Continuing with our monthly Swaps review series, let’s look at volumes in February 2017.

Summary:

- USD IRS price-forming volume > $2 trillion gross notional

- 8% lower than a year earlier

- On SEF vs Off SEF at 65% to 35%

- SEF Compression activity in USD IRS > $230 billion

- USD OIS volume at > $3.3 trillion is massively up (3 times Feb 2016)

- With > $2.4 trillion Off SEF and > $934 billion On SEF

- Daily volume much higher from 14 Feb onwards

- On SEF EUR, GBP, JPY IRS volumes at > $270 billion

- SEF Compression in EUR, GBP, JPY strong at > $75 billion

- Volume for USD, EUR, GBP, IRS, OIS, Basis Swaps was $1.3 billion DV01

- Lower than the $1.5 billion in January 2017

- All SEFs except Tradeweb with lower volume than prior month

- Bloomberg just in the lead from Tradeweb

- ICAP and Tradition neck and neck

- CME–LCH Switch volume was $39 billion

- Back down to Nov 2016 levels and the basis tightened

- Global Cleared Volumes are up at $26.3 trillion

- LCH SwapClear up 40% with a $7 trillion increase in USD OIS

- JSCC volume also up by 25%

- In Asia, both LCH SwapClear and ASX significantly up

- In LatAm volumes slightly down, with CME at $386 billion

- LCH SwapClear with $829 million of MXN IRS, up from $124 million

- Inflation Swaps at LCH SwapClear just above their Jan 2017 high

- NDFs at LCH ForexClear also just above their Nov 2016 high

Onto the charts, data and details.

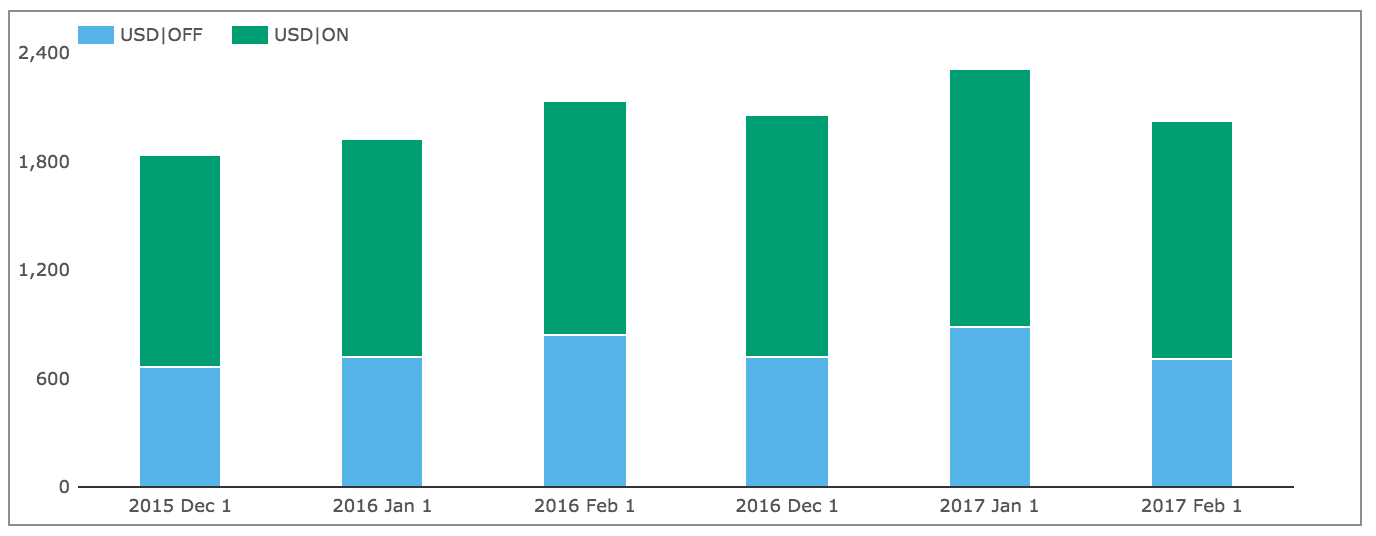

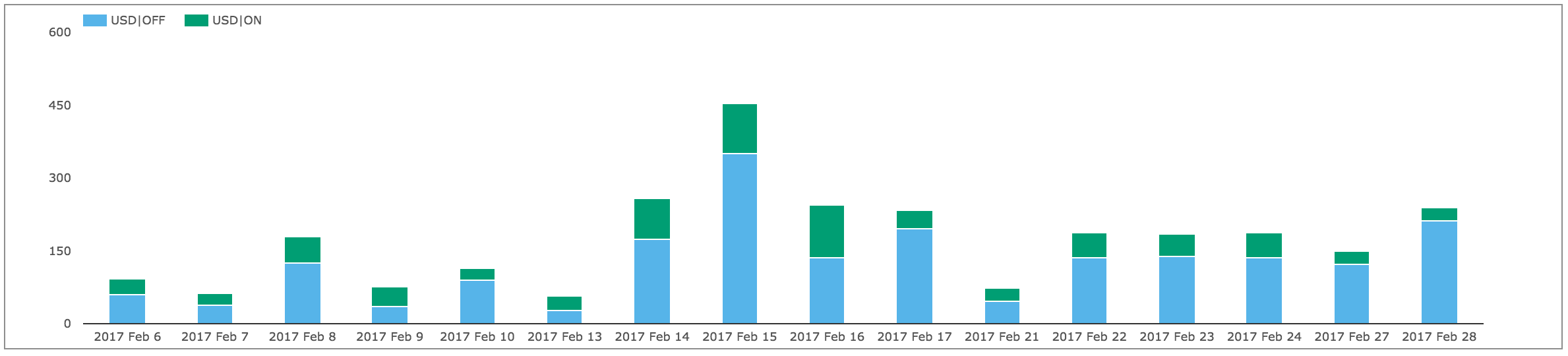

USD IRS ON/OFF SEF

Using SDRView the gross-notional volume (in $billions) of On and Off SEF USD IRS Fixed vs Float price forming trades (Outrights, SpreadOvers, Curve/Flys).

