We covered the significant increase in initial margin for cleared GBP Swaps in two recent blogs; How Kwasi Kwarteng has increased your IM and Rishi Sunak and the impact on GBP Swaps IM. In the first of those blogs, Chris added a brief section towards the end on variation margin and I wanted to take a deeper look into this.

Variation margin

A clearing house will each day value and mark-to-market (mtm) all swaps in member and client accounts and either collect or pay the daily mtm change (PL) for each account. This discipline of independant valuation and settling the gain or loss each day in cash is a key risk management discipline in the functioning of a clearing house and reduces the probability of default and systemic risk.

Clearing members and clients need cash liquidity to meet their variation margin call in the currency of the exposure. When markets are volatile, there can be large and unexpected requirements for cash.

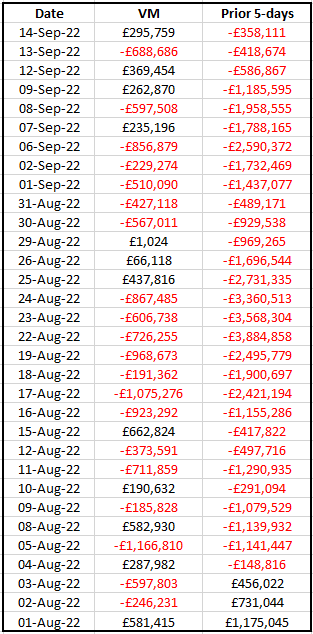

GBP Swaps VM – 1Aug to 14Sep22

Let’s look at the daily VM calls that an account with GBP Swaps would have faced if held over the six week period from 1-Aug-22 to 14-Sep-22. In keeping with our prior blogs, we will use a GBP SONIA 10Y 100million receive fixed swap entered into on 1-Aug-22 at the then par rate of 1.98%.

- Showing in descending date order, the daily VM and the prior 5-days cummulative VM.

- The largest single VM call by the CCP to the member/client was £1.167 million on 5-Aug-22

- The largest single VM paid by the CCP was £0.66 million on 15-Aug-22

- The largest 5-day drawdown by the CCP was £3.9 million (16Aug-22Aug)

- (The IM for this Swap on 1-Aug was £3.8m for house or £4.5m for client)

- Over the 6-week period the cummulative VM was negative £8.5million as 10Y Sonia Swap rates increased from 1.98% to 3.23% and this swaps mtm dropped

Not great, but members or clients would not have had an issue putting up sterling cash for this period.

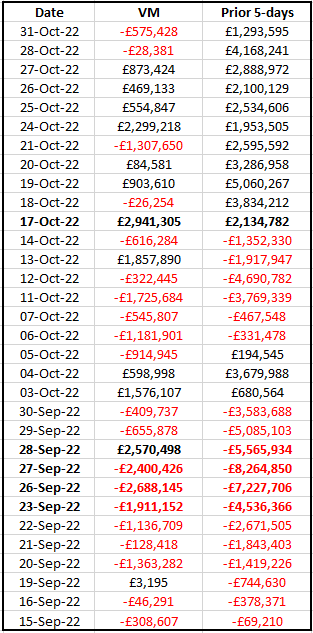

GBP Swaps VM – 15Sep to 31Oct22

Now lets look at the following six weeks, a period of political and market turmoil in GBP rates.

- The largest single VM call by the CCP was £2.69 million on 26-Sep-22

- The largest single VM paid by the CCP was £2.94 million on 17-Oct-22

- The largest 5-day drawdown by the CCP was £8.26 million (21Sep-27Aug)

- The cummulative VM from 20-Sep to 27-Sep was -£9.6 million! (10Y rates up to 4.7%)

- Making the total VM from 1-Aug to 27-Sep a massive -£18.5 million!

- The cummulative VM from 28-Sep to 31-Oct was +£6.4 million, (10Y rates down to 3.8%

- And listing the political and market events on these dates

- 23-Sep-22 was the day Kwasi Kwarteng annonced his now infamous mini-budget

- 28-Sep-22 the BOA Statement to purchase gilts that restored calm and lowered rates

- 14-Oct-22 Kwasi Kwarteng replaced by Jeremy Hunt as Chancellor

- 20-Oct-22 Liz Truss resigned as prime minister

- 24-Oct-22 Rishi Sunak elected as prime minister

Pension Funds and LDI

Let’s extrapolate the above to what liquidity needs a Pension fund with an LDI strategy use swaps would have faced. For that we need to use a more representative £1 billion 10Y receive fixed swap, that would have been held by the pension fund.

- 1-Aug to 14-Sep, £85 million cash needed over 6-weeks for variation margin calls

- Painful, but manageble

- A sudden increase from 20-Sep to 27-Sep, a 6-day period with a further £96 million needed!

- Shock and awe and discussion reaching C-level executives

- It is the large daily moves on consecutive days that caused liquidity stress

- Resulting in the need to sell assets, in this case UK gilts, which further drove down prices and increased GBP rates, until there were no buyers for long dated UK gilts, …

- Not a good place to be

- Then the BOE stepped in on 28-Sep-22 to restore calm and rates dropped back

So while the IM increase we covered in prior blogs wwas costly, it is the VM calls that caused liquidity stress and contributed to the case for Central bank intervention to restore order.

I seem to recall Kwasi Kwarteng saying, “the markets will do what they do” under questioning in the house of commons on the impact his mini-budget had; a statement that he made to make the case for ignoring short term market volatility when setting fiscal policy, but one that came true in an entirely different manner.

I can’t help but end with the now infamous 1990’s quote by James Carville (Bill Clinton’s chief strategist) , “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.“

That’s all for today.