- The new SONIA benchmark becomes effective 23rd April 2018.

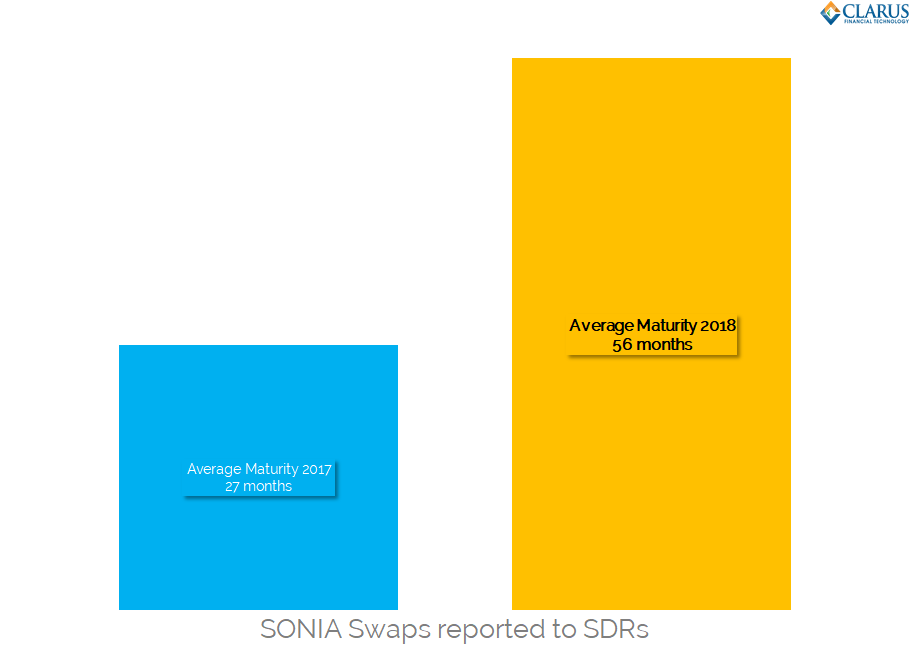

- The average maturity of a SONIA swap has doubled in 2018.

- Is this increase in duration evidence of a behavioural change in markets?

SONIA Reform

Regular readers will know that SONIA has been subject to a Consultation by the Bank of England, with the intention of reforming the index so that it can be the most robust Risk Free Rate possible for Sterling Rate markets. As a result;

- As of April 23rd 2018, the Bank of England will produce SONIA.

- Transactions used to calculate SONIA will include overnight unsecured transactions negotiated bilaterally and via brokers.

- Averaging methodology will change to a volume-weighted trimmed mean.

- SONIA will be published the following working day at 9am UK time.

Details are set out on the Bank’s website.

As well as changes to the index, we are also interested to see if trading can transition away from Libor-based instruments to SONIA based instruments. We take a look at the current state of trading, with a view that we will periodically update our volume findings. One day, we might even be able to draw upon MIFID II data….

SONIA Volumes

We have recently upgraded SDRView to include DV01 calculations for OIS swaps. This is particularly handy when looking at the transition for long-dated instruments from Libor to OIS trading.

