- European Money Markets Institute (EMMI) announced on Thursday 5th May that they will reconsider their plans to move Euribor to an entirely transaction-based fixing.

- It was previously expected that the current quotation-based system would change sometime this year to a transaction-based fixing.

- The EMMI now plans to look into creating a hybrid quotation/transaction fixing as a result of a scarcity of actual transactions occurring on a daily basis.

- Euribor futures sold off (rates went higher) in response.

- Could transactions in related markets be used in a hybrid approach to secure a more stable footing for the fixing process in the future?

Euribor Fixings

Currently, the definition of Euribor is:

“The rate at which euro interbank term deposits are being offered within the EU and EFTA countries by one Prime Bank to another at 11.00 a.m. Brussels time.”

Across the Rates market, benchmark administrators, regulators and market participants have been working towards an “IBOR+” definition, whereby this current quotation-based approach is shifted (seamlessly) to transaction-based fixings.

In general, if fixings were to shift to transactions, the market generally thinks that:

- Rates would shift somewhat lower. Remember that Euribor is the offered side of the market. Transactions will likely be lower as someone is actually willing to lift the offer.

- This is reinforced in the re-stated definition of Euribor as a wholesale “funding rate” rather than a “borrowing rate”.

- The range of counterparties that are covered by transactions is quite broad, covering:

- Deposit-taking corporations

- Other Financial Institutions

- Official Sector Institutions

- Non-financial corporations

- Insurance Corporations

- Pension Funds

- The range of short-term securities making up the eligible transactions is wider, including CP, CDs etc.

- The submission itself is a volume-weighted average of these transactions. Therefore if Official Sector Institutions (excluding Central Banks) are big users of unsecured finance, the transactions could be weighted towards highly credit-worthy borrowing – at least compared to today’s definition.

The EMMI have been conducting a “Pre-Live Verification Programme” for the past six months. The panel banks have hence been submitting their quotation-based rates. At the same time, transactions from 31 banks have been analysed in parallel to these quotations. This allows the EMMI to monitor how the change in methodology will impact the Euribor fixings in terms of both price level and volatility.

Unchanged

On Thursday, EMMI announced;

EMMI’s analysis has concluded that under the current market conditions it will not be feasible to evolve the current Euribor methodology to a fully transaction-based methodology..

Euribor…will be continued as a quote-based benchmark while the development of the hybrid methodology is ongoing.

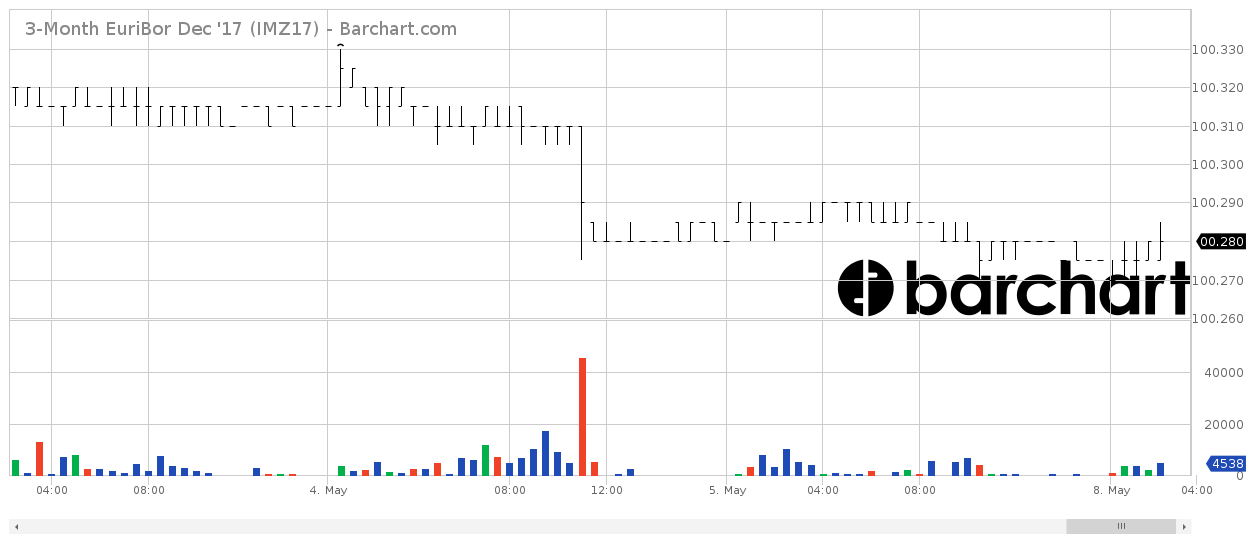

The Euribor STIR future maturing in December 2017 reacted thus:

Showing a 3 basis point drop in the future amid large volumes. This reflects market expectations for quotation-based fixings to be higher than a transaction-based system. To be fair, it also probably reflected a positioning-bias in Euribors generally, where Rates are expected to head somewhat higher.

