More than 10 years after the fall of Lehman Brothers, and with limited changes for several years you might be forgiven for the impression the CFTC is done with SEF regulation. Not so.

With a full complement of commissioners recently approved, CFTC has started the Dodd-Frank Title VII re-regulation ball rolling. CFTC has published proposed rules for comment by February 13th which appear to substantial revamp SEF regulations.

This is the first chunk of CFTC Chairman Giancarlo’s game plan outlined in 2018 in several speeches and two white papers which I call for short Title VII 2.0 and Title VII 2.0 “Cross-border Edition”.

Here I take a look at the proposed SEF rules and request for comment which are out for public comment by February 13th and January 31st.

The rules

The proposed SEF rule-making has public comments due Feb 13. The request for comment on post-trade name give-up has public comments due Jan 31.

At 204 pages, the SEF rule-making is quite heavy going. There is a speed-read:

- the Skadden summary – a one-page summary of both

- pages 39-57 of Title VII 2.0 in Chairman Giancarlo’s own words

- Commissioner Berkowitz’s dissent puts the other side of the argument

From the minutes, the proposals passed 4-1 the November public meeting of the five commissioners. Commissioner Berkowitz dissented and Commissioner Benham’s approval made clear he would dissent if this were a final rule.

Commissioner Berkowitz’s dissent advocates for abolition of post-trade name give-up for cleared trades. It is argued that, since there is no ongoing counterparty relationship once the trade is cleared, there is no need for a dealer to know who they traded with – like a futures exchange trade. As this is a request for comment not a proposed rule, I limit the remainder of this post to the SEF rule-making.

So far there are no public comments on the substance of the rules posted. Despite this, private dialogue must be intense. We might usually expect trade associations (e.g. ISDA, FIA, SIFMA) to publicly comment – jointly or separately. Maybe some individual entities too. I also wonder whether we’re in for an extension of the date (as happened on other major rule-making).

Watch the comments pages.

Meanwhile, I summarise the proposal, the proponents’ hopes and the antagonists’ fears as simply as I can.

The gist

In summary the proposal is to expand SEF scope (a lot) on five main fronts:

- More SEF Registrants: newly including interdealer brokers (IDBs) and single dealer platform aggregators (SDPAs) as forms of SEF (even if their trades are not SEF-mandated)

- More SEF Execution Protocols: newly including voice broking and RFQ1 (a single quote response is required to close a deal); permitting any other protocol a SEF might invent; removing the order-driven CLOB mandate and the quote-driven limitation to RFQ3

- More Permissive SEF rules: newly permitting SEFs to be limited to “similarly situated participants” (meaning e.g. SEFs can be D2D only if they so wish); streamlining some of the SEF compliance rules

- More SEF Mandated products: newly including non-MAT clearing-mandated trades; abolishing the MAT process for mandating products for SEF trading (which hasn’t seen any applications for several years)

- Abolition of Pre-arranged Trading / Pre-execution Communication: removing temporary exemptions for such activities either means in the new SEF world these communications are no longer needed or get handled on SEF (e.g. in the voice brokerage or RFQ1 protocol)

Potential impacts

I lay out the intended benefits and italicize the feared downsides alongside.

- SEF meaning change. “SEF” now just means “CFTC registered multilateral venue” as opposed to the specific CLOB/RFQ3 only formulation today.

- Dozens of newly registered SEFs drives innovation to the good of liquidity. CFTC indicates it expects 40-60 new registrants among which 1 is an SDPA so the rest are either IDBs or ECNs (many supposedly affiliates of existing SEFs). There is no data to demonstrate this will improve liquidity.

- Commercial demand will drive protocol usage. Some of the tighter pricing resulting from RFQ3 will be lost in the shift to RFQ1 / voice / less pre-trade transparency.

- There is a de facto D2C vs D2D SEF split under current regulations. The dealer oligarchy will be further empowered against buy-side interest.

- 28% of total US volume is off-SEF cleared – some of this will move onto SEFs. How much is covered in the next section.

