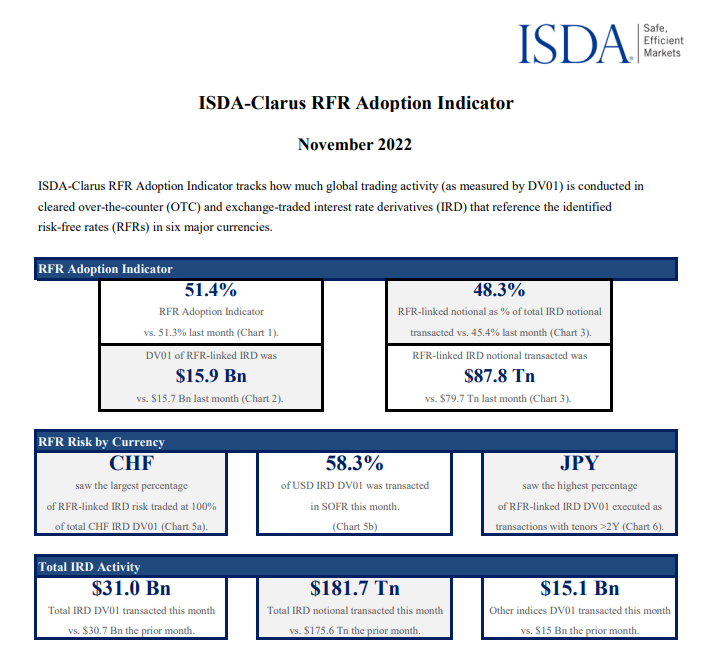

- The ISDA-Clarus RFR Adoption Indicator was 51.4% last month.

- This is the fourth consecutive month that it has remained around 51%.

- SOFR adoption hit a new all-time of 58.3%.

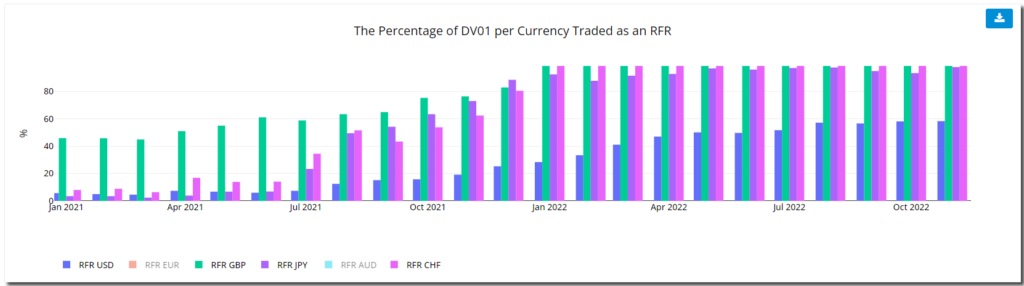

- €STR adoption remains volatile.

- Following on from our last blog, we take a look at AONIA.

The ISDA-Clarus RFR Adoption Indicator for November 2022 has now been published.

Showing;

- The index has increased slightly to 51.4%, almost unchanged for 4 months now!

- SOFR adoption hit a new record high at 58.3%, marginally higher than last month.

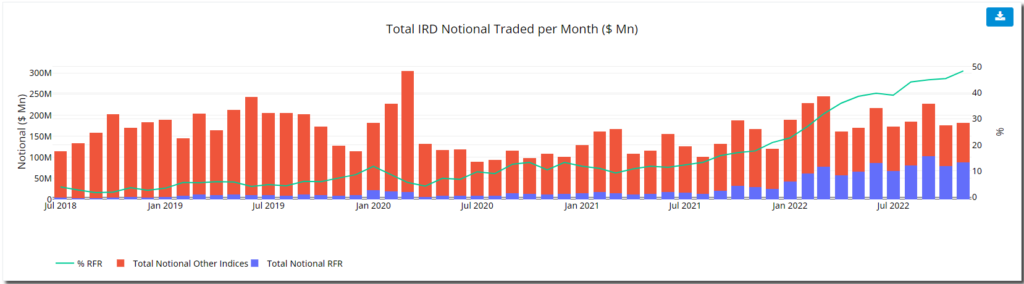

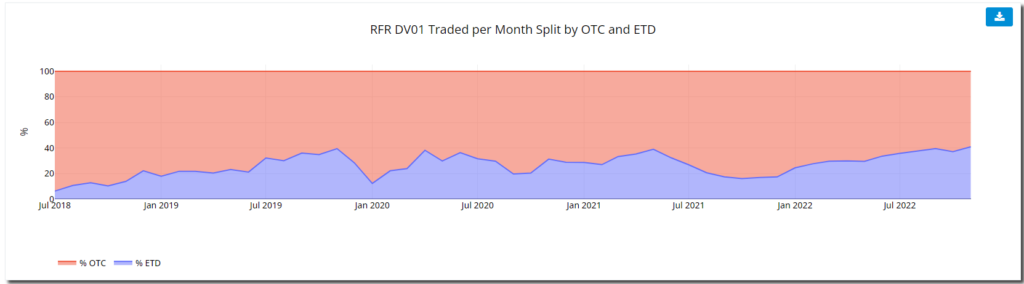

- 48% of total activity by notional was vs RFRs, a new record.