The problem that administrators and regulators face is spelled out in the EMMI report:

The decrease in the daily market activity under the current market conditions, does not allow for a methodology which is fully based on transactions

Volumes

I don’t think this statement from EMMI is a surprise to many market participants.

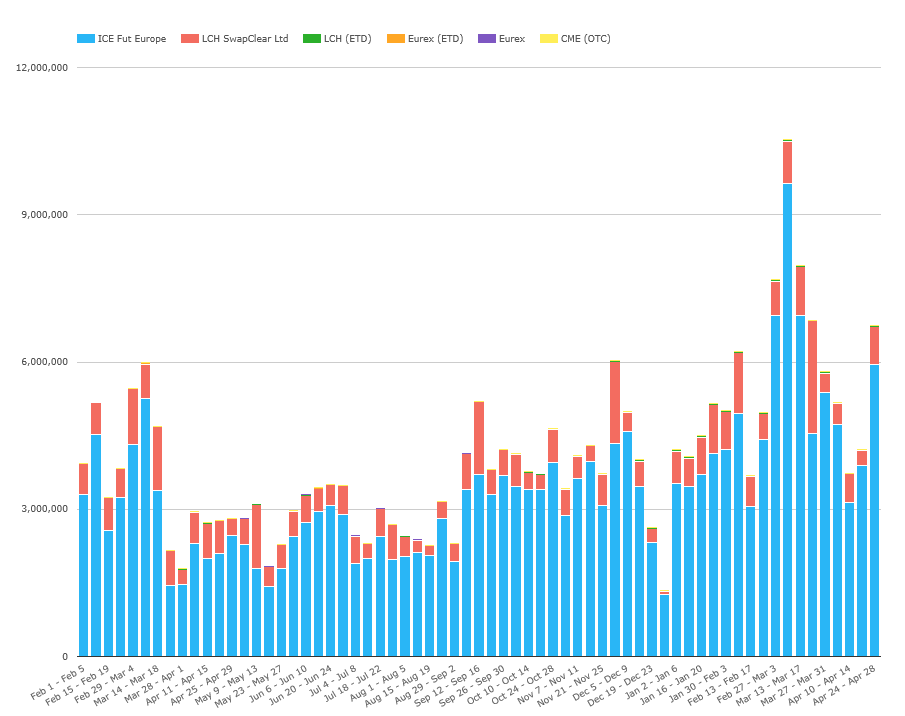

However, we can also say that there has been no decrease in the daily market derivatives activity. For example, from CCPView;

Showing;

- The notional-equivalent volumes trading across EUR-denominated OTC FRAs and Euribor Short Term Interest Rate futures.

- The vast majority of OTC EUR FRAs are cleared at LCH’s SwapClear.

- The vast majority of ETD Euribor futures activity is at ICE Futures Europe.

- A weekly average of €641bn has traded in the past year in EUR FRAs.

- A weekly average notional-equivalent of €3.4trn has traded in the past year in EUR STIRs.

- These volumes have been consistent over the past 18 months.

- These derivatives markets show no signs of being affected by the potential uncertainty in the re-calibration of the underlying index.

Clarus Data

It shouldn’t come as a surprise that I support a transaction-based methodology to define these fixings. Clarus are all about increased transparency across all markets. I have started to think about whether we could turn this problem on its’ head and use our transaction data to help fix the fixing process.

By way of background reading, I caught up on the Market Participants Group efforts to reform Libor in the excellent Duffie and Stein (2015) paper. Once you’ve read that, it will be of particular interest that OIS volumes now outstrip those of IRS (on a notional basis).

Regulated Markets

With OTC derivatives increasingly transparent, clearing mandates enforced, CCPs tightly regulated and futures markets closely monitored pools of regulated liquidity, when does it become time to take a step back and look at the Euribor fixing as a derivative of the FRA and STIR markets, rather than the other way round?

