The recent announcement of the ICAP and Tullet deal (see ICAP’s statement) has resulted in a lot of press coverage, see Financial Times (subs required) or The Guardian or Bloomberg for details.

The transaction will result in Tullet taking over ICAP’s brokerage business (with ICAP retaining a minority stake in the Tullet Prebon Group) and ICAP focusing on its electronic and post-trade business (EBS BrokerTec, TriOptima, Traiania, Reset, Rematch). The result will be what some analysts have been calling for; namely greater scale and cost synergies in the brokerage business and a pure electronic technology business with a higher price earnings multiple.

In this article I will look at the impact on market share of the brokerage business, in a similar manner to our article on the BGC Acqusition of GFI, and do so using the data we have on US volumes.

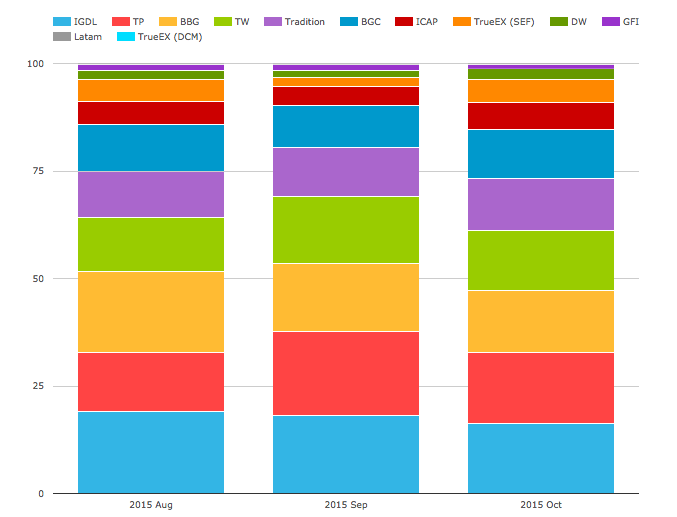

IRD Market Share

Using SEFView lets chart IRD volumes for all currencies and all products (exc. FRAs) for the past 3 months.

Which shows that in percentage terms, the bottom blue (ICAP’s IGDL entity) combined with the red (Tullet) is just over the 30% market share threshold and that is without including the ICAP in brown further up the chart.

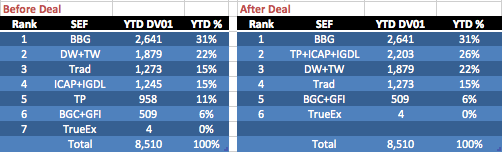

Lets now look at our regular market share metric.

Interest Rate Swaps only including Vanilla, Basis and OIS Swaps and using DV01 (in USD millions) for USD, EUR and GBP. (This time from 1-Jan to 30-Sep 2015).

Showing that after the deal the new Tullet entity will jump to second position with 26% share.

This is up from fourth for ICAP (or third if we were able to adjust for packages) and fifth for Tullet.

So a very significant increase and close to Bloomberg’s leading position.

And specifically for OIS Swaps and Basis Swaps, we know from my USD OIS Swap Volumes and Basis Swap Volumes blogs that ICAP and Tullet are currently No 1 and No 2 for these. Combining their respective shares will mean more than a 65% share for each product, surely a dominant position.

It would also be interesting to look at share in Swaptions, FRAs, Inflation Swaps, CapsFloors and Exotics, but I will leave that for those of you interested to do yourself in SEFView.

CRD and FXD

And what of Credit Derivatives and FX Derivatives?

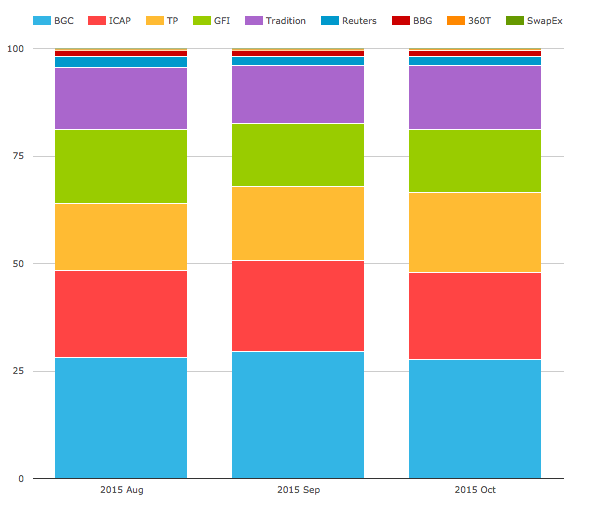

Well neither ICAP or Tullets has much share in Credit, so lets look at FXD for the last 3 months.

Showing that:

- BGC has the largest share at 28.5%

- ICAP and Tullets are next with 20.6% and 17.1%

- Combining these will move them to No 1 with 38% share

- So again a significant move

- GFI and Tradition follow next with 15.5% and 14.3%

Summary

The proposed ICAP and Tullet deal has a massive impact.

The combined brokerage business will move to No 2 in IRD and No 1 in FXD, at least using US SEF data.

Without access to European data, we cannot categorically say what the Global rankings will be.

But most likely these will be similar to the US.

Given the overlap in ICAP and Tullet, it is inevitable that headcount will be cut.

30% reduction in costs have been mentioned in the press.

However competing with Bloomberg and its different pricing will remain a challenge.

The Top 4 firms in IRD in the US will have a cumulative share of 94%.

So are we at the end game for consolidation in this space?

Or will we see Tradition, TrueEx and BGC in further deals?

I would think there is more to come.

Only time will tell.