The 1st November 2020 heralded a fundamental change in swaps markets. SEFs executing trades in specific products were no longer permitted to disclose the identities of the counterparties (to each other) after the trade:

At the moment, this rule only applies to MAT swaps – i.e. those products subjected to the execution mandate and required to trade on-SEF if a US person is involved.

I thought it would be interesting to run through the volumes in the early days of these new rules to see if anything has changed. It is also a good excuse to dig into some SEF data, which we haven’t done much of this year (only 3 SEF blogs in 2020!).

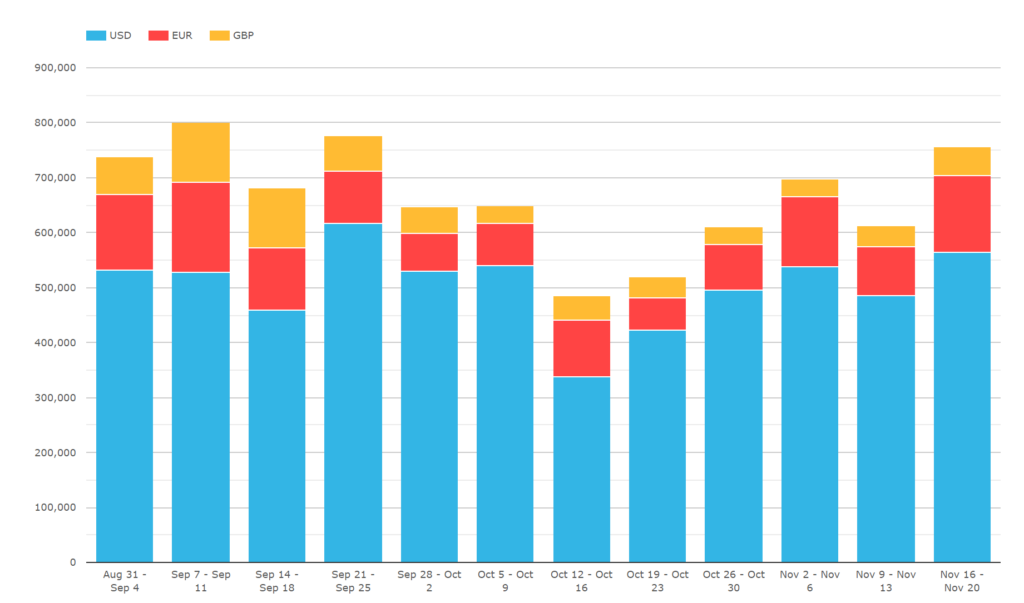

SEF Volumes

I think it is important to state from the off that the new rules on PTNGU (Post Trade Name Give Up) appear to have had little effect on the weekly volumes of SEFs. I can’t see from the chart above any clear evidence that either:

- End-users have flocked to SEFs so that they can now execute huge chunks of risk anonymously.

- Dealers have actively moved flow away from SEFs because they no longer learn the identity of their counterparties.

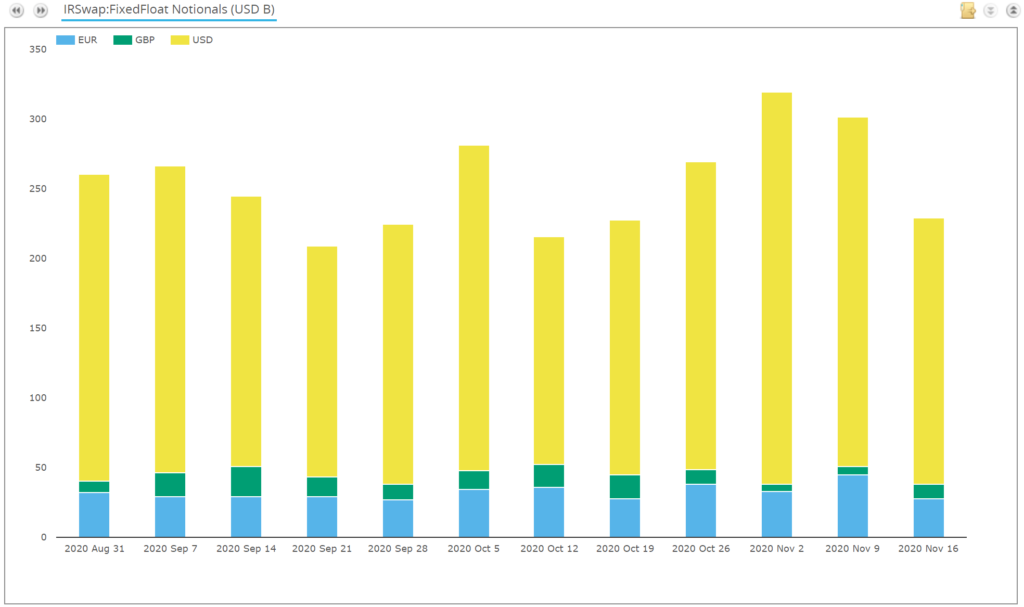

SDR MAT Volumes

Equally, there doesn’t appear to have been any great change in MAT trading. At the moment, only MAT products are subject to the new PTNGU, so in theory only these products are traded anonymously:

The Global Market

Given there are no obvious signs in the SDR data, I decided to combine US data with our global data. That means looking at the percentage of the global cleared market that is executed on-SEF, combining CCPView data with SEFView.

