- ISDA SIMM version 2.0 is coming in December 2017.

- Re-calibration and new risk factors will mean Initial Margin changes for all portfolios.

- SIMM for Excel gives you the tools to understand and model these changes.

- Quickly compare before/after SIMM levels in Excel.

- Drill-down into Counterparty and Risk Factor levels.

- Perform your own analysis and optimisation from Excel.

- Sign up for your free trial to test the impact ISDA SIMM v2.0 will have on your portfolio.

Version 2.0

ISDA have announced ISDA SIMM v2.0. The press release tells you all you ne

- New products have been added which introduce new risk factors.

- Risk weights have been recalibrated for all products.

- It goes live as of December 4th 2017.

This is the 4th iteration of the ISDA SIMM model. Our Clarus calculators support all versions of the model (yes, we are live with 2.0 already), and our tools are designed to give quick and easy comparisons between the models.

Sign up now for your free trial to test the impact ISDA SIMM v2.0 will have on your portfolio.

It’s not just a calibration

But the reality of introducing a new IM model to cover all OTC derivatives, from scratch, is far more daunting than that. As large banks continue to back-test their portfolios and report those results to local regulators, the process of refining the model, adding risk factors and identifying gaps is bound to continue. The reality of maintaining an ISDA SIMM solution for software providers begins to bite from v2.0 onwards.

Luckily, we are strong advocates of ISDA SIMM at Clarus. We have had v2.0 live across our products for a few months now. We are well acquainted with it.

Today’s blog will look at some of the changes and how you can analyse them using SIMM for Excel.

Your Margin will change under SIMM 2.0

As with all multi-asset models, a recalibration exercise can cause unexpected changes in margin levels. These can be up or down. It is therefore important to have the tools at your disposal that explain these changes, allowing you to drill-down into the numbers and get to the root cause of the changes.

SIMM for Excel, encompassing our Clarus functions in Excel, allows you to do exactly this. I constructed a simple SIMM Compare worksheet to compare v2.0 to the predecessor models. I would be happy to share this workbook with any of our current trialists and subscribers – feel free to reach out to me.

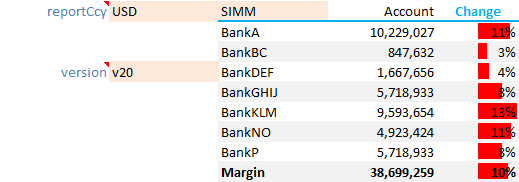

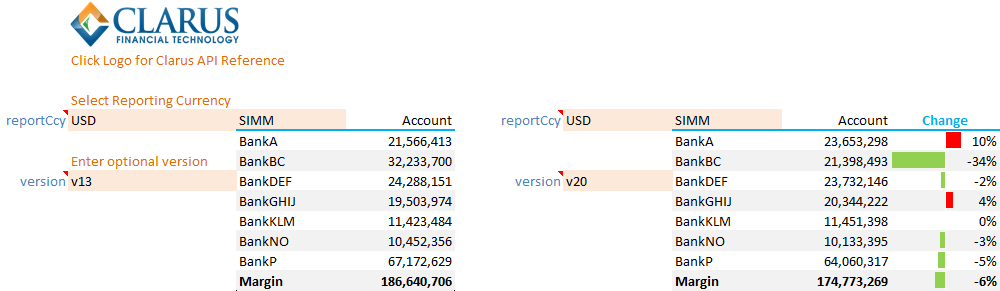

Per Counterparty Changes

Hands up, I thought this was going to be an easy blog this week. All I care about is how much my margin changes between counterparties, right?

Showing;

- ISDA SIMM Initial Margin versus 7 counterparties under version 1.3 on the left hand side.

- ISDA SIMM v2.0 margin on the right hand side.

- It looks like I save 6% in Initial Margin for this sample account. Great!

- But then I realised I have no idea why, how or whether this is likely to still be the case come December.

Basically, it is a classic example of being given a little bit of information but immediately needing to know more.

Is your SIMM tool limited to providing only output calculations? The Clarus tool is far more flexible than that.

