- There are two parallel branches to the SONIA reforms.

- One is to modify how the rate itself is being set.

- The other is to promote its’ use as the near Risk Free Rate for GBP derivative markets.

- We take a look at current SONIA markets.

*Updated 18th May 2017 to correct the use of trimmed-mean (not median) for Reformed SONIA, with current SONIA volumes.

SONIA Reform – The Data

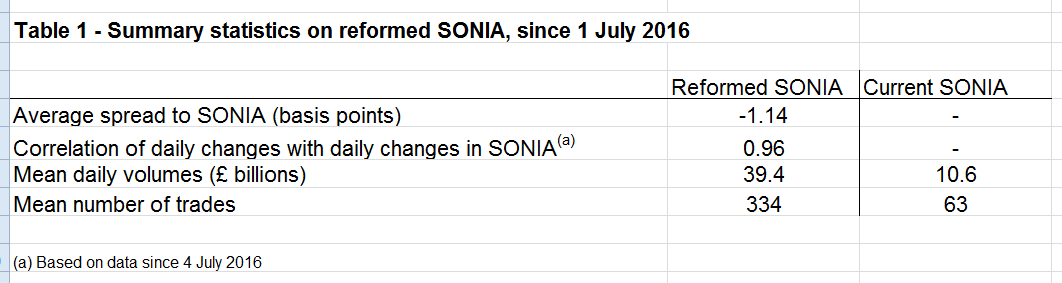

The Bank of England are leading the reform efforts for SONIA. Helpfully, they provide the actual data used to assess the intended reforms to the benchmark. The table below summarises the results of their empirical study:

Showing;

- The changes in how SONIA is both collected and calculated resulted in a fixing that was, on average, 1.14 basis points lower than the old methodology during the second half of 2016.

- The new methodology has a very high correlation with the old methodology at 96%.

- During the sample period, the average daily volume of qualifying trades in the reformed SONIA benchmark was nearly 4 times greater than previously.

- It is worth noting however that recent SONIA volumes in 2017 have been higher than during the sample period (at around £15-18bn).

On these last two points, it is important to note that the BoE has proposed to calculate Reformed SONIA as a “trimmed-mean”, based on the middle 50% of rates. This should make it less sensitive to outliers than a median calculation, hence the methodology.

The change to “Reformed SONIA” will happen early next year (March or April 2018). The details of the changes are:

- A change to a trimmed-mean, “calculated as the volume-weighted mean rate, based on the central 50% of the volume-weighted distribution of rates”.

- An expansion to include bilateral as well as brokered trades. Trades must still be over £25m in size.

For those interested readers, there is a great summary in Box 1 of the Bank’s March 2017 consultation paper, along with lots of data on the actual fixings here and here.

SONIA Reform – Market Take-Up

As we looked at with Euribor reform last week, improving the fixing methodology is part of a two-pronged approach to improving our Rates markets. As well as these methodological changes to the fixings, regulators around the world are promoting the use of risk-free interest rate benchmarks (RFRs).

In light of which, it was interesting to see that the BoE last month announced that the Working Group on Sterling Risk-Free Reference Rates had chosen SONIA as its’ preferred benchmark. According to the press release:

This expression of market support for SONIA will act as a platform for further work to broaden and promote its use as an alternative to sterling Libor

The two candidates that could have replaced SONIA were £SONET (FTSE-Russell administered) and £RIR (Nex administered). These two other indices are based on secured transactions – i.e. the repo market. I wonder if swap dealers the market over breathed a small sigh of relief that they can continue discounting at (unsecured) OIS rather than secured.

SONIA Market – The Data

With these upcoming changes and a regulatory tailwind, the outlook for SONIA markets looks pretty rosy. There are no solid timelines for when markets are expected to shift away from Libor to SONIA, so I thought we should start the conversation rolling by looking at the current state of play.

How dominant is Libor in GBP Rates markets at present?

SDRView Data

From SDRView, we can take both trade counts and trade notionals to estimate what percentage of the entire market is SONIA-based versus Libor-based.

