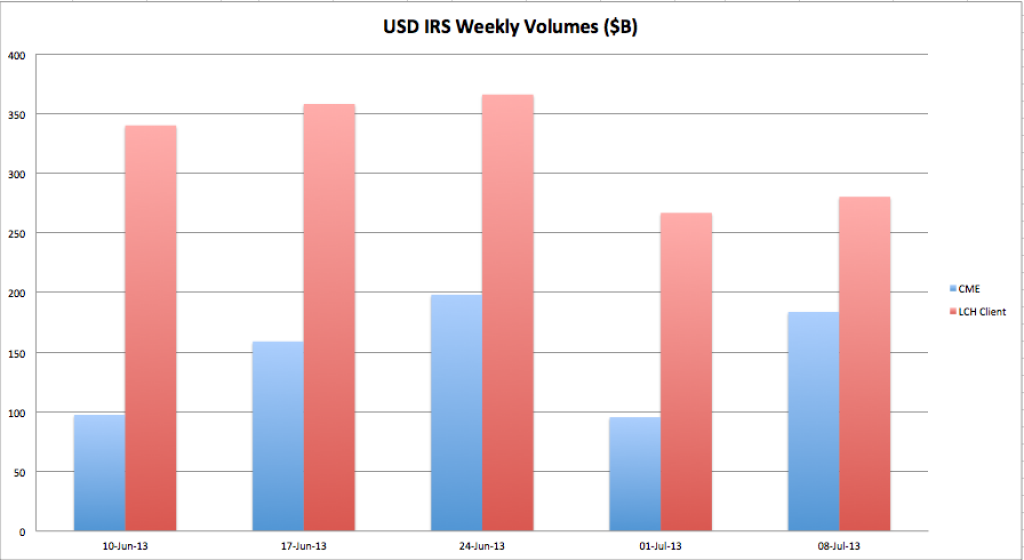

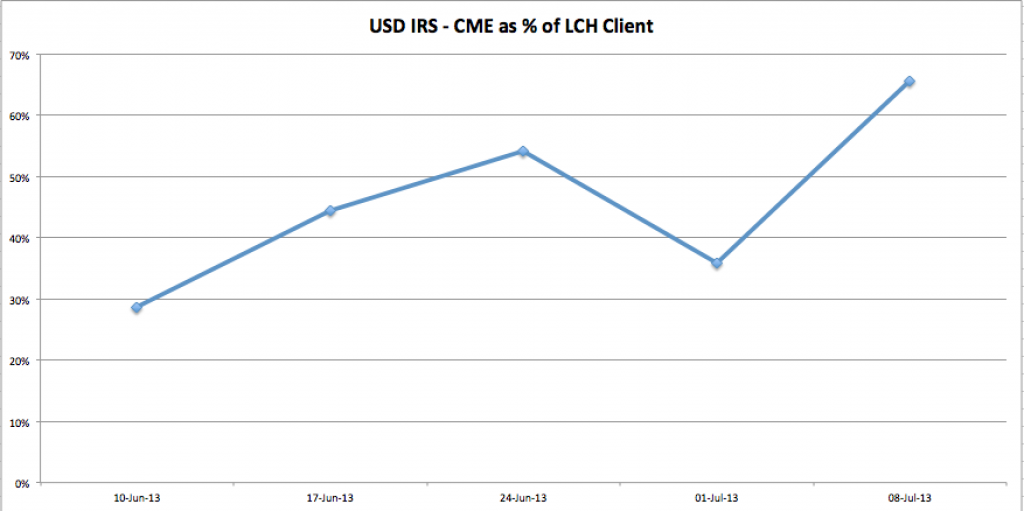

Following on from my article of June 25th, Mandatory Clearing, June 10, Week Two and CME or LCH, I wanted to update the figures with more recent data.

So focusing only on USD IRSwaps and having taken the daily figures from CME and LCH websites, I created weekly volume figures, which are shown in the charts below.

From these we can observe that over the five week period post June 10:

- CME volumes have risen from 30% of LCH Client volumes to 66% of LCH Client volumes.

- So from one third to two third.

- The week starting 1-July, has the 4-July US holiday, so this week is best ignored in terms of trend.

- The increase in CME volumes is not coming from a commensurate decrease in LCH Client volumes.

- (LCH Client volume as a percentage of LCH All has remained at 20% over the period, not in chart).

This suggests that CME has gained more client clearing volumes from the June 10 mandatory deadline than LCH. The recently launched LCH Swapclear US-Domiciled LLC, does not yet appear to have meaningful volume, see here for the figures.

It will be interesting to see how these volumes develop in the coming weeks.

Not least because as my recent article on the LCH Swapclear margin details, the LCH move to a higher initial margin (improved defaulter pays) and lower guarantee fund contribution (members pay) ,is likely to mean that Clients will face lower initial margin requirements from CME than LCH.

Particularly from October 2013, when the Sep 2008 scenarios (Lehmans bankruptcy) fall out of the 5 year look-back window used by CME.

It will be interesting to see the volumes in the 4Q 2013.