DEFINITION

two-time (to̅o̅′tīm′)

tr.v. two-timed, two-tim·ing, two-times Slang

1. To be unfaithful to (a spouse or lover).

2. To deceive; double-cross.

BACKGROUND

Over the past 8 months, I’ve heard various complaints that some, or all, SEF’s are “double-counting”. Through these conversations, I’ve learned that people have different definitions of double-counting. It’s quite a dangerous assumption and accusation to make, for there are various ways in which this happens, and I’d like to dispel some of the more sinister claims and bring light to what is really going on.

WHAT IS DOUBLE COUNTING?

First, its important to note that there are various types of double counting. Let me run through these differences, and I will give them names.

“Perspective” Double Counting

For every buyer there is a seller. Let’s assume I use insurance broker “Broker Inc” buy an insurance policy from AIG. The broker arranges the policy, but I settle direct with AIG. Taking Broker Inc’s perspective, there is a purchase of a policy, and a sale of a policy. If booked properly, with Broker Inc as an agent to the trade, this shows up only once, as one line item on their books. In financial markets, some agents, often dictated by software limitations, book this as two line items.

With respect to financial derivatives, this would be akin to a SEF reporting a single, 1 million dollar trade, as two 1 million dollar trades (one a buy, one a sell), for a total of 2 million dollars.

I am fairly confident this is not happening on SEF reporting. Nor public SDR reporting. I have been made aware of a few cases where this has happened, but they have been treated as the accidents they truly are. I do not consider this a problem on an ongoing basis.

“Novated” Double Counting

Now let’s assume I need a pen to sign this insurance policy. I head to Amazon to purchase it. Amazon not only brokers the deal, they also settle the transaction for me. I do not need a credit relationship with Pen Vendor Inc, nor do they have to know who I am. Amazon takes my cash, delivers it to Pen Vendor, and in return takes a single pen of Pen Vendor stock off the shelf and delivers it to me. There exists a certain guarantee that I will get my pen, and that Pen Vendor will get their money. We each have a settlement relationship with Amazon.

Here, we begin to have room for debate. Let’s dismiss the fact that Amazon brokered the deal, and focus on the fact that they are clearing the transaction. If booked properly, I would expect Amazon to debit and credit two separate accounts; Pen Vendor Inc, as well as my own. Amazon’s clearing & settlement operation has novated the trade so that Amazon stands between us. Amazon has credit risk to both parties, as each party can default on their part of the deal. I acknowledge that somewhere in the Amazon Terms Of Service they probably pass on credit risk to Pen Vendor Inc, and that Amazon are further covered by the credit card companies, but please, just play along, and I’ll move on from the analogy.

In financial markets, this is analogous to the Derivative Clearing Organizations (DCO’s) such as CME, ICE, and LCH reporting a single 1 million dollar swap as 2 trades of 1 million dollar each, or 2 million dollars in total. While I’ve heard many people cry foul here, we should first acknowledge that the DCO truly does have 2 trades. Taking the (legacy) case where the original trade existed as a bilateral trade, the trade is properly novated when it gets to the DCO (original trade legally torn up and replaced with two separate trades). Because we expect DCO’s to support the world of derivatives, they need to be expert managers of credit risk, so they need to behave as though they have trades with 2 separate counterparties. As such, I support them reporting that original 1 million dollar trade now as two 1 million dollar trades; the DCO now has 2 million dollars of notional credit exposure to manage.

One consequence of this is that some reporting of DCO activity can be perceived as “doubled”. DTCC TIW has been blamed for this, but really, don’t blame them; rather its upon you to know what you’re looking at.

It is my understanding, through spot checking SEF and SDR records, that this type of “double counting” is also not happening on SEF reporting.

“Packaged” Double Counting

Keeping with my desire to have a pen, let’s now assume some different scenarios:

- I give someone a red pen and a blue pen. In return I receive two white pens. Is this a trade for 2 pens or 4?

- I purchase a package containing two pens. Is this 1 unit or 2?

- I give someone $1 in exchange for letting me use a pen for a week, at which point I return the pen and get my $1 back. Did we agree to trade 1 pen or 2?

- I purchase a twin-tip pen.

Let’s drop the pen analogy and look at some of the financial derivatives reported by SEFs:

- Butterflies. Market convention quotes the notional of the body of the butterfly, so a 8/9/10 butterfly will be quoted as the 9 year notional, with DV01-adjusted notional amounts for the 8 and 10 year. Taking a theoretical butterfly with notional values of 60/100/45, I would expect this to be quoted as a single 100 million dollar trade.