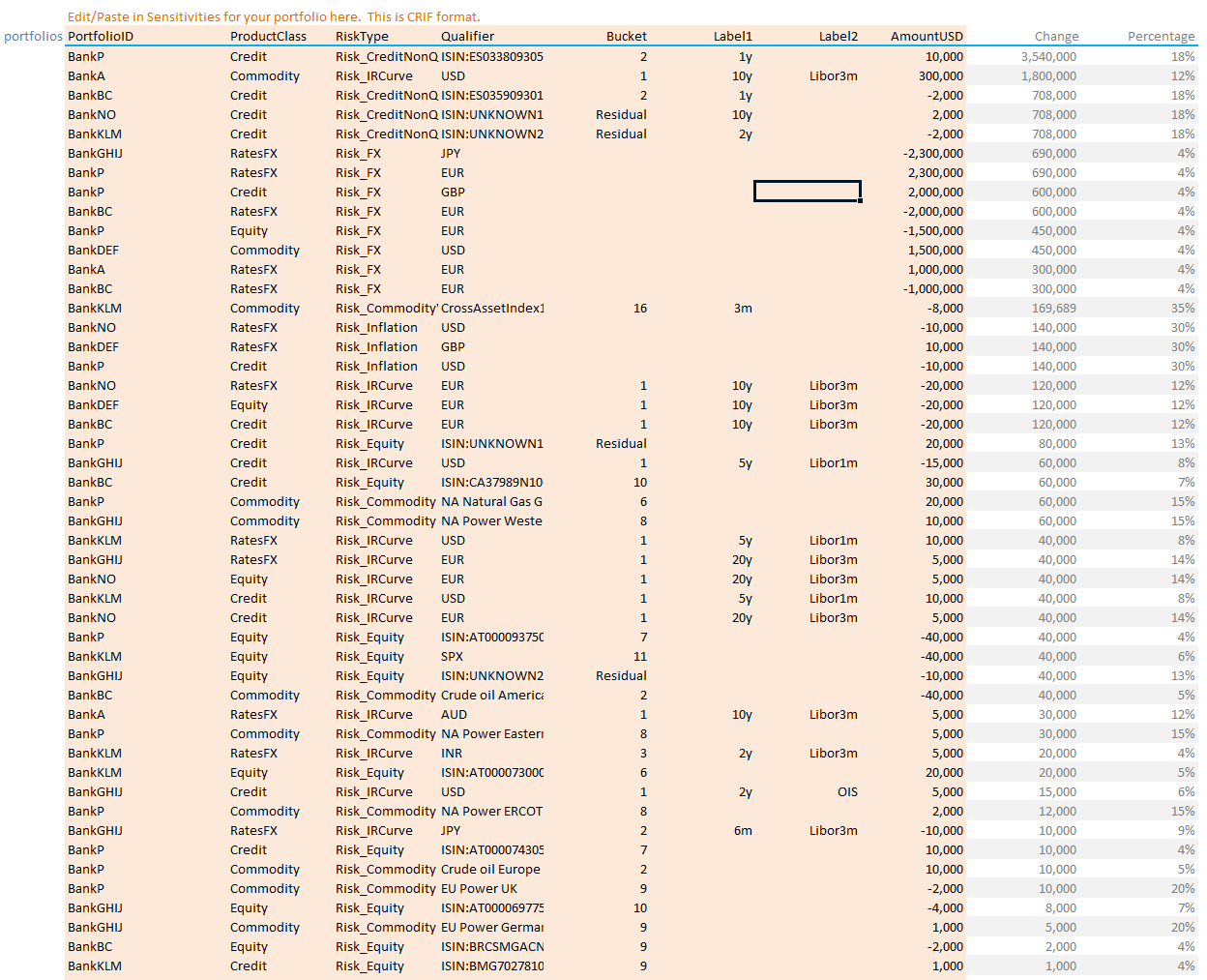

Risk Factor Changes

I wanted to understand these changes. So I turned to Excel and the SIMM_MARGIN function to solve this. By calculating SIMM margin on each trade as if it were a standalone trade, I can see which risk factors are causing the biggest changes:

Showing;

- My input CRIF file, and the change in IM required between v1.3 and v2.0.

- Absolute changes in Margin are somewhat related to the total size of my risk factor. So the majority of the large impacts are from FX.

- These types of changes are pretty straightforward to interpret from the change in risk factors themselves, hence I have included the percentage changes as well.

- For example, inflation risk factors have gone up considerably.

- And there are large changes in the Credit and Commodity Product Classes.

- There have been some re-classifications of credit assets as well.

These changes are difficult to appreciate without the right analytics. This is where SIMM for Excel comes in.