- We saw more trading activity in Futures, accounting for 41% of all RFR risk – an all-time record.

Is History Repeating?

Groundhog Day appears to be a traditional film that isn’t actually set at Christmas but is associated with this time of year. RFR Adoption is somewhat similar – in the run up to the end of 2021, it was all anyone spoke about (well, in certain circles!) and regulators choosing a year-end cut-off for (most) LIBORs just seemed so cruel to the industry that I doubt anyone will forget it in a hurry.

In light of which, I checked back on my blog covering November 2021 to remind myself just how slow RFR Adoption was, even with just ~ 20 days to go:

Regular readers will not be surprised at the level of hyperbole as we tried to promote the move to RFRs as early as possible. Avoiding event risks is just good risk management after all.

However, RFR adoption was still down in a 62-76% range for the three currencies staring cessation in the face (GBP, CHF & JPY). Should we be surprised, therefore, that with 6 months still to go, USD SOFR adoption is “only” at 58.3% but increasing slowly month-on-month? It is entirely in-keeping with previous experience.

For USD in November 2022, we need to look back at GBP in June 2021. Back then, SONIA made up 61% of the market, and it even fell the following month to 59%. USD SOFR adoption seems to be following a very similar course, which is why it has reached a “natural plateau” these days around 58%. It seems to be how the cycle works. It doesn’t half make it hard to write blogs about it though!

In Positive News

We do have positive movement in the market, without any tenuous links to 1990s films! As measured by notional, the proportion of the market trading in RFRs just keeps on increasing, this month reaching a new high at 48.3%:

And in related news, the proportion of RFR risk that was traded as a Futures contract (“ETD) increased to a new all-time high of 41%:

These two facts are somewhat linked – more futures trading in RFR means more of the short-end risk they are associated with is moving to e.g. SOFR. This in turn increases the amount of notional traded as RFRs without really moving the needle on our preferred DV01 (risk) metrics.

It is still somewhat puzzling that we can have positive momentum in a couple of key metrics (as well as a new high in SOFR adoption) and yet the headline Adoption Indicator remains static.

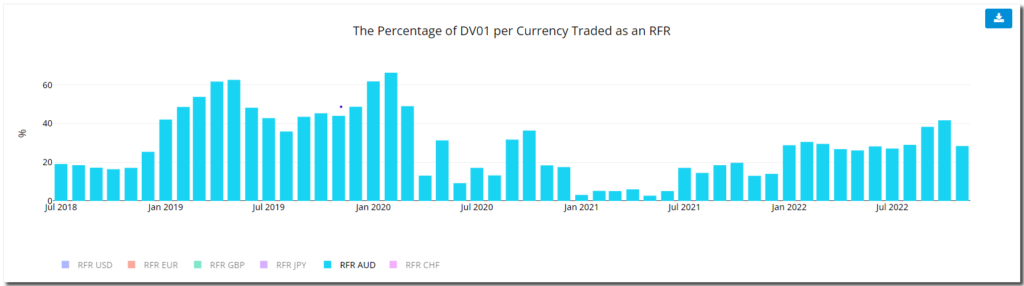

AONIA

One of the metrics pulling the Adoption Indicator lower this month was AUD trading. The amount of risk traded as AONIA in any given month is very volatile – take a look below:

Showing;

- AONIA accounted for 66% of all AUD risk way back in February 2020.

- It sank back to 3% as recently as May 2021. I told you it was volatile!

- This year, the trend had been gradually higher…until November.

- With such a volatile time-series it seems entirely down to market expectations of rates and RBA action – without much consideration to market structure or simplifying the AUD curve.

The reason I’ve spent a bit of time on AUD this week is because AUD and EUR likely have similar dynamics. It looks like the term rates are going to continue, but the market is beginning to show signs of choosing to trade the RFR. Will the RFRs gain enough traction to gain a consistent market share or will the activity continue to be focused on short-end products?

It’s been a very rare occurrence when €STR Adoption has topped AONIA adoption. Will we see a reversal in 2023 at all?