- Initial Margin for GBP swaps has increased by up to 65% due to the mini-budget.

- 5 of the 6 largest ever moves in GBP rates have occurred during September 2022, since the mini-budget.

- We look at Initial Margin models and how IM has changed over time.

- It is fair to say that GBP Swap markets have never seen a month like it before!

For those who know, this blog pretty much writes itself. Tod wrote a very similar blog 6 years ago:

Let’s crack on with the analysis and look at the scenarios that now drive Initial Margin for GBP SONIA swaps cleared at LCH.

The Numbers

Initial Margin Required

After the shock and awe of the mini-budget and then the incredible U-Turn, Initial Margins for centrally cleared interest rate swaps in GBP markets have fundamentally changed.

Remember that these swaps are subject to Clearing Mandates, therefore if you are active in this market you have felt this pain. How much upfront Initial Margin now needs to be posted?

We run the analytics in CHARM to find out.

Receive Fixed GBP Swap

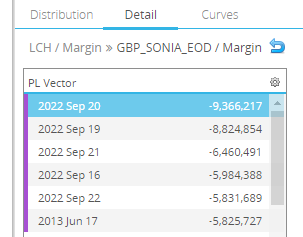

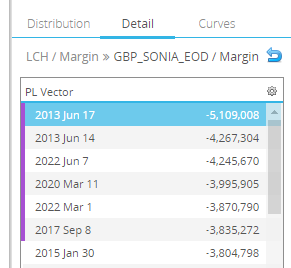

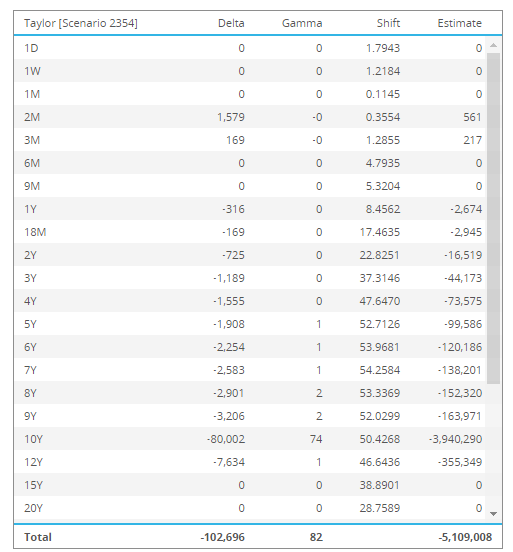

The Initial Margin required to trade a standalone GBP100m 10Y Receive Fixed SONIA swap at LCH now stands at GBP7.180m (equivalent to about 86bp of risk). From CHARM:

Showing;

- LCH take the average of the six worst historic moves to calculate the Initial Margin on a swap.

- For a Receive Fixed Swap, this means looking at periods when Rates have increased (a Receiver loses money when interest rates move higher).

- These are market moves over a 5 day period – a so-called 5 day “PnL vector”.

- Incredibly, as we stand today, 5 of those 6 worst EVER 5 day moves for a Receive Fixed swap were in September 2022, as a result of the mini-budget shock.

- Even more incredibly, all of those 5 moves were larger in magnitude than any prior increase in rates.

- The previous worst day was way back on June 17th 2013. Anyone remember the cause?

- Nothing else has caused Rates to spike so high in such a short period of time.

Pay Fixed GBP Swap

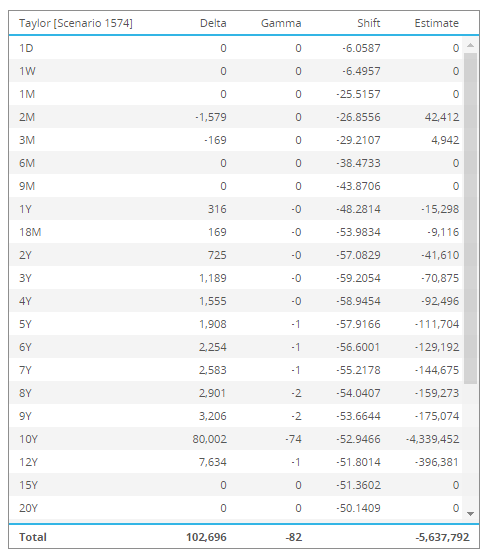

The Initial Margin required to trade a standalone GBP100m 10Y Pay Fixed SONIA swap at LCH now stands at GBP5.308m (equivalent to about 63bp of risk). From CHARM:

Showing;

- The six worst 5-day moves for a pay fixed swap – i.e. the times when Rates have moved lower by a lot.