Showing:

- February 2017 On SEF gross notional is > $1,311 billion ($1.3 trillion)

- (recall capped trade rules mean this is understated as the full size of block trades is not disclosed)

- This is 2% higher than February 2016

- February 2017 Off SEF gross notional is > $710 billion

- 16% lower than February 2016

- Overall gross notional was > $2.02 trillion

- And On SEF vs Off SEF is 65% to 35%

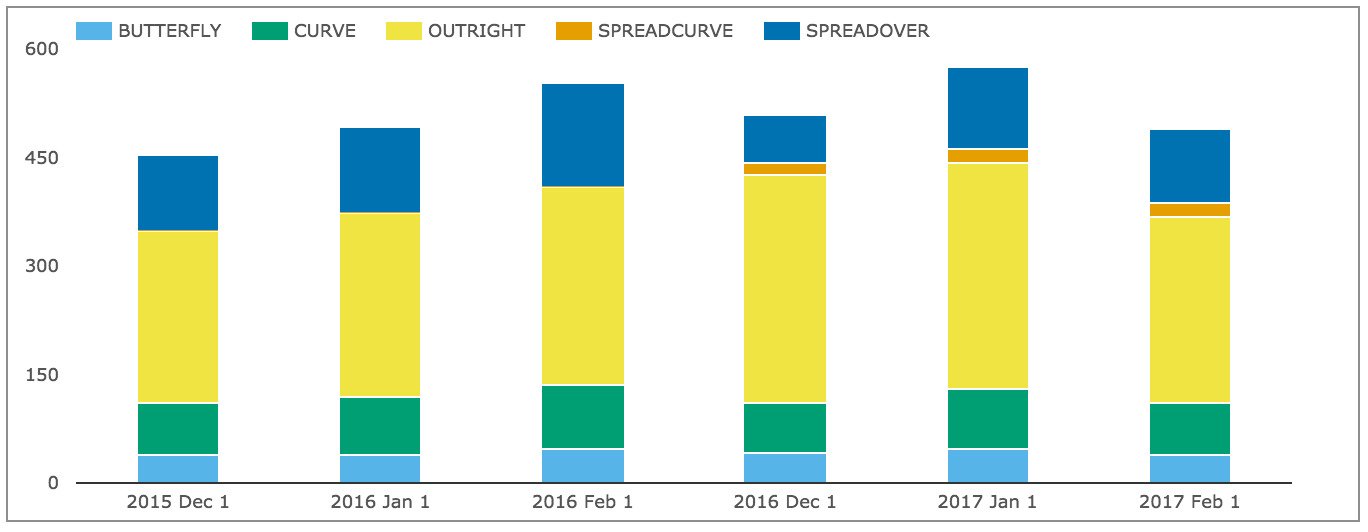

Next splitting by package type and showing On SEF DV01 (adjusted for curves and flys).

Showing:

- In DV01 terms February 2017 was 11% lower than February 2016

- Overall >$490 million of DV01 was traded in the month

- (recall capped trade rules mean this is understated)

- Outrights were 52% and SpreadOvers 21% of DV01

- Curves 15%, Butterflys 8% and SpreadOverCurves 4% of DV01

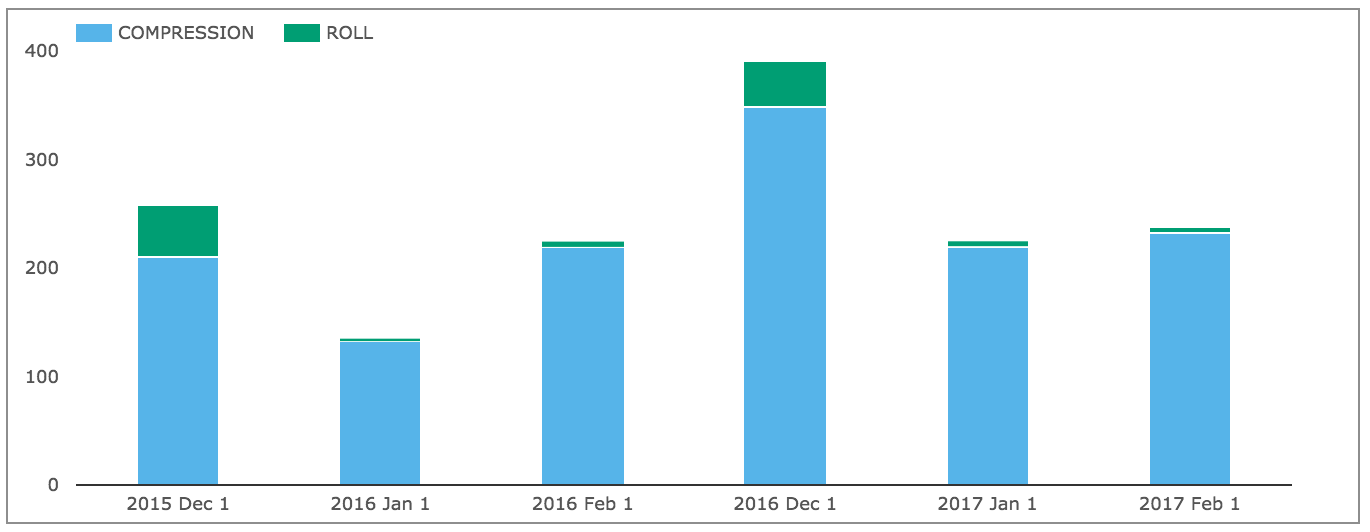

And gross notional of On SEF non-price forming trades; SEF Compression and Rolls.

Showing:

- SEF Compression in February 2017 was > $230 billion

- 6% higher than February 2016 and January 2017

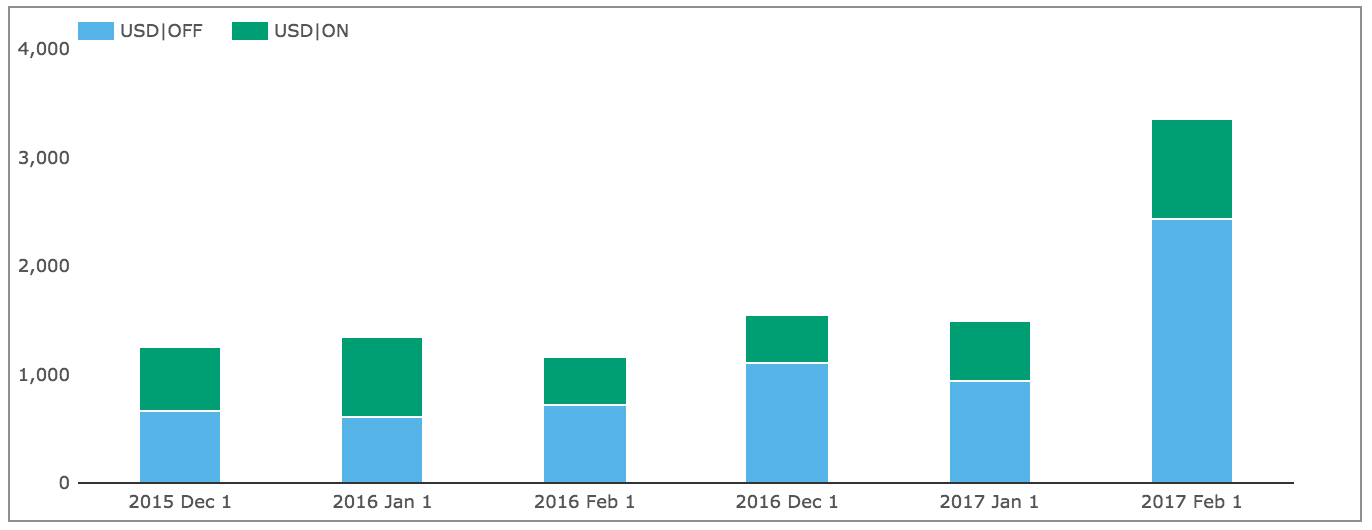

USD OIS Swaps

Next USD OIS Swaps volumes.

