credit index versus government funding. What could these swaps look like in the future? A SOFR vs US Treasury rolling contract could be something very different.

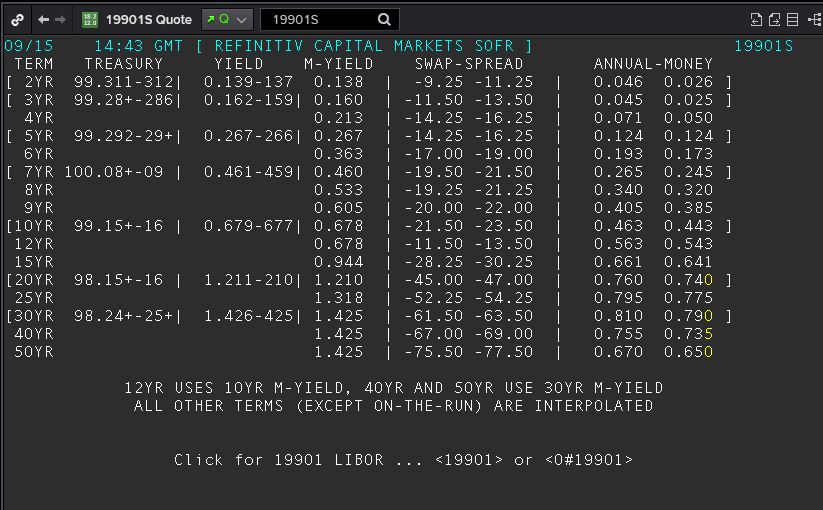

Talking of which, ICAP were kind enough to send me their latest page, 19901S, which takes their “traditional” 19901 page for Spreadovers and translates it into a SOFR world. It makes for very interesting reading – I’ll follow up with a blog on this next week:

In the first table, I believe the title of “Fixing Lag (D)” actually meant “Publishing Lag”.

the fixing lag, or reset lag should be 0.

Hi Leon, thanks for the comment and I follow your logic. For EFFR and SOFR ‘Fixing Lag’ is indeed a publication lag. However, we choose to refer to ‘Fixing Lag’ to compare with dates commonly associated with LIBOR. Hope that makes sense?

The reformed SONIA is published T+1 similar to the case of SOFR, but according to Bloomberg SONIA OIS does not have any payment delay, which is different from SOFR OIS. Would you share how SONIA OIS tackles the challenge of publication lag of the reformed SONIA?

This is highly informative. But the conventions which are described above pertain to standardized swaps. There are definitely more DCC based on ISDA and others. Can you also write a few things around ?

1. How the yield curve will change ? projection vs discounting ?

2. Is SOFR term structure fully available now like LIBOR ?

3. Won’t the payment lag need to adjust for additional payment period ?

4. Finally the spreadovers..