The topic of whether CCPs have sufficient “skin in the game” was a popular and contentious one at conferences in 2014 and 2015, but one that I thought had been done and dusted. So I was surprised that it came up again at one of the FIA Boca 2016 panels in mid-March and with the usual protagonists at US conferences; JP Morgan and CME.

Interestingly I heard articulated a figure of 10% of Default Fund as a desirable CCP capital contribution from the JP Morgan person on the panel; which struck me as an oddly spurious number to come up with. So I decided to look in more depth at this topic, firstly by reviewing the literature and then by looking at the data.

Background

The most useful paper I found is by the Reserve Bank of Australia from June 2015, titled “Skin in the Game – Central Counterparty Risk Controls and Incentives” and I recommend reading this as not only does it cover the topic very well but it also provides a bibliography of references to all of the key sources.

For those of you pressed for time, here is a selected bullet point summary:

- CCPs run matched books and are not exposed to market risk under normal conditions

- CCPs apply risk controls to manage potential losses in the event of a member default

- The sequence in which these are applied is called the CCPs “Default Waterfall”

- The Default Fund is sized to cover the potential loss in stressed markets of the largest two members

- Members and the CCP have an incentive to minimise the risk that their resources will be used in a default

- The distribution of these losses can influence incentives and minimise free-rider problems

- There is no minimum regulatory requirement on the composition or order of use of a CCP’s resources

- Typically most CCPs apply a portion of their own capital before utilising member contributions

- If this portion is material to the CCP, that should be sufficient incentive for prudent risk management

- This remains true regardless of the size of the CCPs contribution relative to the size of the default fund

- Under EMIR a CCP must contribute at least 25% of its regulatory capital before member contributions

- Governance of the CCP and transparency of CCP risk controls are very important

At first read I was not sure of the minimum 25% capital required before member contributions, but the more I think about it, the more I like the concept. As long as a material amount of capital of the CCP is ahead of members, than that should be sufficient for the CCP to be prudent and not lower margins to try and attract more business. Whether 25% is the correct percentage, I am less sure.

Onto some data.

CCP Disclosures

Lets look at the CPMI-IOSCO Disclosures from 3Q 2015 for a few OTC CCPs and their Default Funds.

[UPDATE: New version of table to replace ASX Clear numbers with ASX Clear Futures which covers OTC IRS]

Showing:

- All these CCPs put their Own Capital Before using Pre-funded member contributions

- ASX Clear F is the only CCP in the list where its Own Capital Contribution is greater than member particpants

- For the others Own Capital ranges from 1% to 5% of Pre-funded Aggregate Participant contributions

- However these percentages are largely meaningless

The more interesting question is whether the CCP’s Pre-funded Own Capital is material to the CCP and sufficient incentive to mitigate against imprudent risk management in terms of lower risk margin and the free rider effects from over relying on participants.

The more interesting data would be comparing the CCP’s Pre-funded Own Capital with its Regulatory Capital. However this latter figure is not available in the Quantitative disclosures. Shame even with hundreds of numbers, there are always others you would want to be added. Lets hope there exists a feedback mechanism to augment the reported data, or perhaps these are already published elsewhere; if someone knows, please inform us.

However looking at some of the numbers, $150 million CME IRS, is a significant number even at the CME Group level and definitely at the CME IRS Clearing Service level. The same applies to the $53 million at LCH SwapClear.

Default Fund Contributions

A question worth exploring is what financial benefit would accrue to a member if the CCPs Prefunded Own Capital were increased as a proportion of the overall Default Fund.

For simplicity’s sake lets use an example:

- A member participant that contributes 10% of the CME IRS Prefunded Aggregate requirement of $3.5 billion

- CME doubles its Pre-funded Own Capital from $150m to $300m

- As the Total Available Loss Resources do not need to change, the Prefunded requirement from members is reduced by $150 million

- And for this member that means a $15 million reduction in DF contribution

Assuming a cost of capital of 10%, this is a saving of $1.5 million in funding the DF contribution over 1-year.

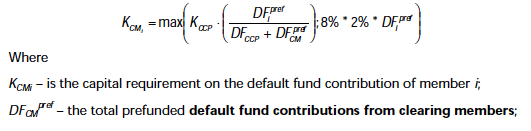

The RWA Capital for DF contributions from BCBS 282 is given by:

KCCP is given in the Quantitative Disclosures and for CME IRS is $100,769,820.

Running through these figures shows the capital requirement reducing from $9.6million to $9.2million, a reduction of $400,000, so not a big number.

At least in this example, increasing the portion of the CCP’s Own Capital in the Prefunded portion of the Default Fund does not make a large difference to a members costs.

Of course this is very different for ASX Clear Futures, where the majority of Pre-funded DF Resources are provided by the CCP, meaning that there is a material difference in member costs.

Summary

Skin in the game was a hot topic in conferences in 2014 and 2015.

It has been well covered with position papers, discussion papers and press.

CCP Risk Controls and Incentives must mitigate free-rider problems.

The consensus is a CCP needs to have a material part of its capital ahead of members in its Default waterfall.

In EMIR this is specified as a minimum of 25% of it regulatory capital.

CPMI-IOSCO Quantitative Disclosures greatly help in providing transparency.