- The 4 worst days for UK rates were all around the Brexit referendum result. What a shock that was!

- Whilst interest rates crashed due to Lehman, due to the European debt crisis, due to the COVID pandemic (!) they did not move the needle (in GBP rates) as much as Brexit.

- But wait, we do have two days in 2022 that also make the cut – June and February this year. February I guess was the Russian invasion of Ukraine. June I struggle to pinpoint the cause?

- Crucially, we have no appearance of dates since the mini-budget. The wild moves in price have been one directional – and so Pay Fixed positions have so far been unaffected by the government’s fiscal policy.

Initial Margin changes over time

The Pay Fixed swap above was taken as at October 4th. We can look at the same swap on September 1st, one month ago. We find that it had exactly the same scenario dates driving Initial Margin (as it should, there are no recent events that have changed the economics of a pay fixed position):

The precise PnL vectors are slightly different as we are now at different levels of interest rates. This means the DV01 (and hence discounting of cashflows) occur at different rates, as do the relative shifts of interest rates. These all alter the PnL vectors.

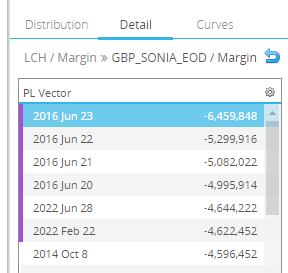

However, turning to a Receive Fixed swap, and the scenarios were of course different on 1st September – the mini-budget and ensuing market mayhem hadn’t happened yet!

Incredibly, even on September 1st we had four scenarios in 2022 driving the Initial Margin on a Receive Fixed swap! August 15th -17th this year all made the cut, as did June 7th.

This tells us that 2022 has been an incredibly volatile year for GBP swaps. Market participants are witnessing all-time record moves frequently. This may be due to the fact that interest rates are now higher than at any time since Lehman. The brutal end to a Fixed Income bull market is well represented by the long-term Bloomberg chart of 10Y SONIA swaps:

It may also be model specific – are CCPs using absolute or relative moves to drive Initial Margin, do they weight recent market moves more strongly? These are all risk management decisions that a CCP (and to some extent their regulators) must make.

For GBP Swap markets, this underlying volatility is occurring against a backdrop of falling GBP swap volumes. That is quite an unusual scenario.

Initial Margin Time-Series

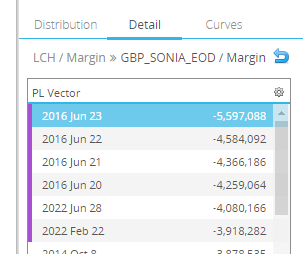

Now let’s go all the way back to August 1st 2022 and look at a Receive Fixed swap and its initial margin requirement of GBP4.36m:

The market moves causing the most severe tail event were about 50-55 basis points on the curve:

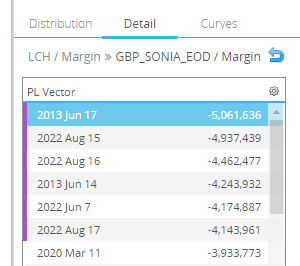

The opposite position (Pay Fixed swap) on August 1st was still being driven by events in 2016 (Brexit), with very similar PnL vectors to the Receive Fixed position above:

However, ever since, the Initial Margin requirements for these two positions have diverged significantly.