Showing:

- February 2017 volumes massively up from prior months

- An overall gross notional of >$3.356 trillion

- (recall capped trade rules mean these are understated as the full size of block trades is not disclosed)

- Almost 3 times higher than February 2016!

- Off SEF gross notional at > $2.4 trillion is 236% higher than February 2016

- On SEF gross notional at > $934 billion is 109% higher

Let’s look at February volumes by day.

Showing that Feb 15th was an unusually high volume day, with > $450 billion and 14th, 16th and 17th were also abnormally high.

Whilst some of these large volumes may be due to positioning or hedging by market participants on expectations of higher interest rates in the US, it also looks like Compression is taking off in OIS swaps. We can see this in SEFView when we look at how much of the USD volumes on TrueEx are made up of OIS. In February, there was a significant spike, suggesting that OIS Compression activity is picking up:

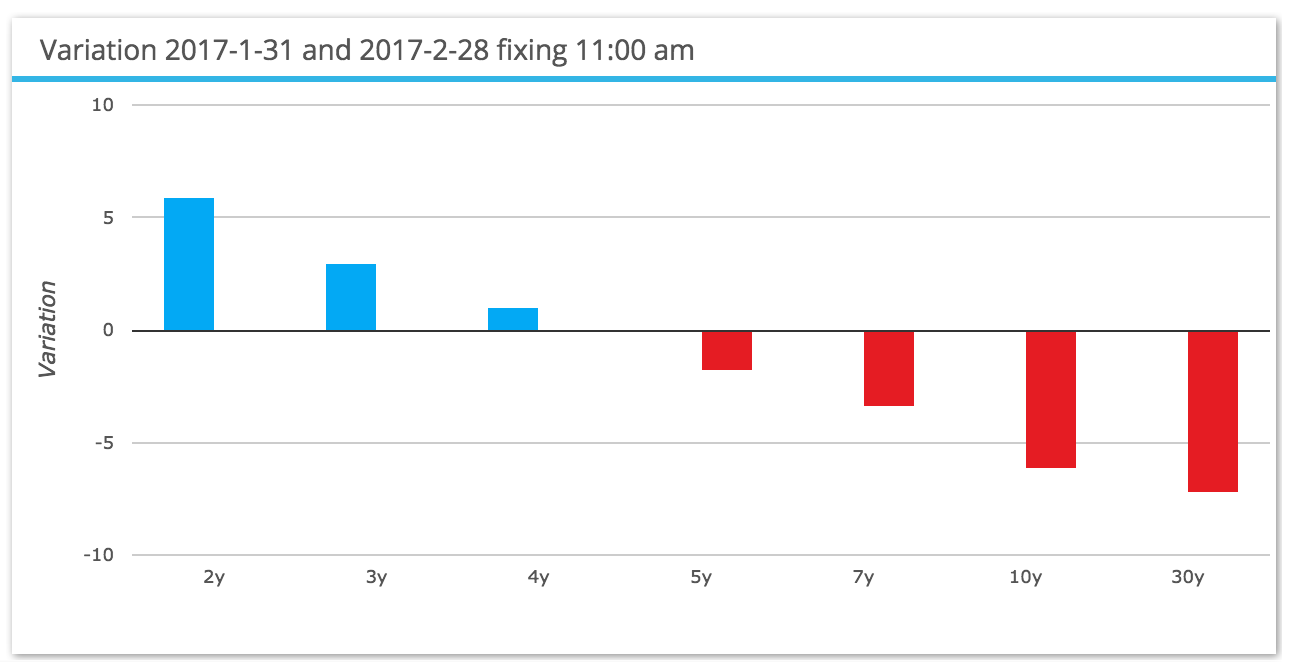

USD IRS Prices

Lets now take a look at what happened to USD Swap rates in the month.

Showing the Swap curve pivoting around 4Y, with short end rate up 6bps and long rates down 7bps.