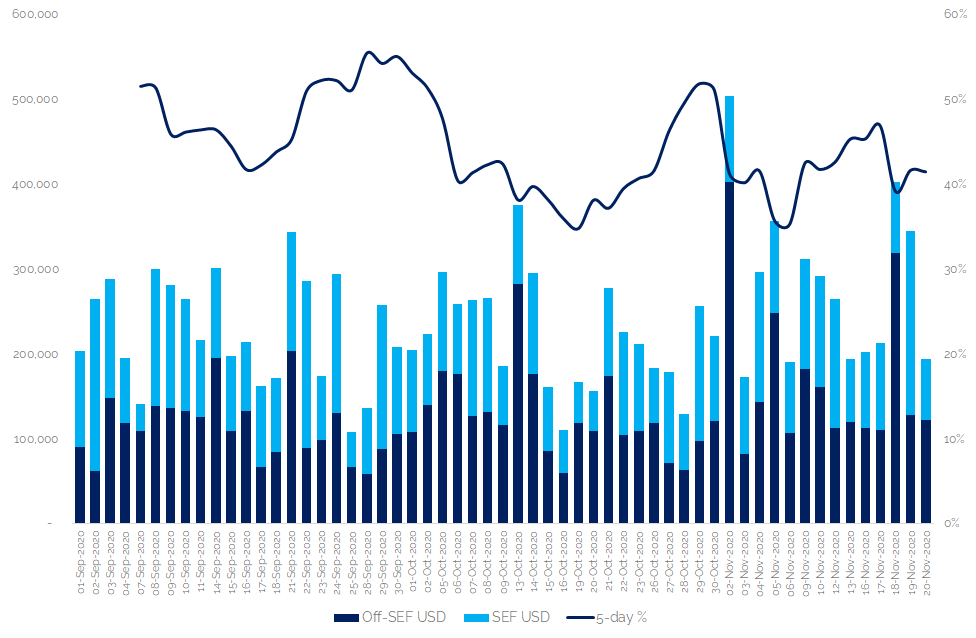

USD

First up, the largest SEF Rates market, USD IRS.

Showing:

- PTNGU rules came into force 1st November 2020.

- I can’t see any dramatic changes in the chart from that date, other than the huge volume spike that occurred on the 2nd November in Off-SEF USD IRS activity.

- Similar activity was seen on 13th October as well, so doesn’t seem necessarily linked to the new PTNGU rules?

- In November so far, ~40% of USD IRS has traded on-SEF.

- In October, that figure was 42%.

- Remember, we are measuring the entire USD IRS global market here, not just the trades reported as On-SEF and Off-SEF in the SDRs. The SEF data also relies on uncapped notional amounts as reported T+1 by the SEFs themselves, so SEF volumes are accurately stated.

It appears that, in terms of volumes in USD IRS, the new PTNGU rules have neither dampened nor accelerated the choice of SEF trading.

I got to thinking maybe this was because there is an ingrained and “sticky” pool of USD IRS liquidity on-SEF, which market participants are used to accessing since 2013.

Therefore it is natural to wonder whether this same pattern holds in other currencies and smaller SEF markets?