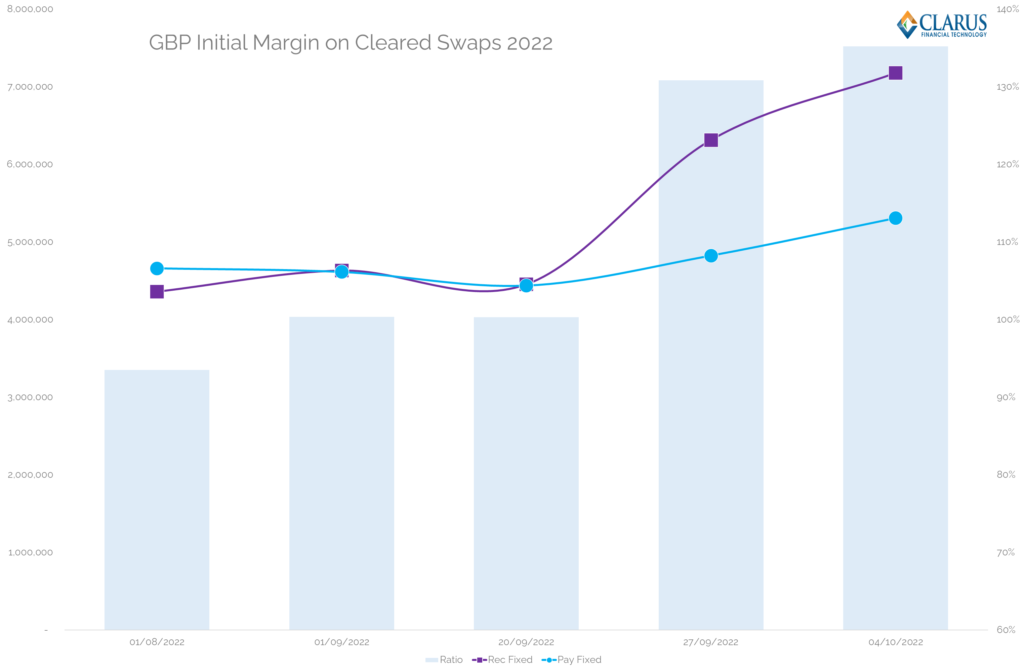

Unlike ISDA SIMM, Initial Margin posting is not symmetrical between Payers and Receivers for CCP Initial Margin models. What this all means is that Initial Margin calls have become incredibly asymmetric since the mini-budget:

Showing;

- Since August 1st, the Initial Margin required for a Receive Fixed swap has increased by 65%!

- The Initial Margin required for a Pay Fixed swap has increased by 14% over the same time period (as Rates have moved higher, therefore the relative moves in Rates are expected to be higher in higher rate environments).

- The IM required for a Pay or Receive Fixed position was almost identical at the beginning of September.

- Now, 35% more IM must be posted to hold a Receive Fixed GBP IRS than the equal but opposite Pay Fixed position.

To be clear this is expected behaviour:

- It is dictated by the Initial Margin model chosen by the CCP.

- It is predictable – that’s why I knew the numbers would make it an interesting blog.

- We cannot just “make up” scenarios for a model based on past observations. So this asymmetry is to be expected, and has likely been seen previously to the benefit of Receive Fixed positions.

- You just have to look at how many recent events make their way into the Fixed Income sell-offs to see that previously all of our biggest moves were risk-off moves with Rates headed lower.

However, we do need to bear in mind that:

- Posting more IM is more costly.

- More IM reduces leverage.

- It can make certain positions (in this case paying fixed) relatively more attractive.

Variation Margin

Finally – this is not Variation Margin here. All of the articles you have read about UK LDI are related to Variation Margin. We are not talking about VM in today’s blog.

Variation Margin (VM) is the liquidity draw necessary to hold onto losing positions when markets are so volatile. We’ve written about the difference between VM and IM during the COVID Pandemic previously. VM is the effective daily cash settlement of market moves, and crucially can be re-used. Initial Margin is the long-term funding cost associated with holding a position, and it cannot be reposted. IM is therefore typically considered very expensive. A sudden daily liquidity draw for VM could also be very expensive, depending on the resources available to you (and the directionality of your portfolio).

In Summary

- Initial Margin for GBP swaps has increased by up to 65% due to the mini-budget.

- 5 of the 6 largest ever moves in GBP rates have occurred during September 2022, since the mini-budget.

- When GBP swap traders say that they have “never seen a day like it before”, the Initial Margin models prove that they are right!

- 2022 has been an incredibly volatile year for GBP rates.

- But as we have blogged previously, volumes have not been great.

- This suggests that trading conditions are very difficult in this particular market.