There is a new April 2020 ESMA consultation on the Transparency Regime for OTC derivatives.

- ESMA are proposing potentially wide-sweeping changes to post-trade transparency in their latest consultation.

- Deadline for responses is currently April 19th 2020.

- We encourage all market participants to respond to this vital consultation.

- We could finally witness the beginning of transparency in Europe as a result of these changes.

The Consultation

The “MiFID II/ MiFIR review report on the transparency regime for non-equity instruments and the trading obligation for derivatives” was published on March 10th 2020.

That probably feels like a lifetime ago for all of us!

I’m therefore worried that this vital consultation, which contains proposals that could finally provide transparency to European markets, could easily be ignored by the market. Too much chaos, too much volatility, too many other things going on to bother replying.

Please don’t let that happen. The proposals outlined below are sound and could finally bring transparency.

A Results-Based Assessment of Transparency

Clarus provide transparency data for OTC derivatives. This is our business.

Every single one of our data clients expected us to provide them with a MIFID II-related product by March 2018. We have experience collecting, curating and publishing a diverse array of data from multiple SDRs, SEFs and CCPs.

Unfortunately, we have never officially been able to launch MIFIDView because post-trade data is almost impossible to access for most of the European market.

However, everyone intending to respond to this consultation is welcome to take a look at the data that MIFIDView is able to access under the current European post-trade transparency regime. Just contact us (and ask nicely).

I warn you now it is….underwhelming. But it certainly proves the point that the current regime IS NOT WORKING.

On Page 61 of the consultation, ESMA state that 279 entities reported non-equities post-trade data in 2018.

Clarus are able to access FOUR of them.

Yes, despite being professionals at this, we can only access 1.4% of the data providers out there.

I think that is the results-based assessment of transparency that it is important for regulators to hear. It has to change.

Proposed Enforcement of Post Trade Transparency

ESMA recognise that post-trade transparency is not currently working. They state across the report that;

The overall level of real-time post-trade transparency appears to be very limited…. Not all trading venues are currently (fully) complying with the requirement to make pre-trade data available free of charge 15 minutes after publication. This significantly limited the analysis ESMA could perform….ESMA agrees with the comments made by many stakeholders that a four-week delay for the publication of a transaction provides information to market participants which is of limited use.

3.2.2 ESMA’s assessment of the post-trade transparency framework

As a result of these deficiencies, and even going as far as to list the issues we noted on our blog 5 Things That Are Making MIFID II Data Useless, ESMA propose the following course of action:

Q14: Do you agree with ESMA’s proposed way forward to issue further guidance and put a stronger focus on enforcement to improve the quality of post-trade data?

So let’s hope to see some enforcement actions coming through. As we know, Transparency is even more vital in stressed market conditions than under normal ones.

Scrap Deferrals. Can we Also Scrap Liquidity Assessments?

Worry not, this consultation is not just about ensuring there is (finally) some enforcement of the rules. It goes much further and now proposes some wide-sweeping changes to post-trade transparency.

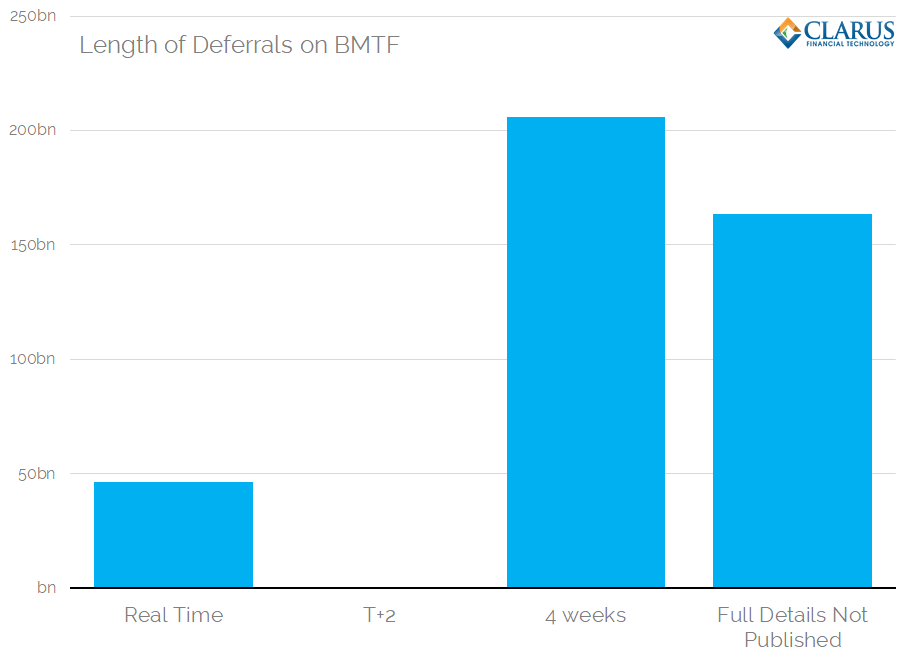

Given that the data is currently inaccessible, unrepresentative and mainly delayed by 4 weeks, ESMA are putting forward three options to fix this. Remember that 89% of notional in IRS is currently deferred by four weeks:

The three options presented by ESMA are;

Option 1

Volume masking for transactions in illiquid instruments and for large transactions

Post-trade information of transactions in illiquid instruments and above the large-in-scale threshold would be published as close to real time as possible with the volume being masked. The volume of the transactions is then published after a certain period of time following the transaction, such as two calendar weeks.

Option 2

Volume masking only for large transactions

Post-trade information for transactions above the large-in-scale threshold would be published as close to real time as possible with the volume being masked. Transactions in illiquid instruments would be published in real time.

The volume of the large-in-scale transactions is then published after a certain period of time following the transaction, such as two calendar weeks. This option would require the deletion of the deferral for illiquid instruments which would be in line with the regime currently in place in the US. However, in contrast to the US regime where the transaction details of block size transactions are never made public, all the details of volume masking transactions would be published after a certain period of time, such as two calendar weeks.

Option 3

Volume masking for large trades for two days and extended volume masking for very large trades

As in Option 2, post-trade information for transactions above the large-in-scale thresholds would be published as close to real time as possible with the volume being masked. The volume of the large-in-scale transactions is then published after two days. For very large transactions, such as those 5 times the large-in-scale threshold, would be published after a certain period of time, such as four calendar weeks.

Notes on the Proposals

I strongly suggest that everyone reads our recent posts on Block Trading. We support making all transactions public in real-time, but are concerned about delaying data for Large in Scale transactions. This is because 43% of notional is transacted above the block threshold in the US. This is despite US block thresholds in interest rate derivatives being higher than the LIS levels.

Nonetheless, what an almighty step forward it would be to see all instruments reported in real-time, with free access (enforced) to the data 5 minutes afterwards.

We also note three things about the proposal in relation to the US regime:

- Any transactions executed on-SEF have their full size reported T+1. These volumes are aggregated at the instrument level, not at the transaction level. However, it allows us to know the aggregated real volumes T+1, just not at a transaction level. This is important for monitoring total sizes traded, given that 43% of notional is executed above the block threshold.

- Trading Venues need to be allowed to report their full volumes so that their market share statistics are accurate.

- Simplicity is key. The current European deferral regime already shows that multiple different deferral periods is detrimental to transparency.

Bringing Europe up to the Gold Standard

Option 2 above certainly offers a step forward. We hope that it can go even further.

However, it is also crucial that respondents note section 3.2.2.3 Assessment of the concept of traded on a trading venue (TOTV). This section of the consultation serves to highlight how little of the total market is even subject to post-trade transparency. This is not helped by a narrow interpretation of TOTV by ESMA.

Fortunately, this consultation puts forward a crucial proposal, under Option 3 on page 70:

203. Option 3: Under option 3, the concept of TOTV for OTC-derivatives would be abandoned and, in principle, any OTC-derivative would be subject to post-trade transparency and transaction reporting. This approach would closely follow the approach chosen in the US for derivatives as set out in section 727 of the Dodd Frank Act and further specified in 17 CFR part 43 for post-trade transparency.

Yes ESMA!

Therefore, everyone really needs to respond Question 18 as well:

Q18: Which of the three options proposed (to clarify the concept of TOTV), would you recommend (Option 1, Option 2 or Option 3)? In case you recommend an alternative way forward, please explain.

Pre-Trade Transparency

There is also a whole section on amendments to pre-trade transparency. I don’t want to water-down the message in this blog about fixing post-trade transparency by attempting to cover this large topic at the same time. But I would say that this paragraph from the consultation is the whole crux of the problem:

Many MTFs and OTFs do not accept orders that cannot benefit from a waiver from pre-trade transparency.

Page 29. MiFID II/ MiFIR review report on the transparency regime for non-equity instruments and the trading obligation for derivatives

How can a transparency regime be in place that allows whole businesses to happily run outside of the regime?!

In Summary

- Please take the time to respond to the consultation from ESMA on transparency in European markets.

- The proposals include aligning post-trade transparency with the US, so that almost all transactions are reported, replacing the current carve-outs for transactions not TOTV.

- Data access will be enforced, so we should finally get access to the public data.

- The deferral regime could be significantly changed, so that all transactions below block/LIS thresholds are reported in real-time.

- These are vital changes to provide post-trade transparency.

- If you need data for any of your answers, please reach out to us for access to MIFIDView. It is a tool that can help your responses, and ESMA need data.