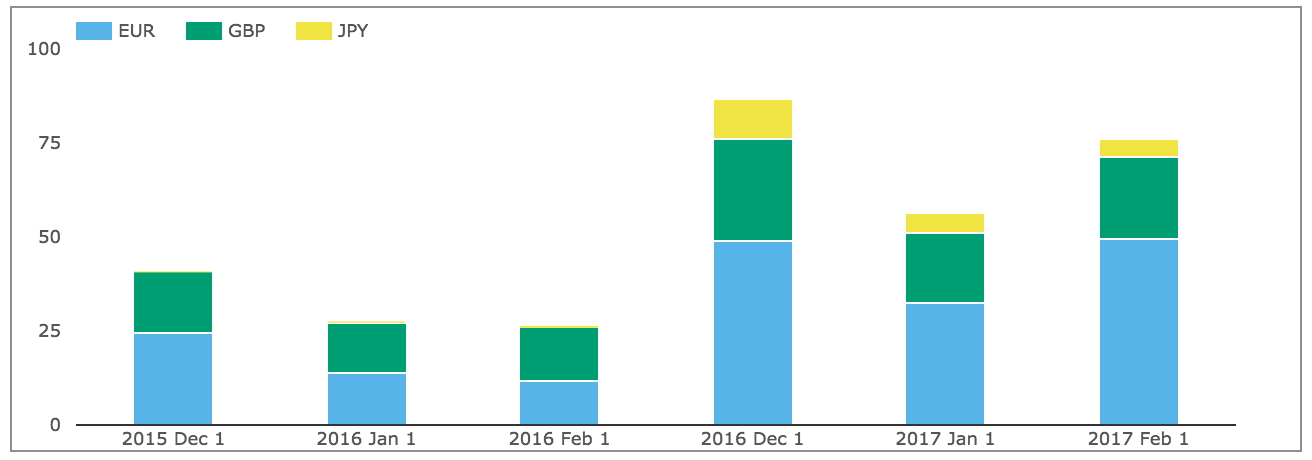

EUR, GBP, JPY Swaps

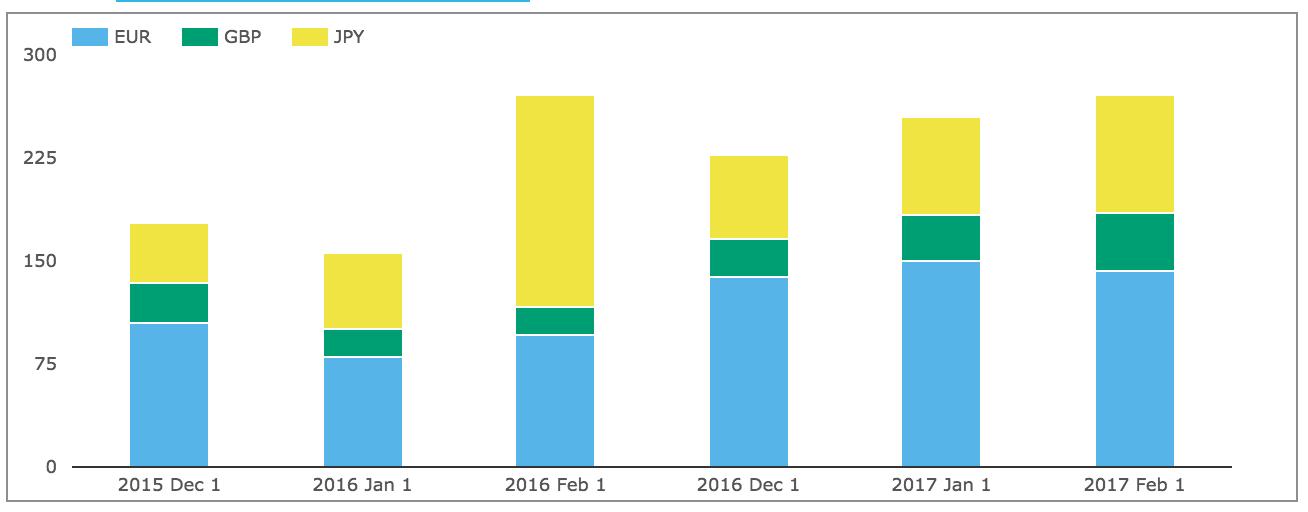

Next On SEF volumes of IRS in the other three major currencies.

Showing:

- Volumes in February 2017 was > $270 billion

- The same as February 2016

- EUR up 48%, GBP up 119% and JPY down 45%.

The overall gross notional in these currencies is 20% of the USD IRS ON SEF volume.

Next SEF Compression activity.

Showing that February 2017 volume was > $75 billion, three times higher than February 2016 and equivalent to 32% of the USD IRS Compression figure of >$230 billion.

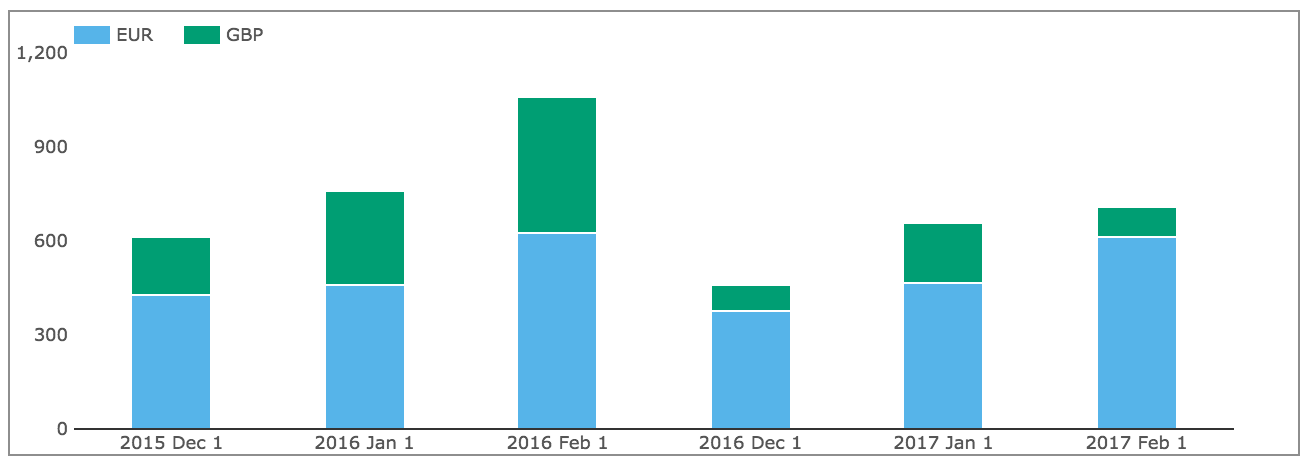

EONIA and SONIA

Next lets check how volumes in EONIA & SONIA have performed.

Showing that February 2017 volume was > $707 billion, up from prior months, but down from February 2017.