The EMMI’s process to change the definition and fixing process gives due care and attention to the potential market impact of any change. But it has been hamstrung by “current regulatory requirements and a negative interest rate environment.”

Given that we have a huge pool of transactions offering price information regarding the index in question, could we ever envision a process whereby transactions in FRAs and STIRs can (help) set the level of the index itself? After all, people have tended to go to jail for profiting off their derivatives transactions, not their cash transactions.

The Problems

There are some potential pit-falls in this approach if we do not change our current thinking:

- Libor/Euribor measures unsecured bank (or wholesale) funding levels. A derivatives contract is simply a contract for difference against a fixing, not a provision of funding. Changing the Underlying in such a fundamental manner could mean that the fixing loses all attachment to its’ original purpose.

- In light of this, do we satisfy the EMMI (& IOSCO) requirement to keep the “Underlying Interest” for Euribor the same (i.e. we need to avoid changing the economic variable that the benchmark (Libor) seeks to measure).

- Practically speaking, we need a spot fixing whilst most derivatives are only concerned with a fixing in the future.

- Fixings do not evolve in a straight-line. Derivatives are priced with dynamic “jumps” in the level of fixings between dates.

- Participants in derivatives markets (traditionally) do not need to commit balance sheet to the transactions, as they are naturally leveraged positions. However, with more stringent capital requirements on the banking sector and large derivatives users, a reduction in speculative trading at banks, and continued shrinkage in unsecured cash markets themselves, maybe the biggest players in derivatives commit just as much balance sheet as those banks still making (very small) unsecured loans each day?

- Are we just transferring the potential for problems from one market to the next? What if volumes in FRAs and STIRs dry up due to a shift in liquidity towards new Risk Free Rates such as OIS indices?

The Solutions

To this author, none of these potential problems seem as great as the single problem underlying unsecured cash markets – there are no transactions, leaving the fixing floundering in a grey “subjective” area.

Why can we not flip markets on their heads and state that STIR-derived and FRA-derived volume weighted average prices are the benchmark? A few years back, I would have said because Libor measures unsecured lending. But when unsecured lending can be seemingly cheaper than secured, I’m not sure Libor really has any base in reality? Isn’t it now only an index upon which derivatives are based – be they either off-balance sheet swaps or on-balance sheet loans.

Imagine the following fixing methodology:

- Take all transactions that do actually occur in unsecured markets, as previously planned.

- Add an additional requirement that panel members provide a spot fixing, defined as a spread (in basis points) to the IMM date.

- These Spread Quotes are binding. Panel members must contribute their spread to the IMM date for FRAs fixing today.

- Panel members must provide both a bid and offer spread.

- Any crossing rates are automatically executed as a FRA at e.g. LCH.

- The benchmark administrator sets the maximum allowable bid-offer spread.

- The window for the IMM fixing can be set according to administrator wishes. Generally speaking, the longer the window, the less chance of manipulation.

- As with proposed Euribor membership, “banks in the euro area categorized as “significant” by the ECB under the Single Supervisory Mechanism” would be regarded as potential panel members. All of these will have the ability to clear FRAs.

- We could, as a market, decide to open up panel membership to non-bank entities, allowing the fixing to evolve with potential changes in market structure.

The Future

I have no doubt that better minds than mine have looked into this question and clearly reached a different conclusion. I am therefore not suggesting that I can come up with the solution in the space of a blog. For example, self-critiquing this blog is easy:

- To minimise any difference between what we are trying to measure (actual unsecured funding) versus what we can observe (a derivative fixing in the future), we may want the future and/or FRA contracts physically deliverable into an unsecured loan (deposit) against a mutualised credit institution. (Isn’t that just a CCP….?)

- That still doesn’t solve the problem of having a (partially) self referencing futures contract in the first place.

- Or help to identify the position limits an exchange may have to enforce.

- Or solve how to define the 1m, 6m or 12m tenors.

And yet, I feel like these are at least problems to overcome rather than a crucial lack of transactions themselves.

In Summary

- The market generally wanted to move Euribor to an entirely transaction-based fixing methodology.

- The number of unsecured transactions occurring each day are not high enough to provide a reliable source of data.

- The benchmark administrator, EMMI, will therefore look to develop a hybrid approach between a transaction and quotation-based methodology.

- We would like to support the development of a hybrid approach, incorporating transaction data from related markets.