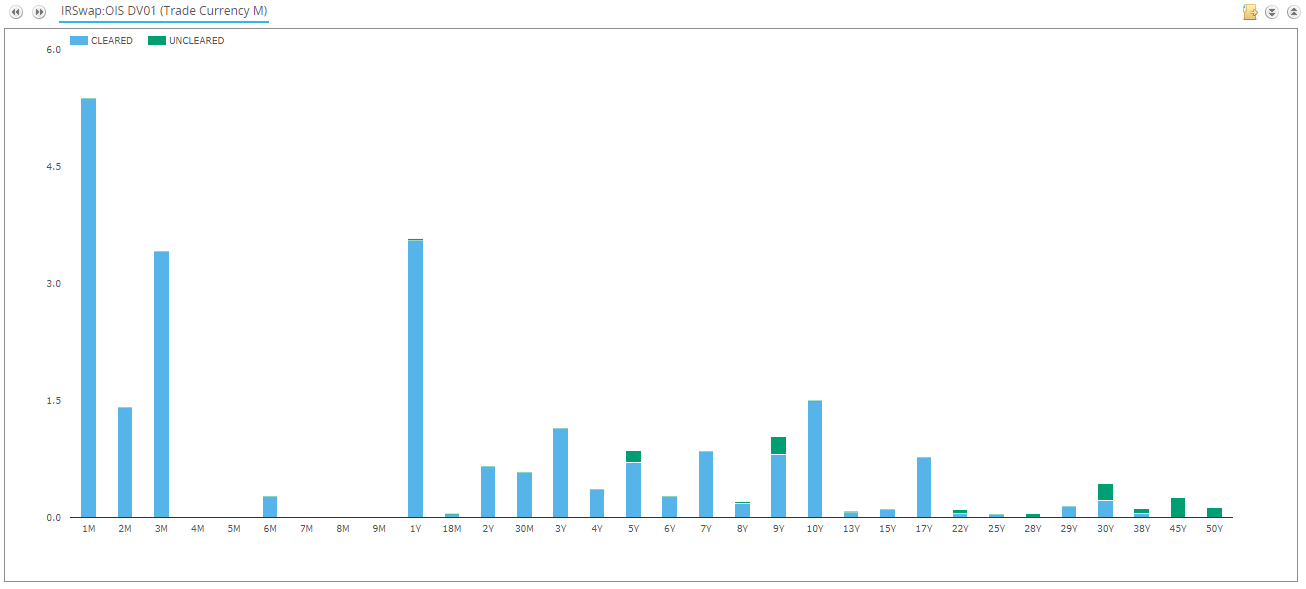

So in 2018, what does the maturity profile of Sonia trading look like?

Showing;

- The total DV01 traded for SONIA swaps in each maturity bucket so far in 2018.

- 1 month is the most traded tenor, closely followed by 1 year and 3 months.

- Interestingly, 10 years is the 4th most traded tenor. This year, it has had an average daily volume of £27,000 DV01.

- The total Average Daily Volume for SONIA swaps (as reported to US SDRs) has been £424,000 DV01.

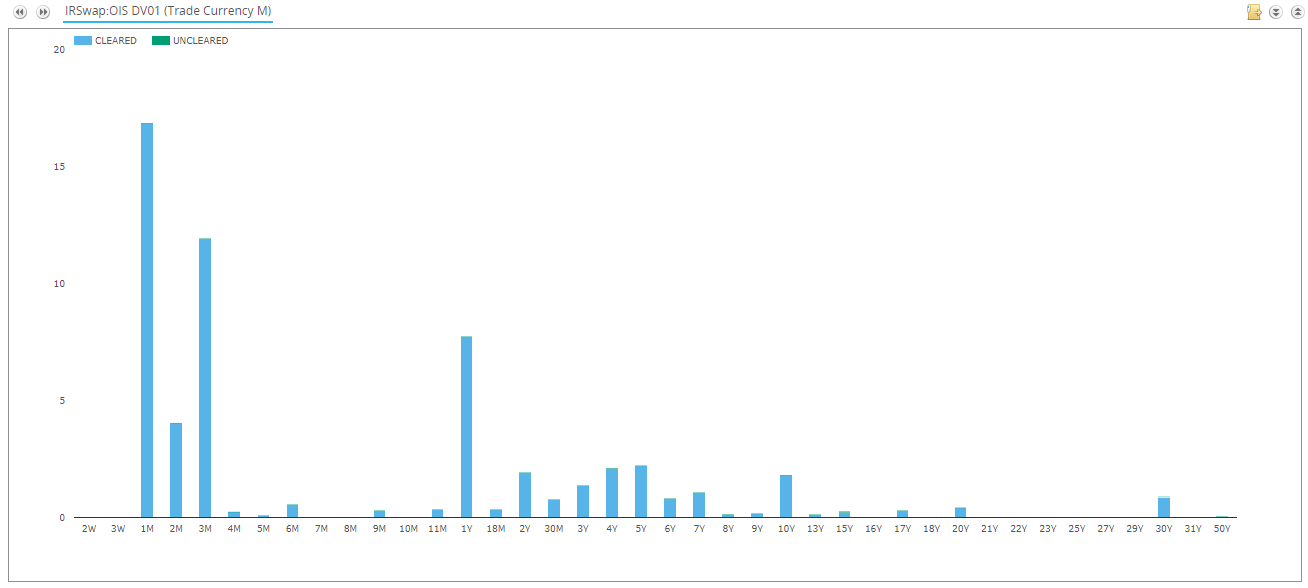

How does this compare to 2017? The same chart but for 2017 is below:

Showing;

- 1 month was the most traded tenor, followed by 1 year and 3 months.