Showing;

- Percentage of notional traded vs SONIA on the left hand axis.

- Percentage of number of trades transacted vs SONIA on the right hand axis.

- SONIA swaps are already a significant portion of the overall GBP Rates markets.

- On a notional basis, the percentage of total notional traded can, in some months, be over 80% linked to SONIA.

- However, this notional measure is highly volatile, dropping as low as 20%.

- We therefore prefer to consider trade count as a more reliable measure of SONIA market activity.

- SONIA trades account for between 5-15% of activity during any given month.

The spike in SONIA activity last year coincided with Brexit, as market participants hedged any monetary policy responses from the BoE. Relative activity in SONIA markets has dropped since, with no sign that markets are naturally moving towards SONIA as their benchmark of choice.

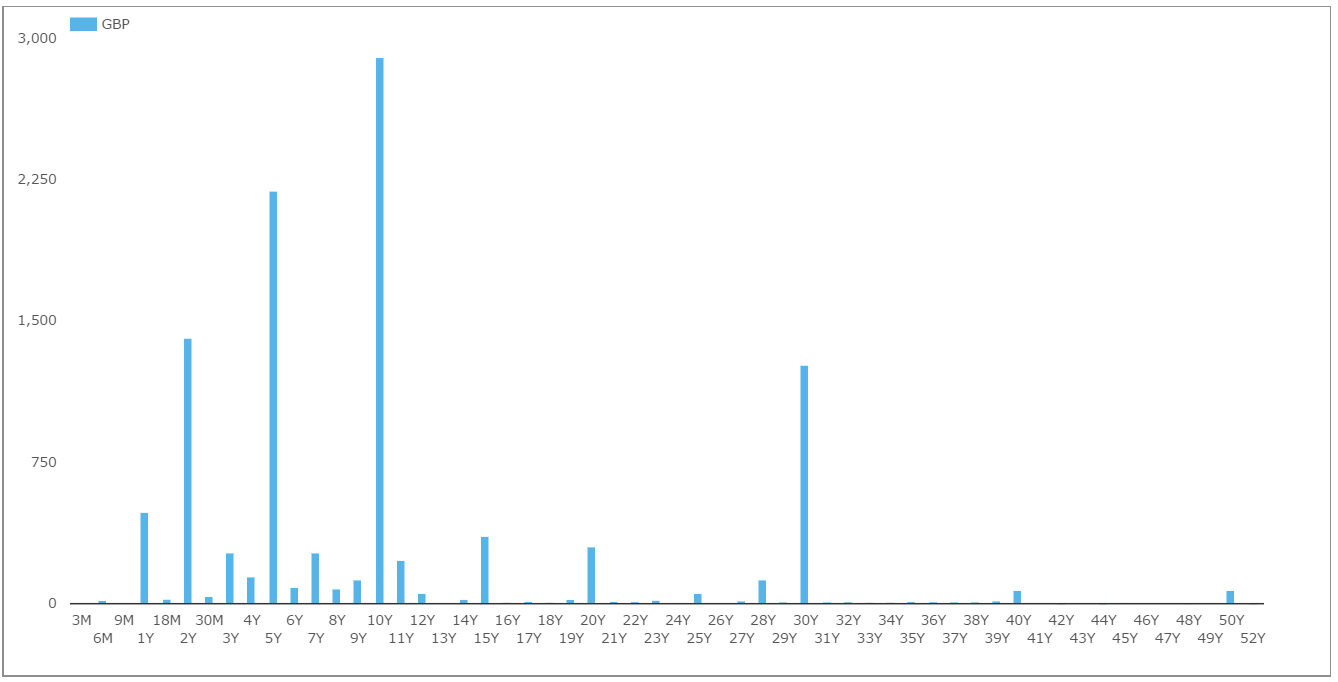

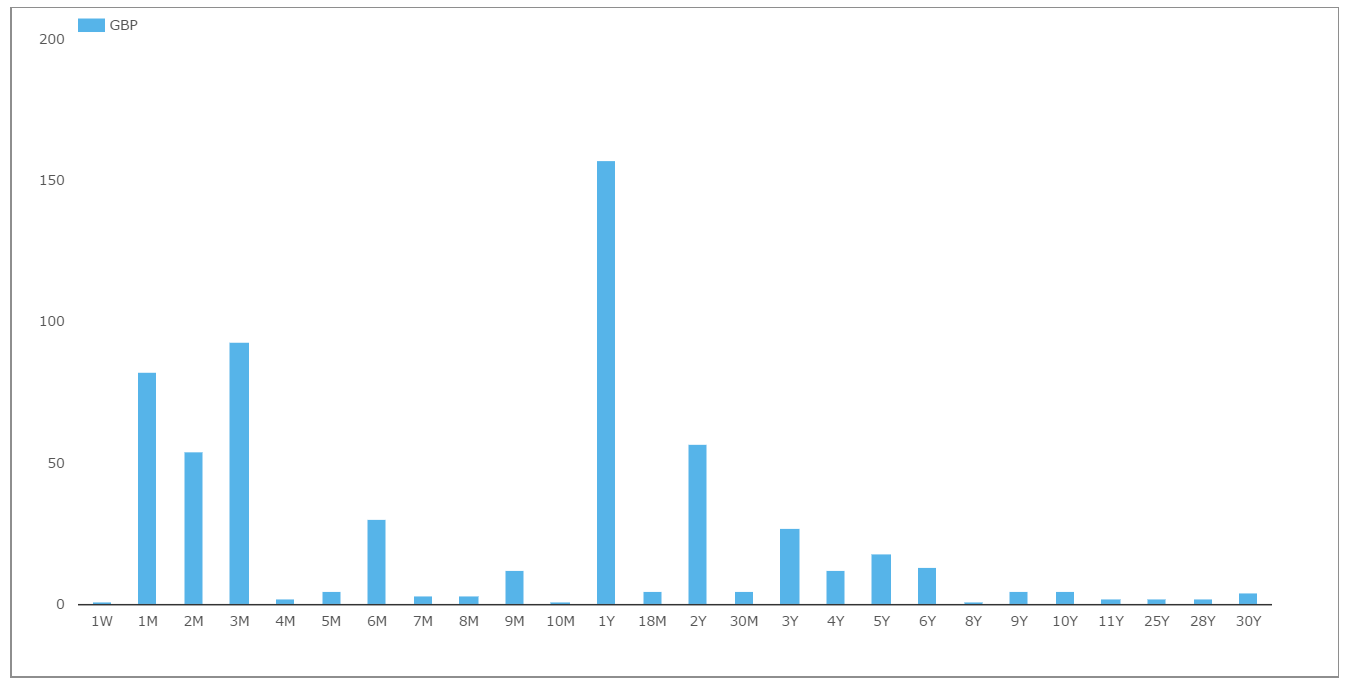

Tenor Profile

As a 30-second primer on the SONIA markets, here are a few key numbers to put the SONIA and Libor markets in perspective. From our SDR data, we see that:

- SONIA average trade size is £1.1 billion.

- SONIA weighted average maturity is 4.3 months.

- LIBOR average trade size is £48.5 million.

- LIBOR weighted average maturity is 65.3 months.

Consistent with other OIS markets, we can therefore say that SONIA trades relatively infrequently, in large notional size, but short maturities.

The two charts below show the Tenor profile on a trade-count basis for both SONIA and LIBOR markets:

These charts paint a fairly clear picture. For markets to fully transition to SONIA as the benchmark of choice, liquidity in maturities greater than 2 years will have to be transformed.

CCPView Data

Finally, we can take a look at the global Cleared markets in SONIA and LIBOR in CCPView. CCPView data paints the same picture of GBP Rates markets as we found in SDRView (which represents around 30% of the total cleared GBP Rates market).

CCPView provides an added element of granularity over and above SDR data – a split between Dealer and Client activity:

Showing;

- The percentage of overall GBP cleared notional that is SONIA-linked for both Dealer and Client activity.

- Virtually all of this is cleared at LCH.