- Straddles, Strangles and Spreads. Likewise 2-legged packages, typically with the DV01 weighted notional values on each leg

- FX “Spot/Forward” Swaps. Probably the simplest case. It’s very clear in my mind that a 1 million dollar FX Swap should be counted as 1 million, not as a 1 million dollar spot leg + a 1 million dollar forward leg.

So What is actually happening?

As I have said before, whenever you look at data, you have to know what you’re looking at.

Let me describe the behavior I see across all the various product types:

- Butterflies. Without exception, everyone is reporting butterflies as individual line items. At least, there is no evidence to the contrary. Hence our 8/9/10 butterfly mentioned above, we’ll see a line item for 8, 9 and 10 years, with the 9 year having a DV01-adjusted notional of the sum of the 8 and 10. One might argue this is “double-counted” or “grossed-up”, but it seems to be commonplace.

- Curve Trades. Likewise, we see two line items. It should be mentioned that BGC has placeholders for these in their reporting, but I have never seen any activity. I suspect any such activity gets recorded as 2 line items.

- Swaption straddles. It gets a bit more interesting here. As a general rule, after scouring some examples of SEF data across both SEF and SDR reports, I’ve concluded that straddles are being reported again as two line items (“gross-up”). So a 50mm USD straddle is reported as 2 separate 50mm outrights. There is however a couple exceptions. Both ICAP (and IDGL) and Tradition seem to be reporting the straddle as a single line item for the appropriate (notional of one leg) amount.

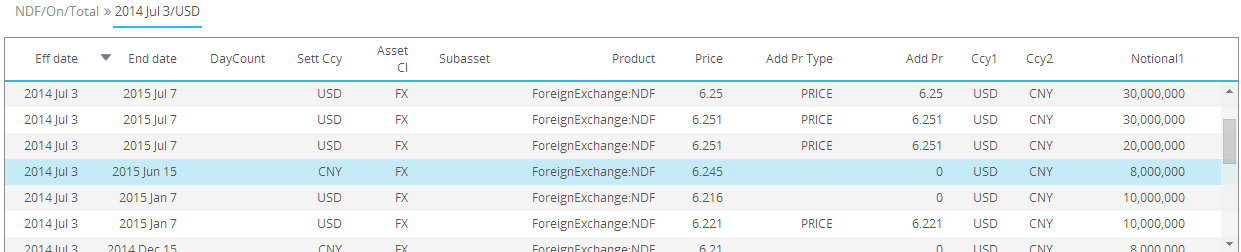

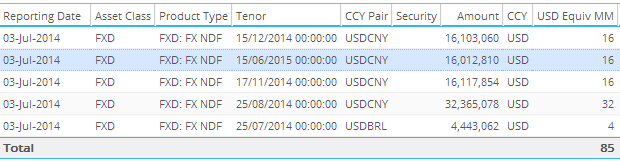

- FX NDF. These can get quite hard to discern. 360T is the only SEF to clearly delineate ND Swaps, and spot-checking their reports, seem to report a 65mm USD NDF swap as 65mm, not 2 lines of 65mm or 1 line of 130mm. I spot-checked various other NDF positions and trades against SDRView, and found at least one case of a SEF reporting both the spot and fwd legs as one line. A particular SEF reported a 16mm USD USDCNY NDF for June 15, 2014. Looking in SDRView, we can see that the only trade maturing on or near this date was an 8mm USD outright (as seen in the images below), so hence the SEF report is grossed-up to account for both legs. On the flip-side, I am of the understanding that Thomson Reuters reports their FX NDF as simply the larger of the two notionals (near or far leg), which I find an acceptable practice.

- FX Options. Generally, I’ve found every case of an FX Option straddle or similar strategy to be reported either as (a) multiple lines, or (b) a single line with doubled notional. So in either case the notionals are grossed up.

Taking the FX NDF example above, SDRView shows:

While SEFView shows:

Summary

- No two SEF’s share the same reporting formats

- When it comes to packaged transactions (ND Swaps, IR or FX Options straddles, curve trades, etc), we generally see individual line items per leg (some might call this “double counting”). There are few exceptions.

- Until we have more clear reporting rules on such transactions, we can expect most SEFs in these cases to gross up their reporting.

- Know what you are looking at. SEFView gives you the ability to do the homework.