- There was a huge move lower of 30 basis points in short-dated cross currency swaps on Thursday September 28th.

- This is because the “front roll” went over the turn of the year date.

- There is a huge disconnect for turn of the year pricing between USD Libor and Cross Currency basis.

- USD overnight interest rates of 16% are implied by Cross Currency Basis for year-end 2018!

The Basis Impact

The start of this year was all about the Libor-OIS basis “blow out“. That has since receded. We looked at the time to see how Cross Currency Basis was reacting. The “true cost” of the basis is now mainly thought of in OIS terms, but the headline figures (and most liquid products) continue to be Libor-denominated swaps.

Even by the standards of Cross Currency Basis, 2018 has seen a pretty wild ride. I love this tweet:

Once or twice a year, cross-currency basis swaps do crazy things.

Today is one of those days. pic.twitter.com/B6o4hdQscm

— Brian Chappatta (@BChappatta) September 27, 2018

Three month JPY-USD basis (JPY 3m libor vs USD 3m libor) is shown in the tweet. You’ve got to love the craziness of the jumps on 28th Dec 2017 and then on 28th Sep 2018. These price gaps are both related to the “turn-of-the-year” effect.

What Happened this time?

To recap the price behaviour, short-dated cross currency basis had been trundling along in a tight range, within a couple of basis points, for the last month. Then, at the start of the day on September 28th:

- 3 month EURUSD traded down from -15.25bp to -39.25bp. That’s quite a gap!

- 3 month JPUSD traded down from -24.5bp to -55bp. Crikey!

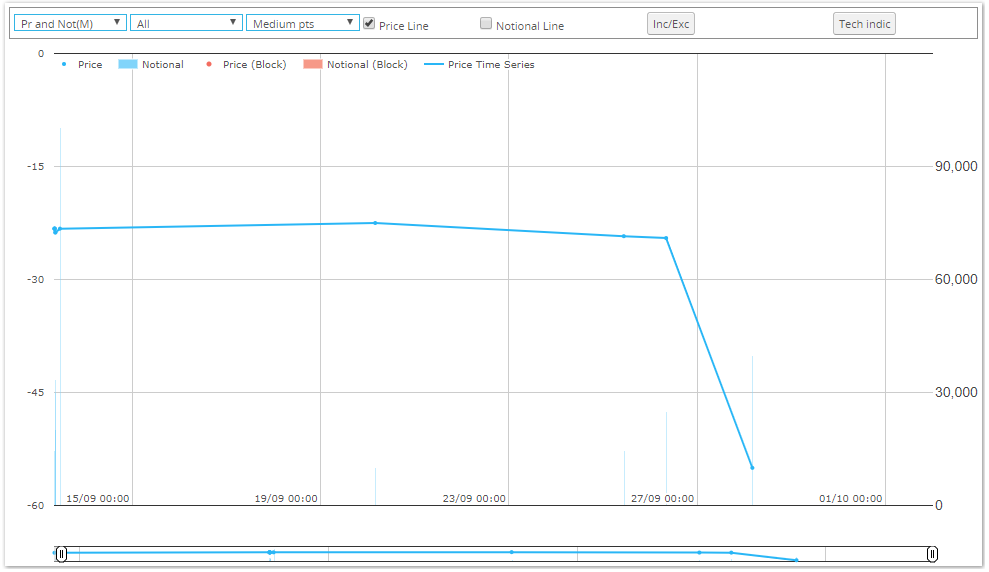

Re-iterating the chart from above, this is what we saw in SDR data for 3 month USDJPY:

- Prices were nice and steady and then BANG! we gap lower by thirty basis points! Bear in mind this doesn’t show all trades – only ones reported to the US SDRs – but you get the idea of what happened last Thursday.

- Volumes were not unreasonable – a clip of JPY90bn + was seen earlier in September, but 3 month USDJPY had mainly been trading in clips below JPY30bn in size. On the 28th it was a JPY40bn trade that printed at -55bp.

- Clearly, something was going on.

The common feature for both 28th September 2018 and the previous gap (28th December 2017), was that the spot date for a cross currency basis trade (or an FX trade) went over the turn of the year. In the case of last Thursday, it was the end date of a spot starting 3 month trade that went over the turn. Back in December, it was the start date.

Turn of the Year

So, what is special about the end of the calendar year?

- There is a demand for USD cash over the turn of the year.

- Cross Currency Basis swaps have a physical exchange of notional, therefore they must be funded with cash.

- Any change in the implied funding of USD (or foreign currencies) over the “turn” will impact cross currency basis.

- Last Thursday, we saw both EURUSD and JPYUSD basis plummet. This implies that it’s a USD story as it is the common component of both.