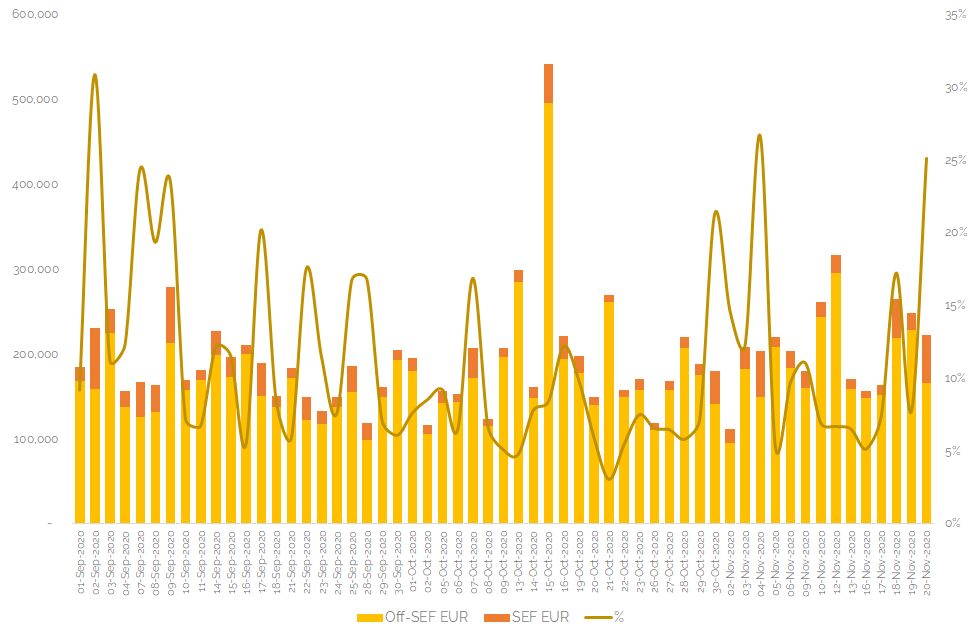

EUR

The pool of liquidity for EUR IRS trading on-SEF is consistently much smaller than in USD, accounting for a significantly smaller portion of the global market.

Showing;

- This is not a great time-series of data.

- The activity of US Persons as a percentage of the overall EUR IRS market varies significantly day-to-day.

- It is therefore difficult to ascertain any trends, particularly over such a short period of time. We are only 15 days into the new PTNGU regime!

- We can at least say that SEF trading has seen two significant days during November when 25% of global EUR IRS volumes have executed on-SEF. This cannot be a bad signal for anonymous trading at least!

Overall, I think it is very difficult to form any opinions for the EUR market just yet. It would of course help if we had decent MIFID II data to look at as well!

- In November so far, ~12% of global EUR IRS volumes have been transacted on-SEF.

- In October, ~8% of global EUR IRS volumes were transacted on-SEF.

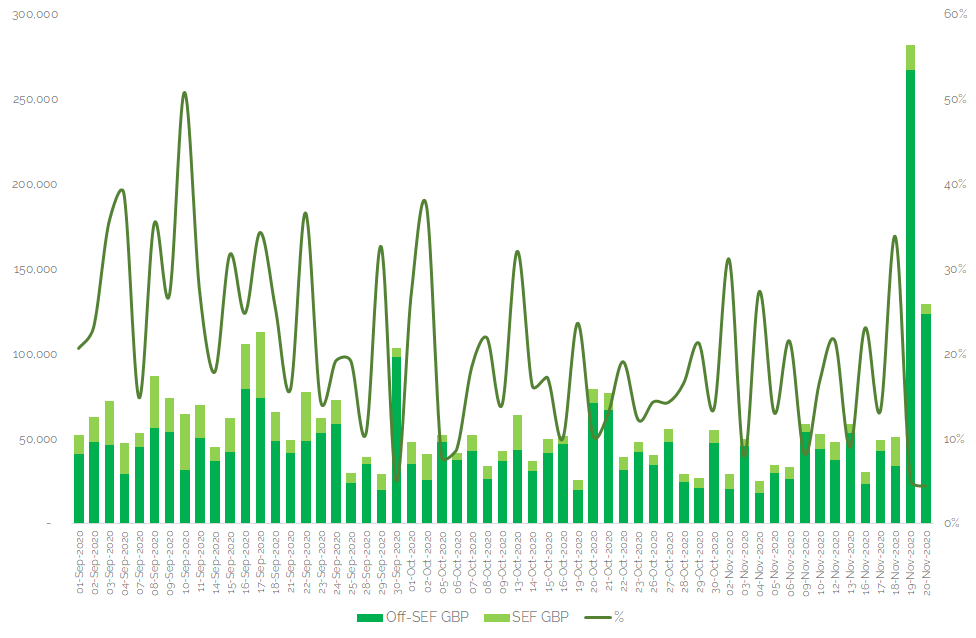

GBP

Finally, what about GBP? Coverage in the SDRs has been fairly good for GBP. This may change with D2D activity moving to SONIA and MAT rules only covering LIBOR trades. Let’s take a look at the data anyway.

Showing;

- Similar to EUR, it is really too volatile to draw any firm early conclusions.

- In November, ~12% of global GBP IRS was executed on-SEF. Bear in mind this is LIBOR-linked, not SONIA.

- In October, ~17% of global GBP IRS was executed on-SEF.

Conclusions

The data doesn’t particularly help us this time in seeing the impact of regulatory reform. However, we feel that the introduction of anonymous trading on-SEF is an important structural change in US Rates markets and we will continue to monitor the effects closely.

At this point in time, I am not sure when we will be able to see this effect in the data. It is of course possible that market participants have had a little too much on their plate during November (election, vaccine) to really concentrate on anonymous trading.

Over time, I am confident the data will reveal the true impact of these changes.