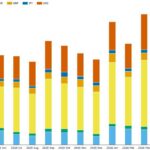

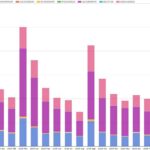

Q2 2026 shares of D2D platform core rates swaps

This blog reviews Q2 2026 D2D platform market shares of major currency rates swaps risk-trading, continuing the quarterly series from Q1 2026 shares of D2D platform core rates swaps. Key takeaways Q2 2026 saw the following D2D platform market share leaders and shifts in each major currency: All the charts and statistics in this blog […]

Record Q1 2026 CCP IM disclosures

At the end of March, clearing houses published their Q1 2026 CPMI-IOSCO Quantitative Disclosures. This blog focuses on cleared IM for rates swaps, credit derivatives (CRD) and exchange-traded derivatives (ETD) together with a sample of the other disclosures. Key takeaways 31 March 2026 saw a new record in CCP-disclosed cleared IM for each of the three […]

US-reported rates swaps compression: up 43% YoY

This blog looks at Q1 2026 volumes of US-reported compression of cleared “core” rate swaps (meaning OIS, fixed float IRS, and basis swaps). Key takeaways Scope and background This blog continues our coverage of US-reported rates swap compression volumes after 2025 SDR-reported IR compression and before that H1 2025 SDR-reported IR compression and 2024 US […]

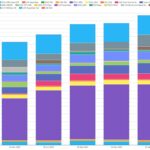

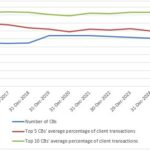

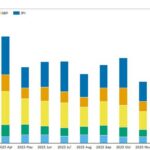

How concentrated are swap clearing brokers?

This blog gives an update on swap clearing broker concentration risk and asks whether the recent increase in the number of swap FCMs heralds an improvement. Key takeaways At the end of Q1 2025: Introduction Whilst client-cleared financial futures have been around a lot longer, client-cleared swaps started at LCH SwapClear in December 2009, about […]

Q1 2026 USD swaption volumes – up 14 percent YoY

This post continues our quarterly strikes analysis of USD swaptions, which are typically 50 percent or more of swaptions volumes in all currencies. We use SDRView data, which captures OTC derivatives trades reported by US financial firms to US SDRs. Key takeaways Swap market context If you are new to swaptions, some basics are outlined at the […]

Q1 2026 exchange/CCP shares of cleared rates derivatives

This blog is the first edition of what will become a regular quarterly blog on competition between rates derivatives exchanges and CCPs measured by market share of trade notional cleared. Key takeaways In Q1 2026, the exchanges and CCPs market shares of the more competitive cleared derivatives products were as follows. Read on for more […]

Volumes and most active names in credit derivatives – March 2026

Today we look at issuer names most actively traded based on single-name credit default swap (CDS) trades reported to US SEC Securities Based Swap Data Repositories (SBSDRs) in March 2026. This follows on from the prior similar blog covering September 2025, as we follow the natural CDS volume peaks in March and September. We rank SBSDR reported names by […]

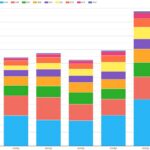

FX derivatives volumes at the end of Q1 2026

This blog covers the volumes of FX derivatives (FXD) in Q1 2026, following on from our prior blog on Q4 2025 FXD volumes. Key takeaways Q1 2026 saw record notional volumes for all five cleared FXD products (non-deliverable FX forwards (NDFs), FX options, FX forwards, non-deliverable FX options (NDOs), and spot FX) and for SDR-reported NDFs and […]

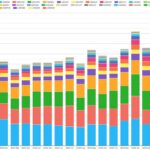

Q1 2026 cleared rates swap volumes and CCP share

This blog covers global notional volumes and CCP market shares of core cleared rates swaps in quarter one (Q1) 2026, including OIS and fixed-float IRS for all currencies and zero-coupon swaps for BRL and CLP only. Key takeaways In Q1 2026 global notional volumes of core cleared rates swaps were US$321 trillion – up 43 […]

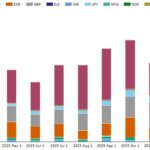

Q1 2026 cross-currency swap volumes and market shares

This blog reviews Q1 2026 cross-currency swap volumes and platform market shares, following on from our recent blog on a similar theme for the whole of 2025. We focus on US-reported cross-currency basis swaps in USD versus the five other major currencies. We use SDRView to aggregate volumes, DV01, and trade count by month and quarter. Key takeaways […]