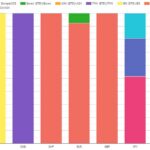

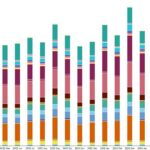

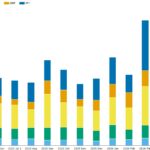

This is the Q2 2026 edition of our quarterly blog on competition between rates derivatives exchanges and CCPs. It can be directly compared with the Q1 edition and is a complement to our recent Q2 blog on cleared rates swaps volumes. Key takeaways In Q2 2026, the quarter on quarter (QoQ) shifts in the CCP […]

Read more

Our Technology

- Browser-based, nothing to install

- Simple APIs, integrate in Days

- Secure & Scaleable Cloud Hosting

- Built-in Connectivity to Data Sources

- High Volume and Super Fast Performance

- Highly Reliable Processing

- Full Production in Weeks not Years

- Monthly Subscription, No Upfront License fees