Last week I looked at Swap Volumes in October 2020 and focused primarily on SOFR Swaps and Futures at Clearing Houses, so this week I am going to look at Swap Execution Facilities (SEFs).

D2D SEFs

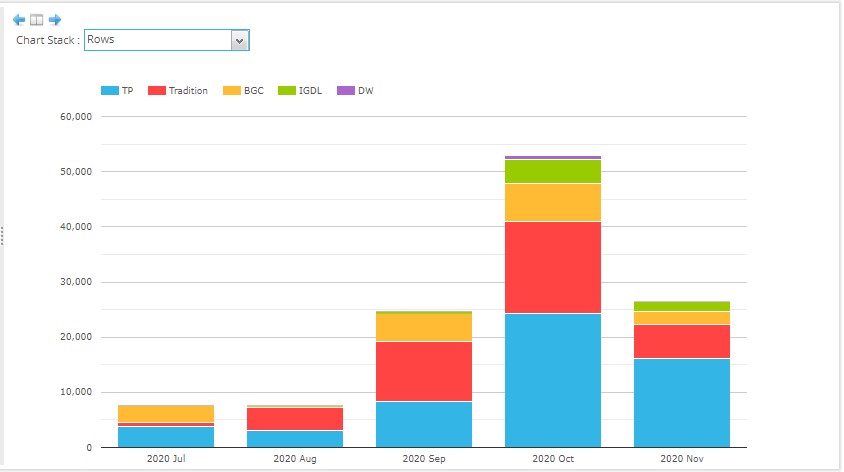

Let’s start by using SEFView to look at D2D SEFs, where the main product is SOFR v FedFunds Basis Swaps.

- Showing monthly volume up to November 16, 2020

- July and August each with $7.5 billion gross notional

- A jump to $24.7 billion in September

- A high of $53 billion in October, the month of CCP SOFR Auctions

- November with $26.5b up to the 16th inclusive, likely to get close to but remain below October volumes

- Tullets with the highest gross notional of $55.5 billion over the period

- Tradition next with $38.7 billion

- BGC with $17.8 billion

- IGDL (ICAP) with $6.6 billion,

- Dealerweb $770 million

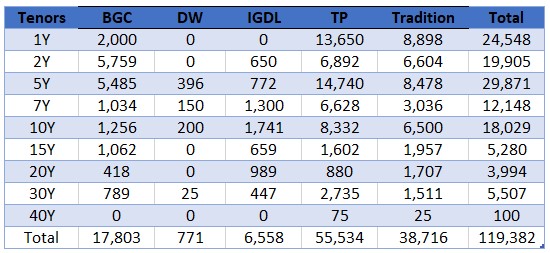

As not all gross notional volume is equal given the larger size and lower risk of shorter maturity trades, let’s look at the above volume not by month but by tenor.

- Showing Tullets the highest in every tenor up to 10Y, also in 30Y and 2 trades in 40Y

- Tradition highest in 15Y and 20Y

- The 2Y to 5Y bucket with the largest notional of $29.8 billion

- While 7Y to 10Y bucket has $18 billion

D2C SEFs

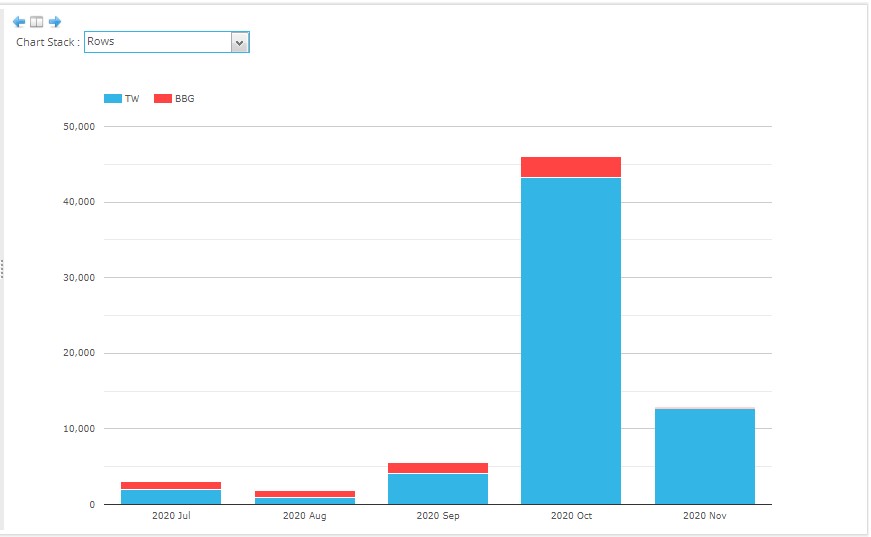

For D2C SEFs, the main product is SOFR v Fixed OIS Swaps.

- Again October by far the highest month with $46 billion

- Tradeweb with a cumulative $69 billion over the period up to 16th Nov

- Bloomberg with $6 billion

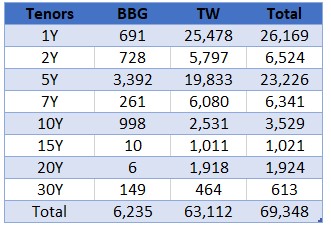

And the same volume but by tenor bucket.

The 1Y and 5Y bucket standing out with $26 billion and $23 billion respectively.

In addition not shown above is the fact that Bloomberg has also reported $520 million in Basis Swaps, mostly SOFR vs FedFunds but also SOFR v Libor 3M.

SEFs and CCP Volume

So in October 2020, SEFs reported:

- $53 billion of Basis Swaps at D2D SEFs

- $46 billion of OIS Swaps at D2C SEFs

- $0.5 billion of OIS Swaps at D2C SEFs

A grand total of $99.5 billion, lets call it a round $100 billion.

This compares to the $412 billion gross notional reported in October by the Clearing House, LCH SwapClear and CME.

Meaning that 24% of the cleared global SOFR volume of $412 billion in October 2020 was transaction on SEF venues.

That’s It

That’s all I have time for today.

It will be interesting to see where November volume ends up.

Will SEFs get a similar 24% share of global cleared volumes?

And will we see a change in SEF market share?

Or will it remain the same.

Only time will tell.