- Dealer activity and Client activity seem to move together.

- Can both Client and Dealer liquidity pools therefore be motivated to move concurrently towards SONIA? Time will tell.

Other Market Impacts

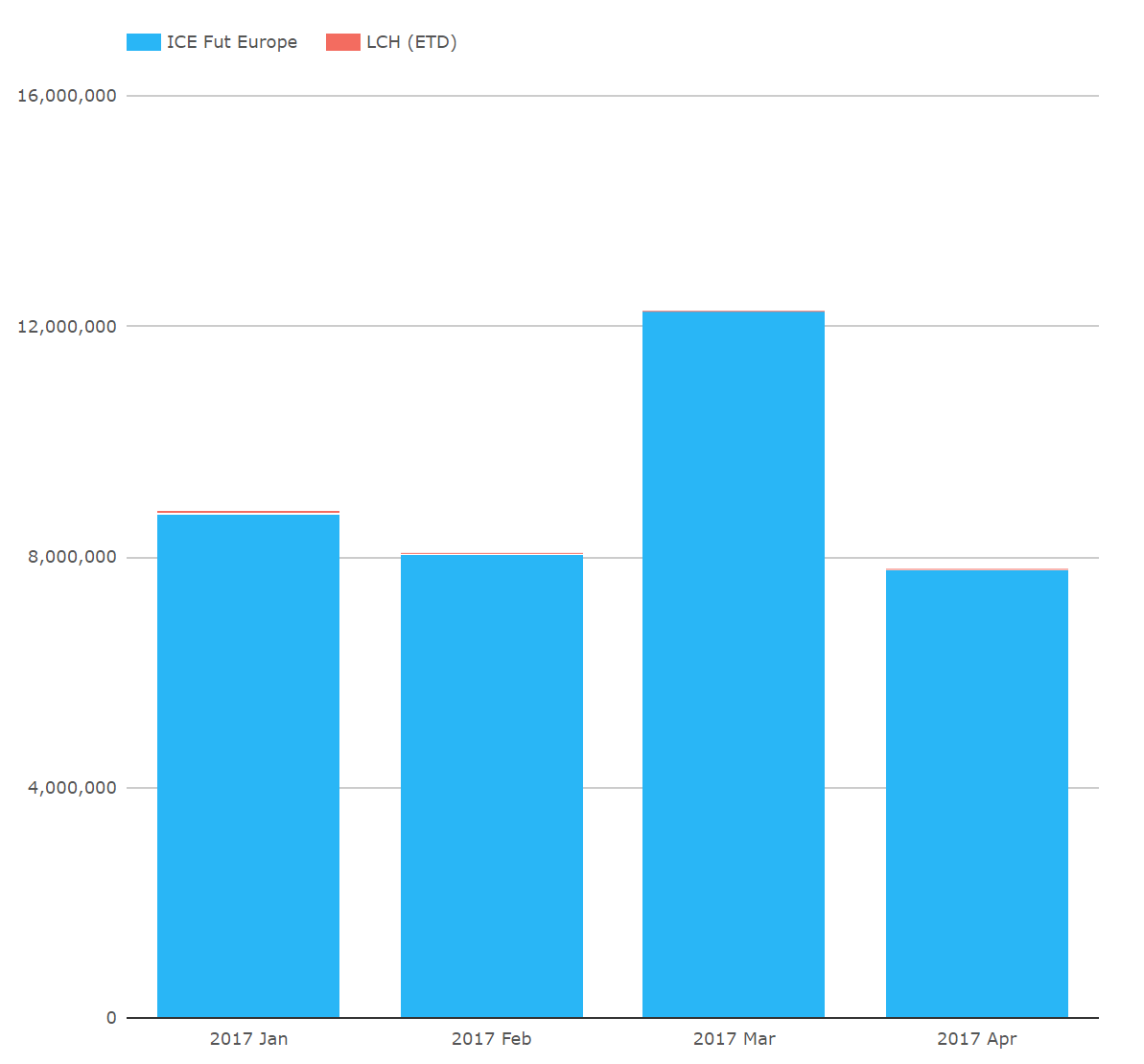

Talking of liquidity, there is another huge pool of LIBOR-based liquidity – futures. In the case of GBP STIRs, we are talking about ICE (LIFFE) futures.

