PRE-SEF Era

Let’s all think back to September of 2009, when the G20 gathered and proclaimed that:

“All standardised OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties…”

At that time, I was in knee deep in the design stages for the business architecture of Rates and Credit clearing in Japan. I remember thinking this G20 stuff was great, as it would give me job security for another 10 years, in 20 countries around the globe.

The clearing aspect didn’t frighten me, given that the LCH had a central clearing model that was working well (albeit only for dealers). What I found amusing was the notion of trading OTC derivatives on “exchanges or electronic trading platforms”. After all, I had spent months figuring out “simple” things like how to integrate the Markitwire affirmation platform into a Japanese clearing framework. We would spend significantly more time on the harder things; months would go by debating a single nuance of Margin calculations. Guarantee fund calculations, default management, even things like client statements would take weeks to agree. Let’s not even get into “super-clearing” (CCP interoperability).

And now the entire market was expected to figure out how to move a voice and relationship business onto an electronic exchange?

Keeping that in mind, now complete the actual G20 proclamation:

“All standardised OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties… by end-2012 at the latest”.

End of 2012!? Not only was I assured job security, but I might be a bit busy.

WHAT BECAME OF 2012?

We all know the punch line. 2012 Came and Went.

SEF’s COME OF AGE

These electronic platforms were given a name long ago – “Swap Execution Facilities”, aka SEF’s.

The CFTC, to their credit, despite lacking sufficient financial budget, have navigated a path that should give rise to an electronic OTC market in just a few months from now. The SEF rules are written and are in the registrar. Everyone can stop complaining about block trades. All we have to do now is worry about things like how a client’s credit line will show up at a SEF, as well as what a seemingly small 15 second delay might mean to the price of an OTC derivative.

The SEF’s themselves, however, are a bit busy. Just today I read about Tullet Prebon filing their SEF application. You would think they have some work on their plate.

WHO ARE THE SEFs?

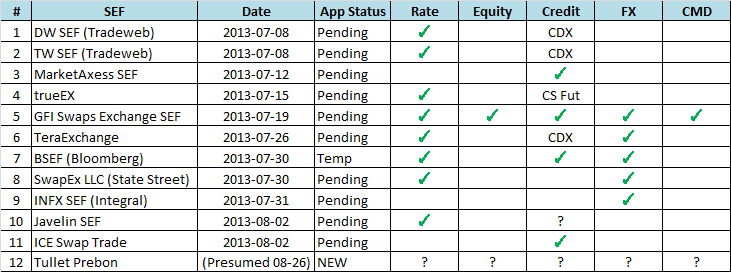

I like to reference the industry filings on the CFTC website. I have consolidated this into my own table to help get a grasp on who is offering what:

I’ve sorted the table by the CFTC “date”. According to this, Tradeweb (both DWSEF & TWSEF) has the earliest activity. However when you read the actual filings that are made publicly available, Tradeweb filed on July 3 whereas Bloomberg appear to have beaten everyone to the game with a filing of June 4. I suspect the “date” column reflects when their application status upgraded from pending to temporary.

HOW DO THE SEF’s DIFFER?

The Rates space seems crowded. I will be interested to see how the SEF’s differentiate their business to earn customers.

I find the Credit space interesting as well. In particular, some SEF’s have been clear that they will be only handling index products. Others are more vague, and some are clear that they will handle both index and single name. And then you have trueEX, who are pushing a potential game changer with S&P indexed credit futures.

You’ll also note some question marks (“?”) on there. In the press, I am led to believe that Javelin will be providing Credit services, however I can’t readily find it in the CFTC filings. (Reading and searching through the CFTC filings is deserving of another blog entirely). And then you have Tullet Prebon, who came out yesterday with news of their filing. Here, I have gone by only what I see in the press release, in that they intend to offer the full suite of products. That news is too hot off the press to even make the CFTC website as of going to press here.

I’m also a bit surprised that the list is only 11 names deep (12 in my list when you include Tullet Prebon). I know I have read press about names like ICAP launching a SEF. And where is BGC & Tradition? All of these names must be up to something. Perhaps they are just fashionably late to the party.

Lastly, any check-mark in the Equity column should probably be taken with a grain of salt. Who really knows where that is headed?

Alas, here we are, past the 2012 deadline, but the game is on, and as interesting as ever.