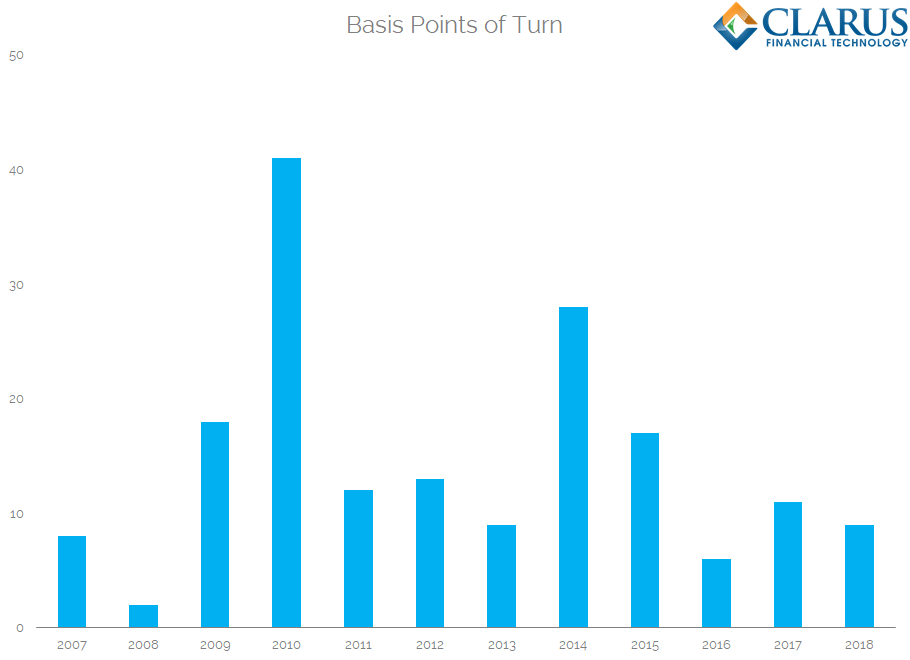

Looking at historic Fed Funds data (EFFR here), we can look at the spread between the 2nd January fixing and the previous day. This shows the magnitude of the turn in USD:

- The realised turn effect in the Fed Funds fixing for USD for the past 12 years.

- This has ranged from +2 basis points to +41 basis points.

- It has always been positive – clearly, there is some demand for USD cash over the turn of the year.

- It has averaged 14.5 basis points.

What causes the demand for USD? Historically, it has been related to balance sheet window-dressing from financial institutions (everyone wants to look like they have lots of cash on the balance sheet at their financial year-end). This year, it may have to do with the tax situation in the US – is it more efficient to leave cash off-shore at year-end and recognise it as a loan, or better to repatriate? I’m not a treasurer, but I can recognise that these decisions impact the availability of USD on reporting dates – such as quarter-end, year-end etc.

What did Libor do?

With the history of the turn, you might expect to see a jump higher on 3 month USD Libor on September 28th as well. Afterall, a spot starting deposit would mature in 2019, and who would possibly want to lend unsecured cash over the turn of the year?

Prepare to be underwhelmed…

- 3 month USD Libor did not budge.

- Apologies for the rather poor chart, but it’s difficult to jazz up something that didn’t move.

- The fix was just 0.002% different between the 27th and 28th of September.

There is obviously a huge disconnect between what we saw going on in Cross Currency markets and what happened with the USD Libor fixing.

Let’s quantify just how big the disconnect is.

Cross Currency Basis and the Turn

What has happened in Cross Currency Basis is pretty absurd by most standards:

- A 30 basis point drop in a 3 month contract suggests a hugely magnified effect for the two-day turn period (31st Dec 2018 – 2nd Jan 2019).

- We can calculate it simply: minus 30 x 92/2 = -1,404.5 basis points! Or about minus fourteen percent!

- That is just the basis component. If we take JPY rates to be near zero, and USD outright rates in December to be 2.3% (as per Fed Funds pricing above) we are looking at rates in excess of sixteen percent for overnight USD at the end of year.

- The change in the 3 month USD Libor fixing implies a turn effect of just 11 basis points (0.002% * 92/2).

This turn effect seems to be a basis story, not an “availability of USD cash” story. Which makes it particularly odd. The disconnect between the two markets is large – and that means it is scary. Something is broken in the link between the two markets. Hedge funds are typically unable to get credit lines to take a cross currency swap into its’ physical delivery, whilst it appears banks might not have balance sheet available to take advantage of it these days.

Data and the Full Story

The frustrating thing with OTC transparency is that it is still completely lacking in Europe. This means that as interested market participants, we are still unable to see the whole picture of what happened last Thursday. We can see a snapshot – from the US SDR data – but we do not know what happened in Europe. Despite the good news back in May from ESMA, we still haven’t seen changes in how data is disseminated from key APAs in our market. We continue to wait.

In Summary

- Short-dated cross currency basis plummeted as it went over the turn.

- The historic premium for USD cash over the turn has been around 15 basis points.

- USD Libor priced in a very small turn effect – a maximum of 11 basis points.

- Cross Currency basis priced in a turn effect of fourteen percent!