Showing;

- A significant pool of LIBOR-based liquidity.

- These 3 month GBP LIBOR based products trade over $8trn notional equivalent each month.

- Due to the high velocity nature of futures markets, these notional amounts are clearly much higher than the turnover we see in OTC land.

- Nonetheless, this is also a sign of just how liquid these products are.

- To speed the take-up of SONIA at the expense of LIBOR, some type of SONIA-based futures liquidity pool would hence be a “nice-to-have” in the future.

What would a SONIA-based future look like? We have examples of monthly Fed Funds contracts in the US to reference. Or we could imagine a future that cash-settles against e.g. 3 month or 1 month SONIA. Or versus MPC-dated SONIA trades.

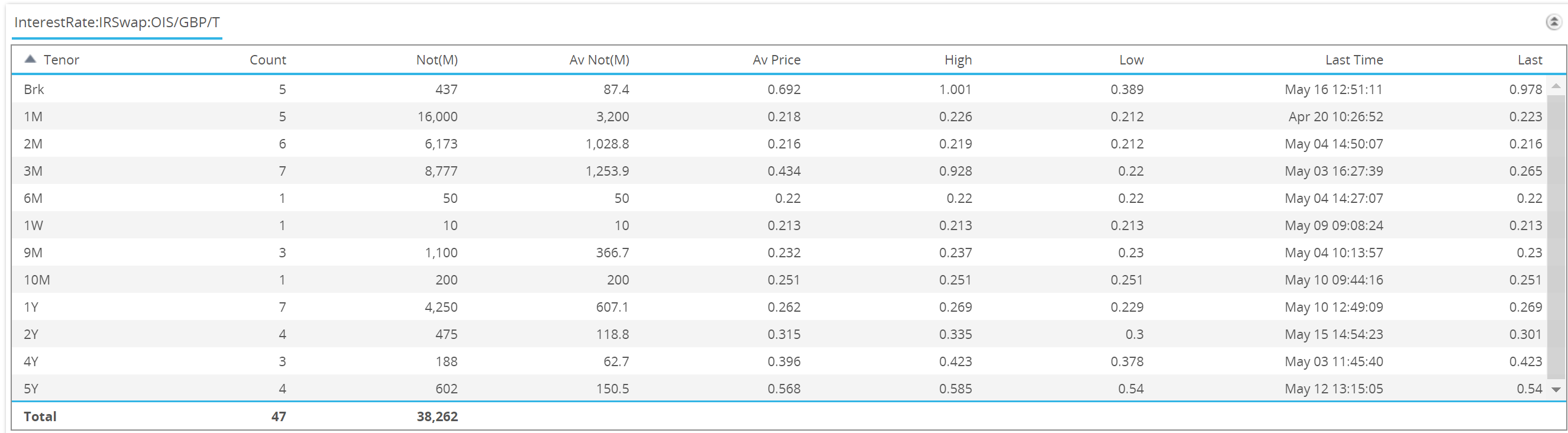

However, when we look at the trade level data for the last month in SDRView:

Showing;

- All SONIA trades reported by US Persons to the SDRs in the past month.

- This includes forward starting structures up to 6 months in the future.

- Sadly, even with this fairly broad search criteria we only see seven 3-month SONIA trades.

- Not enough to base a futures contract against!

- Again, we are left searching for meaningful European trade-level data to help inform market infrastructure.

In Summary

- The fixing process for the SONIA benchmark will change in early 2018.

- The market is looking at ways to promote SONIA as the benchmark rate against which Interest Rate Derivatives should be traded.

- OTC swaps already see between 5-15% of trading against SONIA.

- A large pool of LIBOR-based liquidity exists at ICE in the form of STIR futures contracts.

- It would be beneficial for the OTC market if this liquidity pool could also be motivated to move towards SONIA based structures.