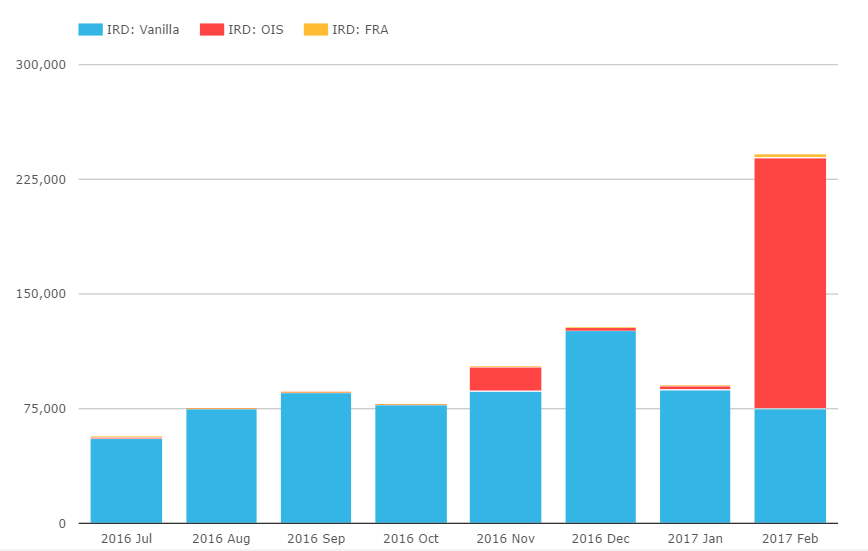

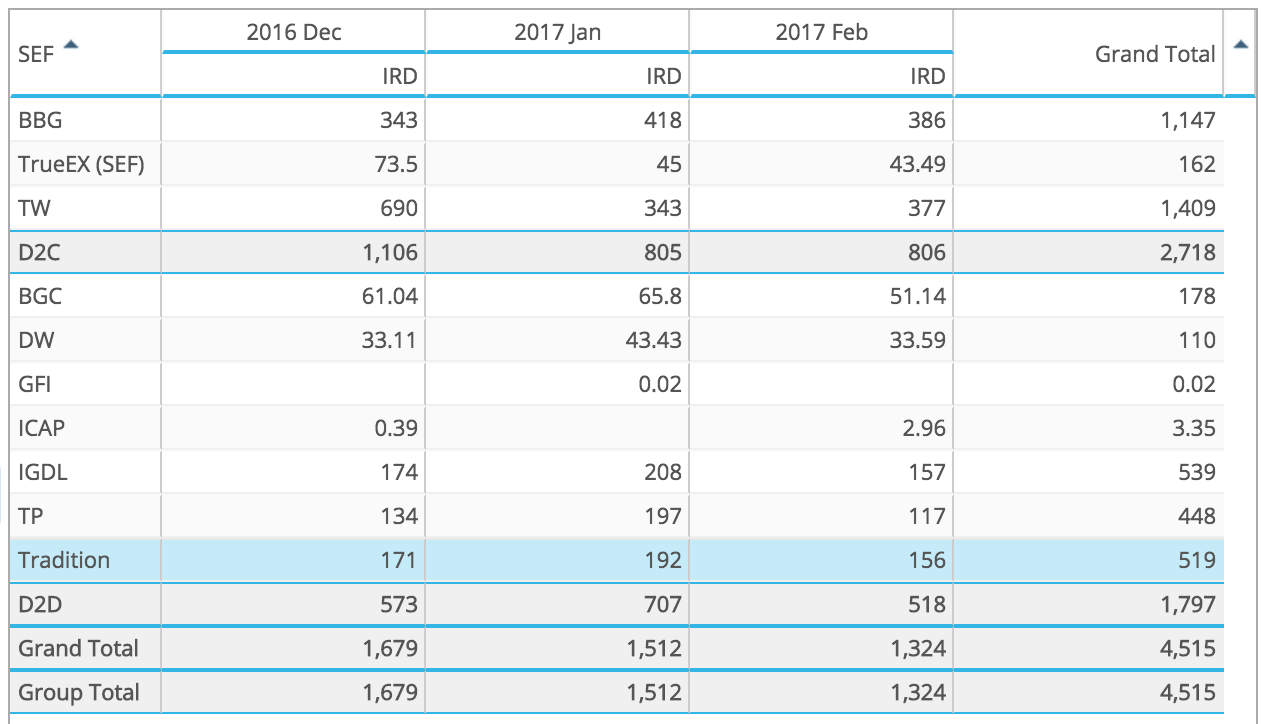

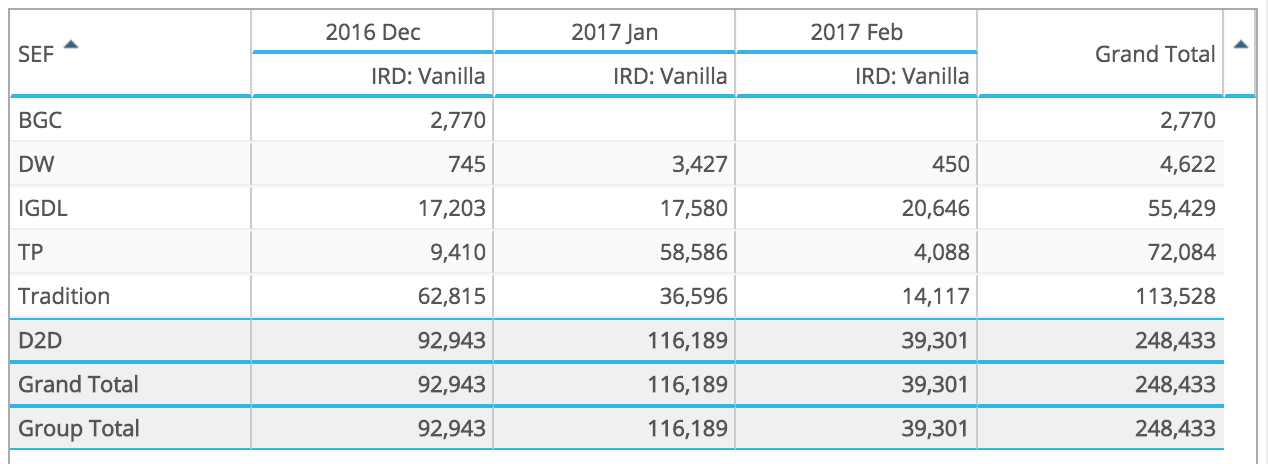

SEF Market Share

Lets now turn to SEFView and SEF Market Share in IRS including Vanilla, Basis and OIS Swaps.

DV01 (in USD millions) by month for USD, EUR, GBP and by each SEF, including SEF Compression trades for the prior three months.

Showing that:

- February volume at $1.3 billion DV01 is lower than the $1.5 billion in Janaury

- Bloomberg is first, just slightly down from the prior month

- Tradeweb is second, up a bit from the prior month

- TrueEx volumes very similar to the prior month

- All the D2D SEFs are down from January

- ICAP and Tradition in the lead and very close in share

- Followed by Tullet, BGC and Dealerweb

In gross notional terms $1.94 trillion of USD IRS traded On SEF in February 2017.

From SDRView data above, we know that $1.3 trillion of price forming capped gross notional and $230 billion of capped compression and roll volumes was reported for On SEF, a total of $1.53 trillion. This is $410 billion less than the $1.94 trillion reported for USD IRS by SEFs.

Put another way the SDR total figure of $1.53 trillion for USD IRS On SEF should be increased by 27% to be equivalent to the actual notional of $1.94 trillion reported by SEFs.

In gross notional terms $1.36 trillion of USD OIS traded On SEF, which is 46% higher than capped notional of $0.93 trillion reported in SDRView.

CCP Basis Spreads and Volumes

In SEFView we can isolate CME Cleared Swap volume at the major D2D SEFs (on the assumption that this is all CME–LCH Switch trade activity). Lets look at this for the past 3 months.

Showing:

- Overall volume in February was $39 billion, massively down from the prior months

- And similar volume to Oct and Nov 2016

- ICAP (IGDL) with the largest volume at $21 billion

- Tradition next at $14 billion

- Tullet with $4 billion

CME-LCH Basis Spreads ended the month at 2.40 bps for 10Y and 3.80 bps for 30Y, both significantly down from 3.30 bps and 5bps respectively.