- 10 years was only the 10th most traded tenor. Average Daily Volumes were half as large as 2018, at only £14,000 DV01.

- The total Average Daily Volume for SONIA swaps was £436k, within 3% of the 2018 average.

Drilling down into the differences between 2017 and 2018, we see a big jump in the average maturity:

As you can see from the first two charts, the changes in risk profile are relatively small. Nevertheless, the duration of the SONIA market has doubled this year. The market is slowly becoming less focussed on the short-end:

As you can see from the first two charts, the changes in risk profile are relatively small. Nevertheless, the duration of the SONIA market has doubled this year. The market is slowly becoming less focussed on the short-end:

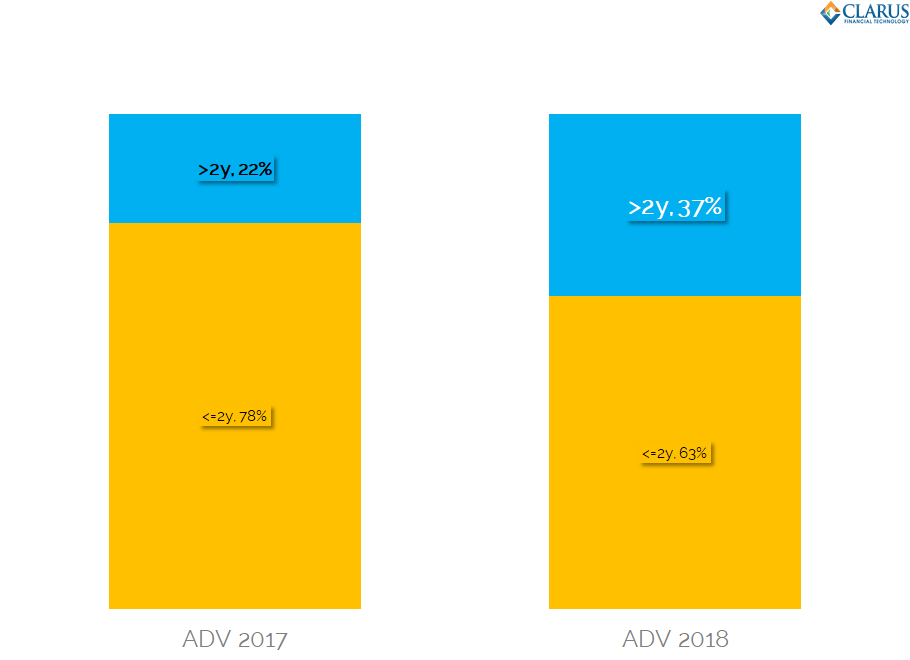

Showing;

Showing;

- The proportion of DV01 traded each year, divided into the short-end (2 years and less), and the long-end (over 2 years).

- In 2017, 78% of SONIA risk was traded in swaps with tenors less than 2 years.

- In 2018, this has shrunk to just 63% of risk.

- The increase in average duration for SONIA swaps has therefore been driven by this 15% of risk shifting to maturities longer than two years. That is a large shift in trading patterns.

LIBOR Volumes

We are also interested in relative changes to the Libor market. The first thing to state is that we haven’t seen this shift in average maturity in the Libor market. In 2017, the average maturity was 135 months. In 2018, it is 141 months. Lengthening duration is very much a SONIA market phenomenon.