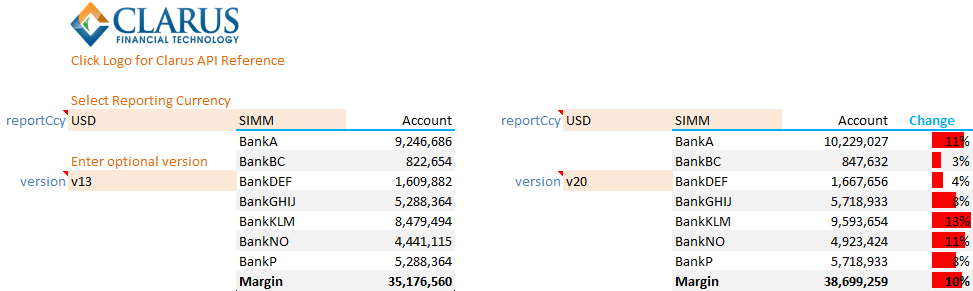

A sample Cross Currency Book for What-If Analysis

A “typical” cross currency book is likely to be hit particularly hard by the changes in risk weights;

- Cross Currency books will almost certainly see higher margins under ISDA SIMM v2.0.

- For all risk factors in this portfolio, risk factors have moved higher.

- These are easily observed in Cross Currency basis.

As a result, the shift to ISDA SIMM v2.0 is particularly painful:

Showing;

- An increase across all counterparties, despite a seemingly innocuous portfolio.

- An overall increase of 10%.

- To be clear, this isn’t due to directionality of the portfolio.

- To manage the risk, the dispersion of risks across counterparties must be managed.

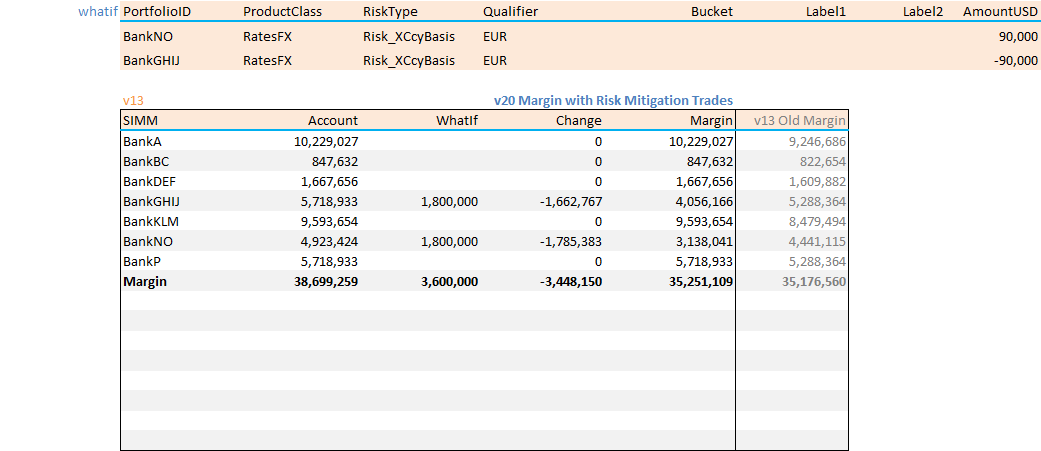

As an example, to ensure that our margin doesn’t increase due to SIMM v2.0 we could do a risk-mitigation trade between BankNO and BankGHIJ in EURUSD basis:

Showing;

- I need to pay the basis versus BankNO

- I need to receive the basis versus BankGHIJ

- This is “easier” in cross currency basis than other risk factors because there is only a single risk vector across the whole curve. I am maturity agnostic. I could even do 5 years versus Bank NO and 10 years versus Bank GHIJ if I was axed.

- The resulting MVA credit to my book should mean that I am particularly motivated to do these particular trades.

- SIMM for Excel enables me to run these What-If trades on my portfolio to judge the impact.

In Summary

To manage the transition to ISDA SIMM v2.0, I need analytics that:

- Performs fast, reliable calculations.

- Enables me to compare different model versions to the upcoming ISDA SIMM v2.0.

- Breaks down my portfolio risks into counterparties.

- Breaks down my counterparty risks into risk factors.

- Runs what-if trades against different counterparties, different risk factors, different SIMM models.

- Gives me the tools to perform my own, self-directed analysis/optimisations. Excel is still yet to be beat for this kind of thing.

This is why you need SIMM for Excel from Clarus. Sign up for your free trial today.