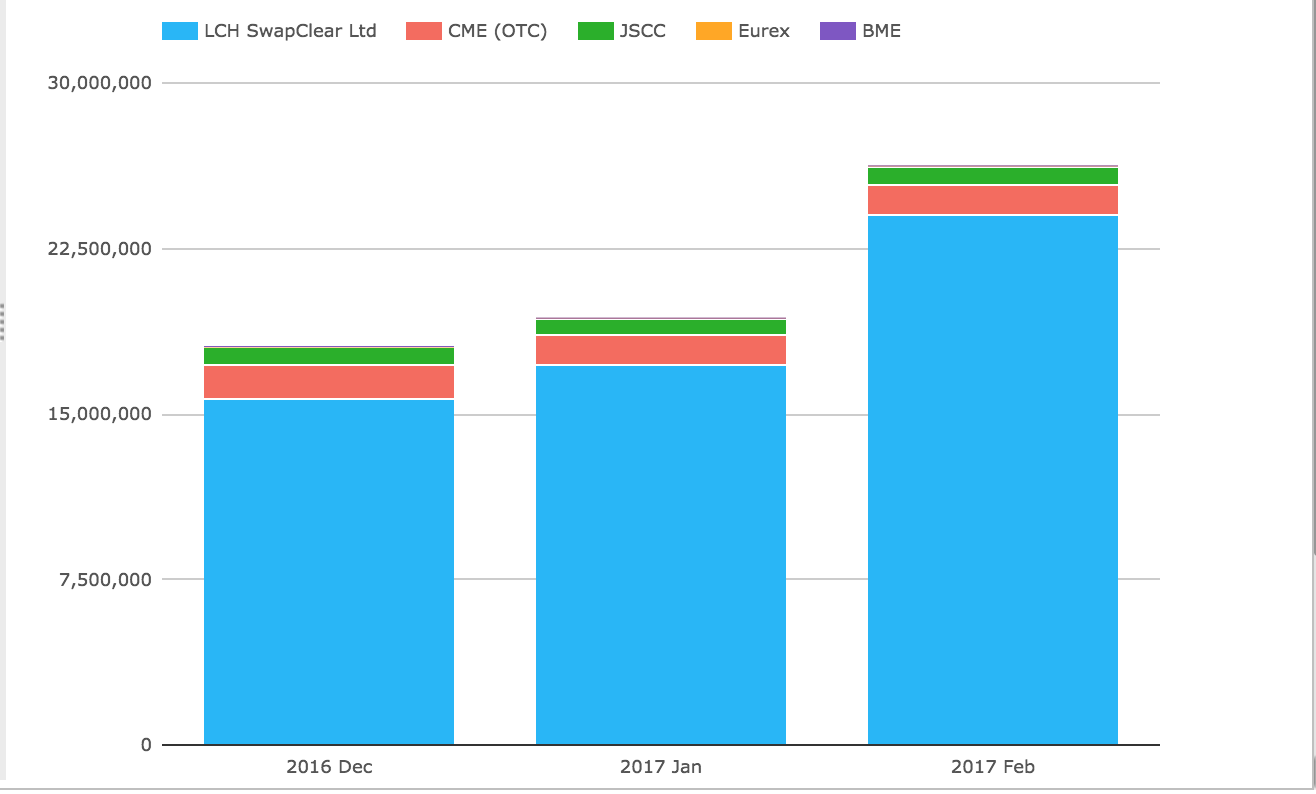

Global Cleared Volumes

Now CCPView Global Cleared Swap Volumes of EUR, GBP, JPY & USD Swaps (IRS, OIS, Basis, ZC, VNS types).

Showing:

- Overall Global Cleared Volumes in February 2017 of $26.3 trillion

- LCH SwapClear volume at $24 trillion, is up a massive 40% or $7 trillion!

- CME volume at $1.3 trillion, is down 9%

- JSCC volume at $866 billion, is up 25%

- Eurex with $42 billion, similar to the prior month

- BME with $16m

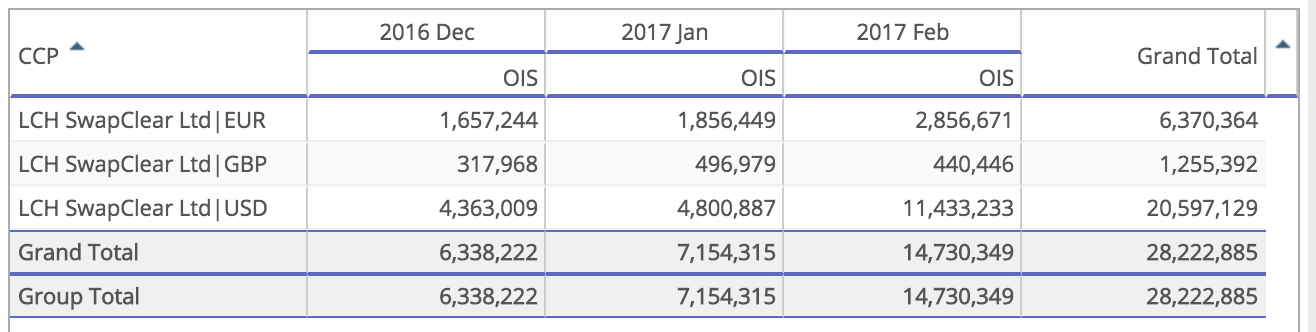

Drilling down on the LCH SwapClear numbers.

We see that the reason for the 40% increase is mostly USD OIS up to $11.4 trillion from $4.8 trillion, reflecting what we saw in SDRView above, as well as an increase in EUR OIS.