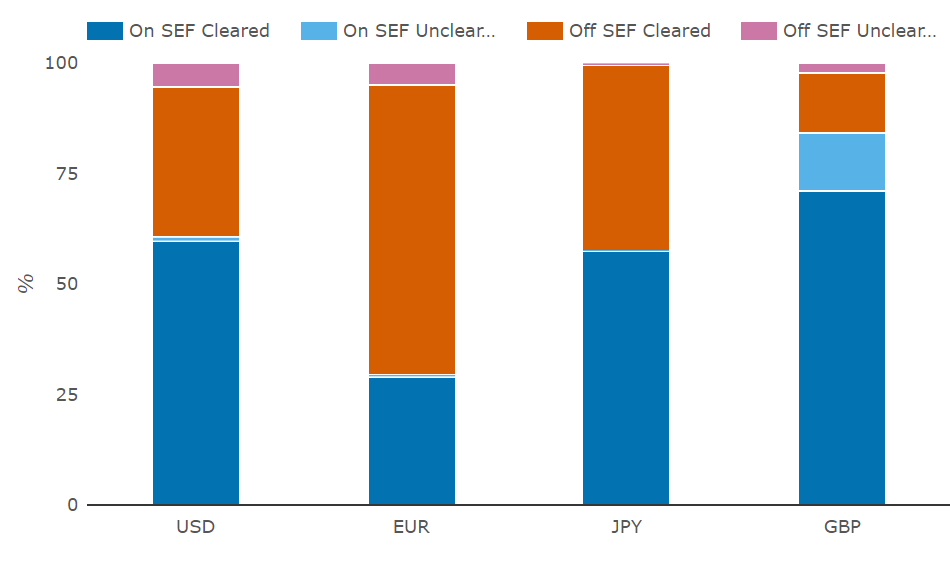

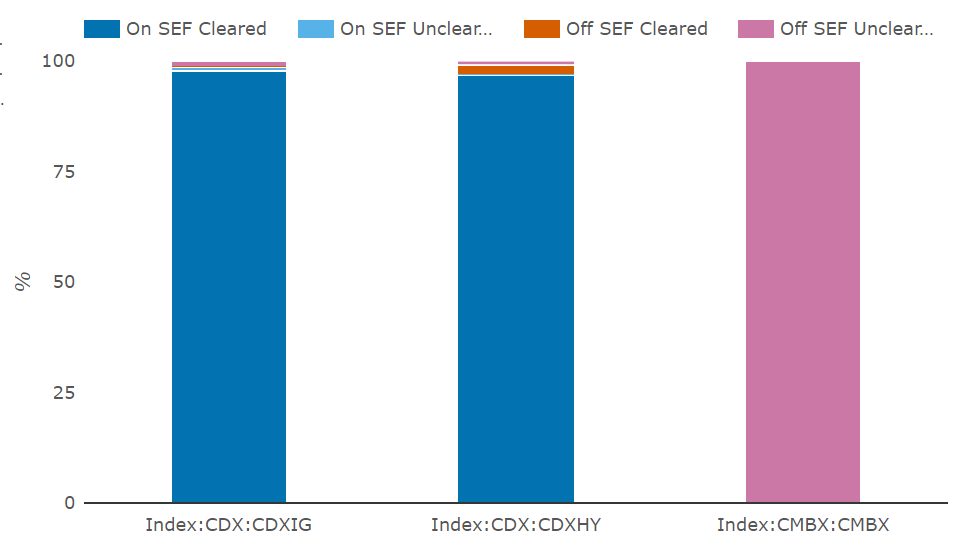

Will more cleared trades move onto SEFs?

CFTC figures suggest that up to 28% of the total US volume is cleared but off SEF and the hope is a large chunk of this is clearing mandated and moves from off SEF to on SEF.

A glance at the SDRView dashboards below (for Jan 11) shows quite a bit of cleared IRD off SEF but not much cleared CRD off SEF. This suggests the biggest shift of volume on SEF would be in Rates.

Two subtler points are worth noting:

- clearing-mandated trades (newly SEF-mandated) are a subset of all cleared trades and

- even if product is clearing-mandated other exemptions may apply.

So we need to dig deeper to figure out the impact here but it could be quite large.

In summary, it depends.

What Title VII 2.0 aspects are not yet in draft rules?

Title VII 2.0 also covers areas in the CFTC’s direct purview beyond SEFs including Swaps Central Counterparties (CCPs) (pp. 7-23 which focuses on default management, default waterfall resources, recovery and resolution) and Trade Reporting Rules (pp. 24-38 which notes that a future reporting solution should be “specific, accurate and useful enough to capture systemic risk”). No specific proposals are made and it is not clear whether there is any urgency here – particularly given the Chairmanship is due to change in 2019.

The remainder of the paper discusses Swap Dealer Capital (pp. 58-70) and End User Exemption (from uncleared margin rules) (pp. 71-88). For both of these the CFTC is part of a consensus across a large US and global group of regulators including both prudential and markets regulators. It seems unlikely that the CFTC would unilaterally change things here.

One aspect not covered in the Chairman’s publications and speeches is an unintended consequence of the clearing mandate and the uncleared margin rules together. Bluntly, the clearing mandate inhibits reduction of bilateral risk. I will post soon on this.

Title VII 2.0 Cross-Border Edition is not covered here but if turned into rule-making might go a long way to the long-standing cross-border issue reflected in a trail of exemptive relief and no-action letters. I will post on this soon.

In Summary

- SEF rules are out for comment by Feb 15th

- The aim is a dramatic expansion and simplification of regulation of the US SEF market liberating commercial forces to make markets more liquid and price efficient

- Up to 60 new SEFs might register

- Up to 28% of total US swap trade volume might move from off to on SEF

- Skeptics suggest this is a name change only, transparency and tighter pricing benefits may be lost and the dealer oligarchy will be further empowered

- We should watch the public comments to see how this one shapes up.

Bibliography / Links

First white paper Title VII 2.0: Swaps Regulation Version 2.0 – An Assessment of the Current Implementation of Reform and Proposals for Next Steps (Jul 2018)

Chairman Giancarlo’s speech at the London Guildhall (Sep 2018)

Second white paper Title VII 2.0 “Cross-border” Edition: CROSS-BORDER SWAPS REGULATION VERSION 2.0 – A Risk-Based Approach with Deference to Comparable Non-U.S. Regulation (Oct 2018)

The minutes of the CFTC open meeting (Nov 2018) which approved publication

Commissioner Berkowitz’s dissent (5 Nov 2018)

Commissioner Benham’s concurrence (5 Nov 2018)

The SEF rules – 17 CFR Parts 9, 36, 37, 38, 39, and 43 Swap Execution Facilities and Trade Execution Requirement with public comments due Feb 13

The request for comment on post-trade name give-up – Post-Trade Name Give-Up on Swap Execution Facilities with public comments due Jan 31

The Skadden summary: cftc proposes swap execution facility rule (Nov 2018)