Happy Valentines Day. Love, The CFTC

The next phase of expanded MAT-package interpretations is upon us. Back on November 10, the CFTC released their letter outlining their most recent extended package relief for certain swap packages. The next deadline is now upon us, February 15.

SUMMARY

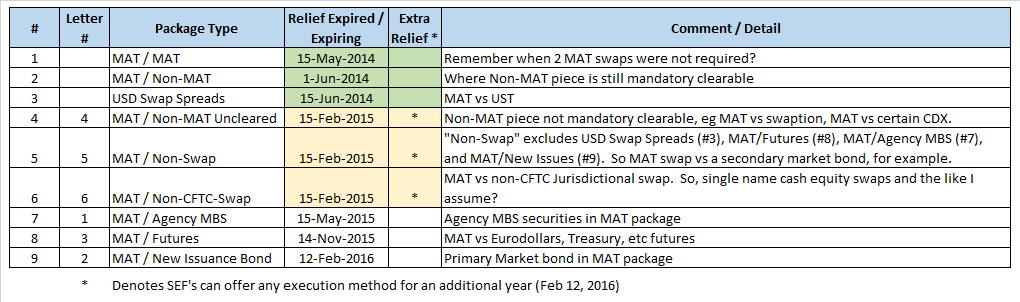

The table below is my little summary of the package relief that we’ve seen. The numbering in the first column is mine – there have been 9 no-action relief line items. The “Letter #” column refers to the corresponding line item in the November CFTC letter.

The green items have come and gone early last year. The yellow items are the ones that lapse February 15. I won’t claim to be an expert but generally these appear to be packages of 2 or more trades whereby the components include:

- MAT / Non-MAT Uncleared. MAT swap vs a non-mandatory clearable, CFTC-regulated swap. Best examples would be a MAT swap with a swaption, and MAT swap with a non-mandatory cleared Credit Index swap.

- MAT / Non-Swap. “Non-Swap” here has lots of exlusions such as futures, Agency MBS, and primary market securities. I’m left thinking this would be a swap vs a corporate bond in the secondary market.

- MAT / Non-CFTC-Swap. I suppose if you can dream of a swap that the CFTC doesn’t oversee, such as a single name equity swap (total return swap on a single name maybe?), then this would include those.

WHATS THE CHANGE

As always, I’d like to think we could come up with some crystal-ball measure of what this implies to expected On-SEF activity. With On-SEF activity running pretty consistently in the 50%-60% range since June 2014 for USD fixed/float IRS, do we expect any increase?

Trouble here is the universe of possible package leg types are not fully transparent. For example, if I had access to a database of mortgage backed security execution data, with execution timestamps that I could trust are in-line with the swap execution timestamps, perhaps I could compare that with trade reports from SDRView.

Having gone to TRACE and randomly chosen a corporate bond (GE), I can see execution timestamps to the second. However, even if I collected every corporate bond trade in every security, could I assume the logic that firms are using to stamp “execution time” is consistent?

A MIDDLE GROUD

So as a quick stab at this, I decided to look at MAT swaps vs swaptions. Surely there are lots of swaptions strategies whereby a hedge is transacted at the same time. I’d expect to find some swaptions that fit the following:

- Both (or more) legs to be executed in the same SEF/Non-SEF fashion (both on, or both off)

- Uncleared swaption of course because they can’t be cleared yet

- Executed at same time as similarly-executed swaps (timestamps to the second)

- Notional of the swap to be generally equivalent in delta terms with the option leg which I felt would apply to both cases of:

- Outright payer/receiver swaptions

- Even option straddles, assuming they are ATM forwards and assuming some vol skew, there should be a delta hedge

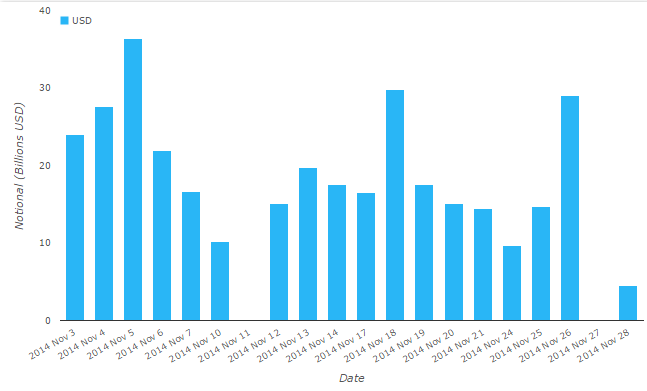

Also important that I look for this in a historical data set, so I chose November. Reason being I didn’t want to be fooled if somehow firms had found a way around this in the run-up to the relief expiration.

So I chose the week of November 3 – November 7, 2014, as this was a good, non-holiday week showing some decent swaptions volume:

RESULTS

- There were 849 USD swaptions reported/dealt in this week. All of which were reported to DTCC (BSDR did not have any).

- 206 Straddles

- 270 Payers

- 178 Receivers

- 195 Exotic

- Of these 849, there were 167 swaptions that shared an execution timestamp, to the second, with another swap or swaption:

- 17 Straddles

- 41 Payers

- 32 Receivers

- 77 Exotic

- All combined, these 167 swaptions accounted for 77 “packages”:

- 61 of these packages were only swaptions, no swap legs

- Only 16 of these packages included both swaption(s) and swap(s)

Hmm. Not quite what I was hoping. Particularly the 61 packages of swaptions-only. As many of you know, we expect normal packages of swaptions (eg straddles) to come through as a single line item (eg “D-“ for those in the know). In fact straddles account for a good portion of the activity we see, as evidenced in the numbers above.

So while not relevant to my research, I went on a slight tangent to examine what these 61 swaptions-only “packages” might be. Remember SDRView has already processed all the cancels and replaces for me, so that does not explain it. The answer seems to be:

- Vast majority of them are packages that include at least one exotic option. The other leg(s) are outrights or straddles.

- A few straddles that have been reported as separate legs.

- A few apparent strangles (different strike prices).

- And finally, while I don’t want to promote any fear-mongering, I found one that I have to believe was simply double-reported, or just so happened that the exact same swaption, same notional and strike / direction, was traded at the same second (and was not related to a cancel/replace event).

Fear-mongering aside, let’s look at those measly 16 “packages” of swaps and swaptions:

- 15 of them appear to be unrelated, with the underlying swap having effective and maturity dates years and years apart. Perhaps this is just a misunderstanding on my part, but would expect most hedges to be similar to the underlying. Even for a Bermudan, I would expect the end dates to at least match up. Further, some of the swaps are larger notional than the option. It just doesn’t match up.

- Only 1 of them appears to be a good match, roughly a 15 delta option hedged with a swap.

Results like that make me think I’ve got my assumptions wrong somewhere. However, this could be explained more simply:

- My analysis relied upon execution times being consistent. Because such packages are not MAT’d, these could be operationally processed with less rigor, particularly off-SEF.

- Swaptions market does not “cross” the delta nearly as often as happens in some other options markets.

SUMMARY

I was hoping to come up with something significant. You’d have to believe many swaps are traded alongside some of these other derivatives that now construe a MAT-package. Unfortunately my quick Valentines day attempt to find these proved troublesome.

Of course, we’ll be able to update our tracking of On/Off SEF analysis in the coming months to determine if these expired relief’s have impacted anything or not.

And why would you not use treasury futures as a hedge given that you might have to re-hedge quite frequently anyhow? Also, saves the pain to pay bid-offer to the in-house swap desk or a swap broker. Any thoughts on this?

Hi Frank,

Thanks for the comment. I think futures do make sense as one alternative. My only thought would be precision. But valid point on costs.