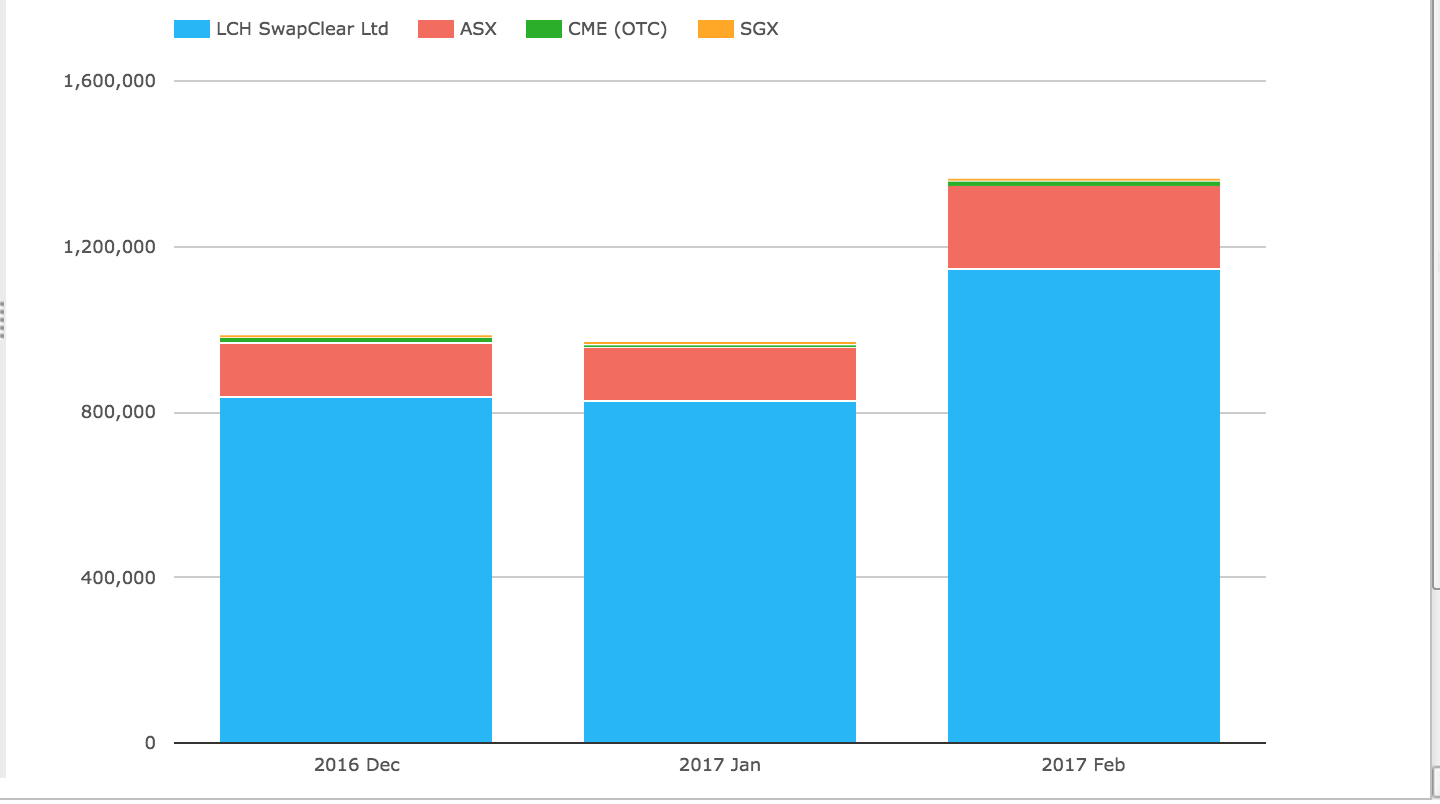

Asia and LatAm

Next the volume of AUD, HKD, SGD Swaps (including Vanilla, OIS, Basis, Zero Coupon).

Showing:

- LCH SwapClear at $1,144 billion up from $820 billion in the prior month

- ASX at $203 billion up from $133 billion

- CME at $13billion up from $5 billion

- SGX at $5 billion, down from $7 billion

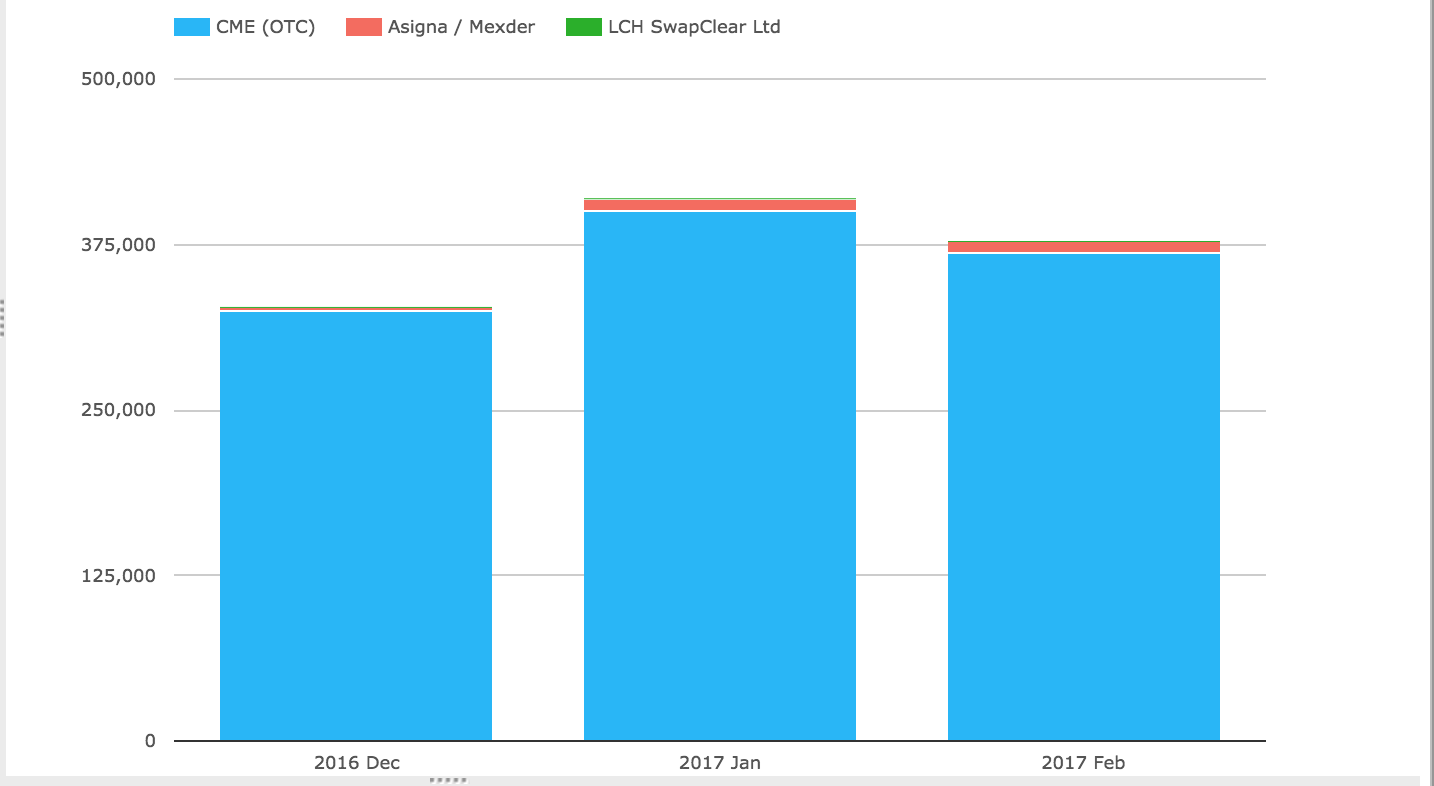

Next the volume of MXN and BRL Swaps.

Showing:

- CME at $368 billion, down from $400 billion in the prior month

- Asigna/Mexder with $9 billion, similar to the prior month billion

- LCH SwapClear showing $829 million up from $124 million (all MXN)