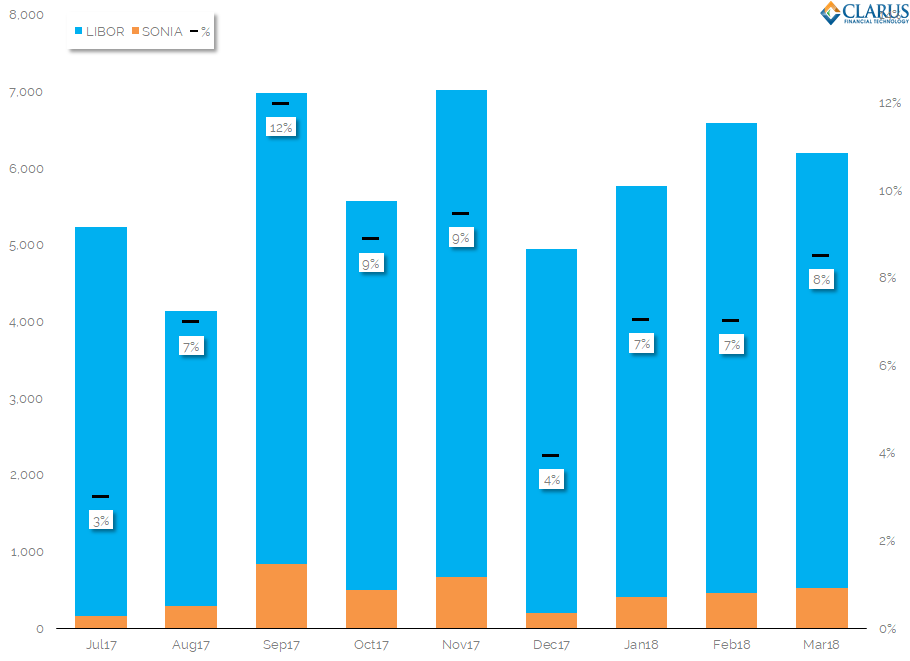

What about overall volumes? Is SONIA trading more popular than ever?

This chart shows the overall risk traded in GBP products, along with the percentage of risk that is SONIA-denominated. Overall, we can say that:

- 2018 has seen 8% of risk traded as a SONIA product.

- This was the same in 2017 (7.5% vs 7.8%).

- September 2017 marks the recent highs in SONIA volumes, when 12% of total risk was SONIA-denominated.

- September saw average daily volumes of SONIA at £835,000 DV01.

- However, LIBOR based products have an average daily volume of £5.7m in 2018. Still some way to go for SONIA trading.

Cleared Volumes

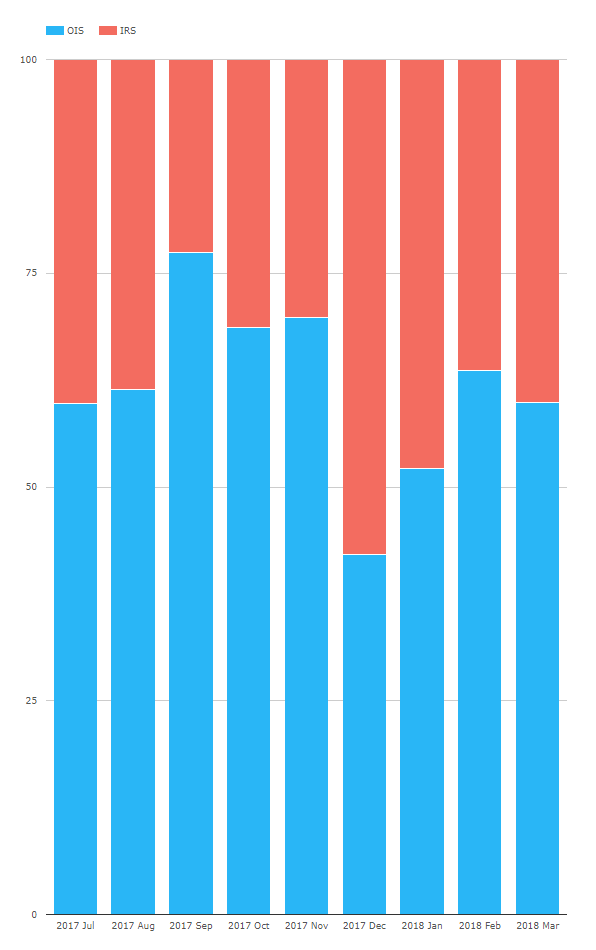

SDR data covers a portion of the GBP IRS market. CCP data, however, covers the entire global (cleared) market. Whilst we cannot calculate DV01s for CCP data (as it is not provided in granular detail), we can at least monitor notionals traded. For GBP swaps:

Showing;

Showing;

- The percentage of notional cleared at CCPs as either an IRS (red) or an OIS (blue) for GBP swaps.

- March 2018 has seen 60% of GBP notional cleared as an OIS swap (excluding basis swaps).

- In 2017, 67% of notional was SONIA based.

In Summary

- The average maturity of SONIA swaps has doubled in 2018.

- Volumes have remained fairly static as a percentage of overall trading.

- SONIA reforms will be complete as of April 23rd 2018.

- We will check back in after this date to see if it motivates any further changes to trading behaviour.