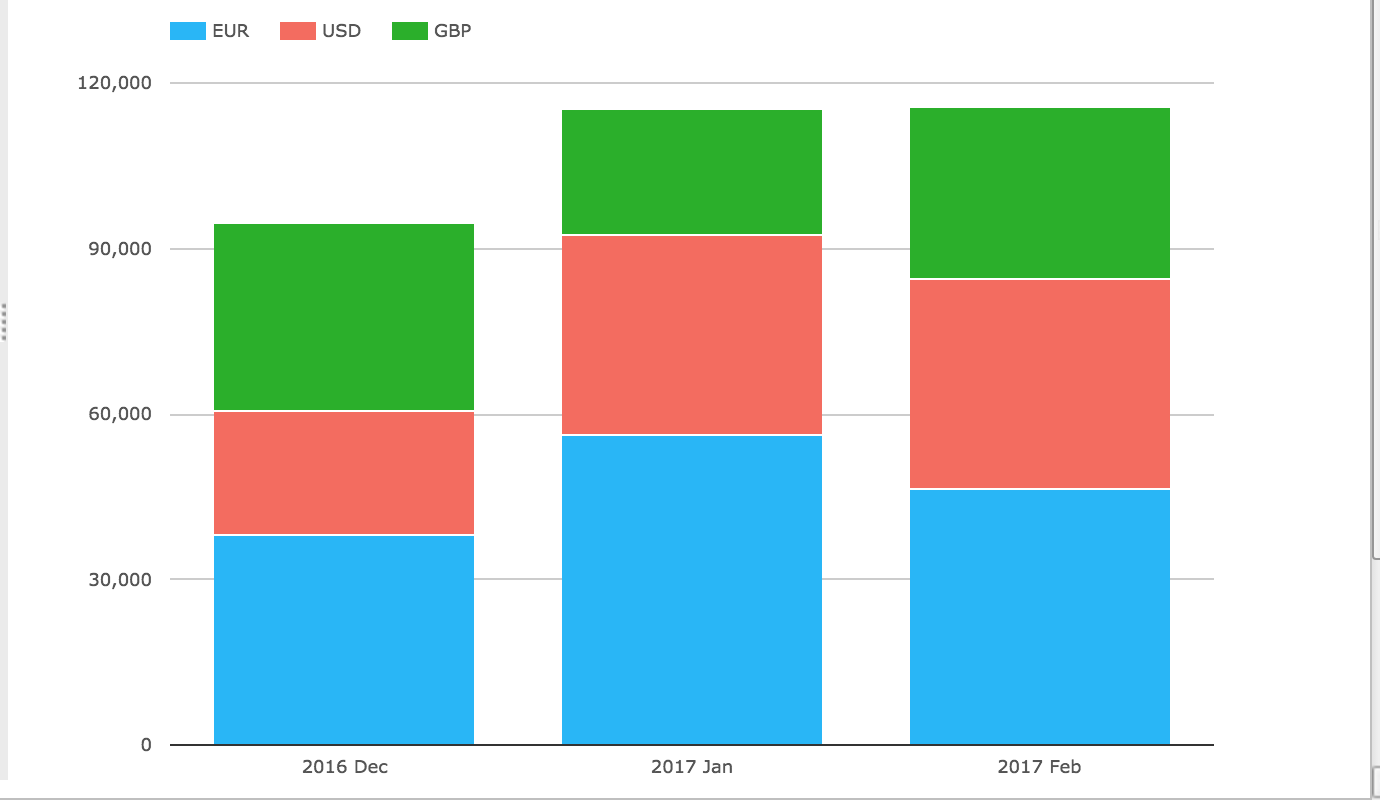

Inflation Swaps

Finally lets look at the two products that have gained the most cleared volume from the Uncleared Margin Rules (UMR), starting with Inflation Swaps.

Showing:

- All the volume is at LCH SwapClear

- Total in February is $115 billion, just above the record in January

- EUR is the largest currency at $46 billion, with USD next at $38 billion

- GBP with $31 billion, increasing from $23 billion

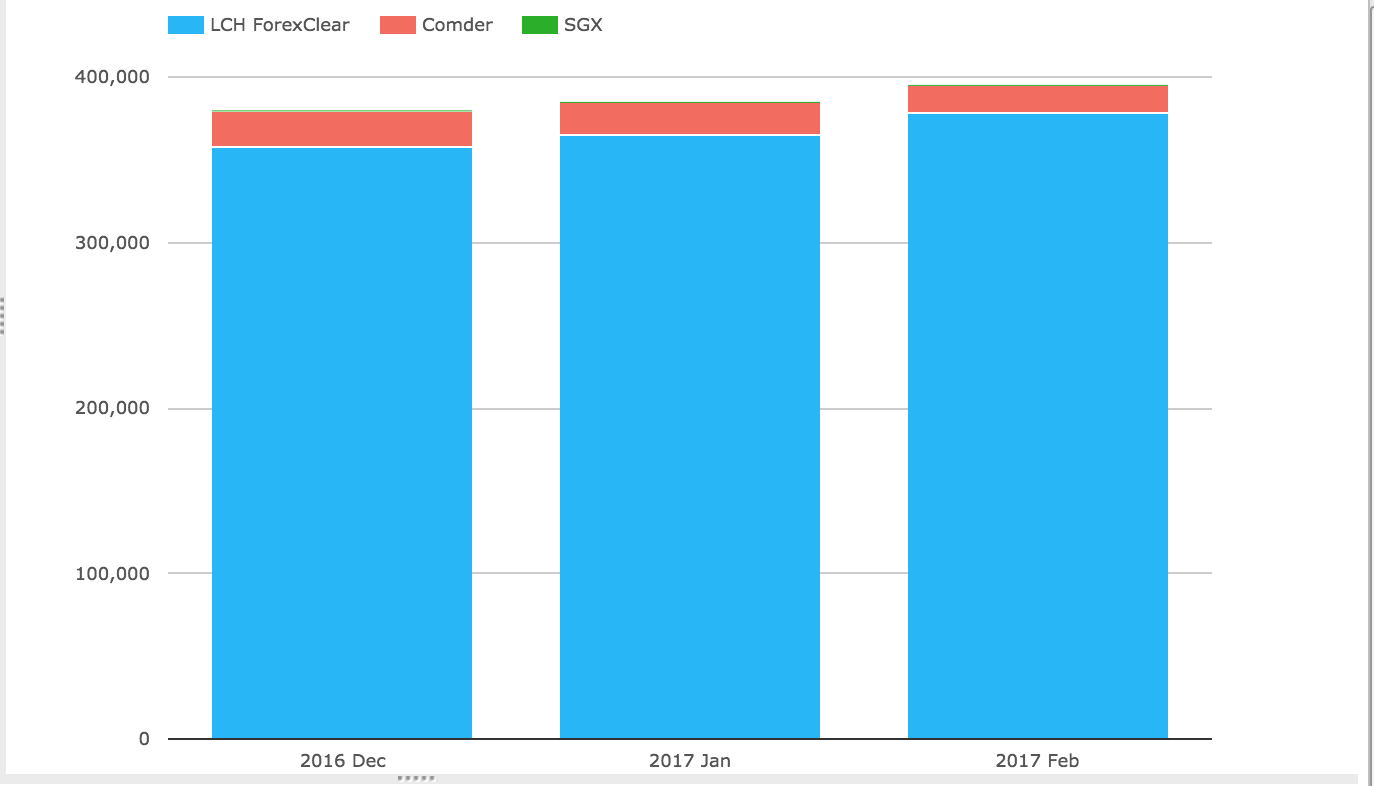

Non-Deliverable Forwards

Showing:

- LCH ForexClear with $378 billion in February

- A new high from November (not shown) with $370 billion

- Comder with $17 billion

- SGX just showing with $6 million

That’s it for today.

Thanks for staying to the end.

Our Swaps review series is published monthly.

Great reviews. Do you have any periodic reviews on Swap Dealers registered with CFTC? the similar articles as FCM Rankings? Many thanks

Thank you for your feedback.

We don’t do reviews on Swap Dealers, but appreciate the idea and will investigate what data is available.