- Every month, over 500 USD swaps are reported to SDRs that match MAT criteria but are executed off-SEF.

- This has been a persistent phenomenon of the data for as long as I can remember.

- The swaps are below block size, but still account for $25m+ of DV01 each month ($50bn+ in notional).

- This has persisted through RFR transition and with the latest MAT filing in 2023.

- Trades that are potentially exempt from the MAT rule include:

- Transactions by counterparties who are exempt from the clearing requirement (“end-users”).

- Inter-affiliate trades.

What is a MAT trade?

A MAT filing, or “Made Available to Trade” determination, is when a trading venue (SEF) submits a proposal to the CFTC stating that they deem certain swaps to be liquid enough to have an execution mandate applied to them.

Basically, a SEF says “I think these swaps should only be traded on SEFs in the future”. Assuming the CFTC then agrees with the SEF, you are then required to trade a “MAT” swap on a SEF.

There have been two MAT determinations – one when SEF trading was in its infancy, and the second as a result of RFR transition in 2023. The following USD swaps are currently required to be traded on a SEF:

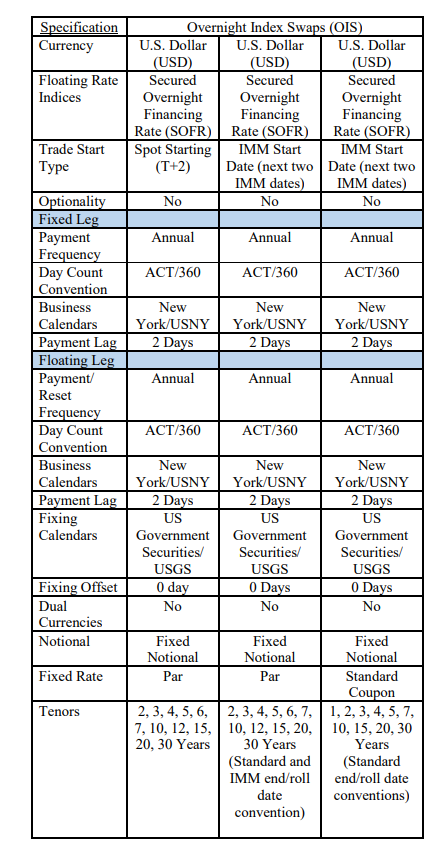

How much of the market is MAT?

MAT trades make up 75% of the spot-starting market in USD swaps:

Showing;

- LIBOR-based swaps were the only MAT swaps until they were joined by the same set of SOFR-based swaps in August 2023.

- The transition from LIBOR-based trading to SOFR trading caused the move from MAT to non-MAT trading during 2022 – there is nothing nefarious happening here!

- The proportion of spot-starting swaps that are MAT is remarkably stable month-on-month at 75%.

As I explored here, readers should bear in mind that spot-starting swaps account for ~50% of total USD swaps activity. This means that across the whole market, MAT swaps account for about 35-40% of activity:

As a rough rule of thumb, MAT swaps account for the majority of trading in the interdealer (D2D) market. A swap is still subject to the execution requirement even when traded as part of a package, such as a Spreadover. As Amir has explored, Spreadovers make up the majority of IDB business.

Customer (D2C) trades are not so standardised and hence are not captured as frequently by the execution requirement. A lot of on-SEF execution in the D2C space is therefore volountary (for a number of reasons that Tradeweb and Bloomberg will be more than happy to tell you about!).

Materiality

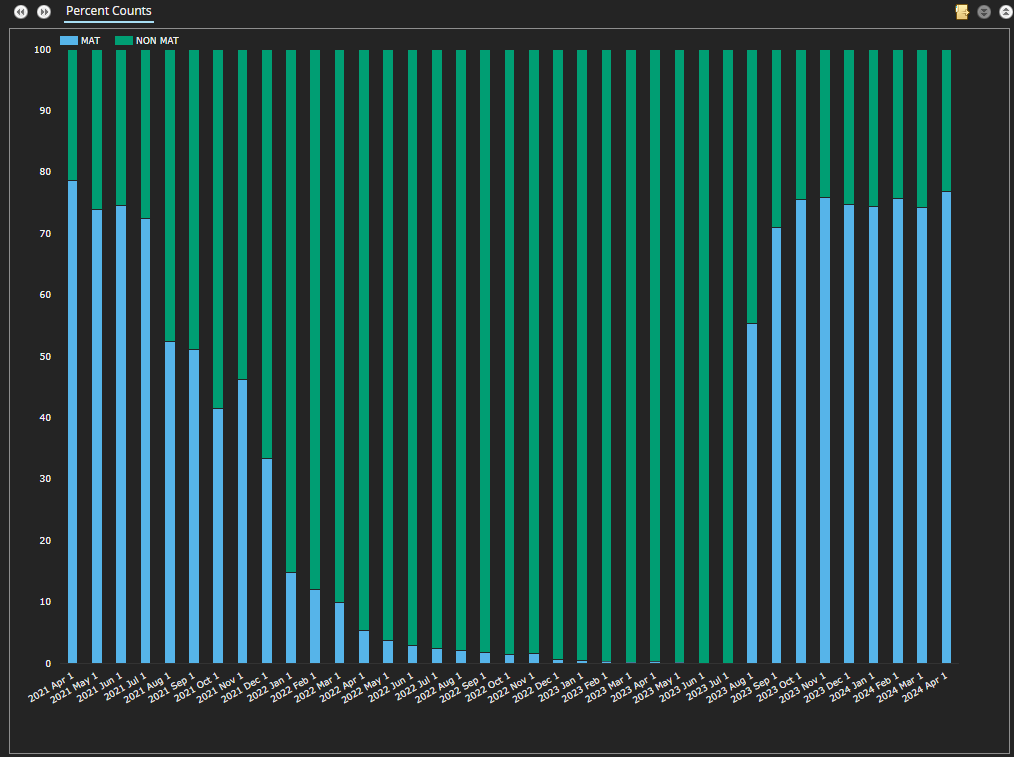

The chart above shows it is common for over 60,000 USD swaps to trade per month. There are about 500 MAT swaps reported off-SEF each month – less than 1% of all USD swaps. Should we care? Yes and no:

- In terms of market participants using the SDR data, these trades should be excluded when trying to identify price-forming transactions only.

- In terms of the Clarus data product, these trades act as a “quality control”. These MAT, off-SEF trades should always represent a very small portion of the market. Any spikes in numbers should lead to a re-assessment of our data augmentation.

- Due to the limited circumstances under which a MAT trade can actually trade off-SEF, we can use this knowledge to track how much of the market is related to inter-affiliate trading and/or by market participants invoking their end-user exemption.

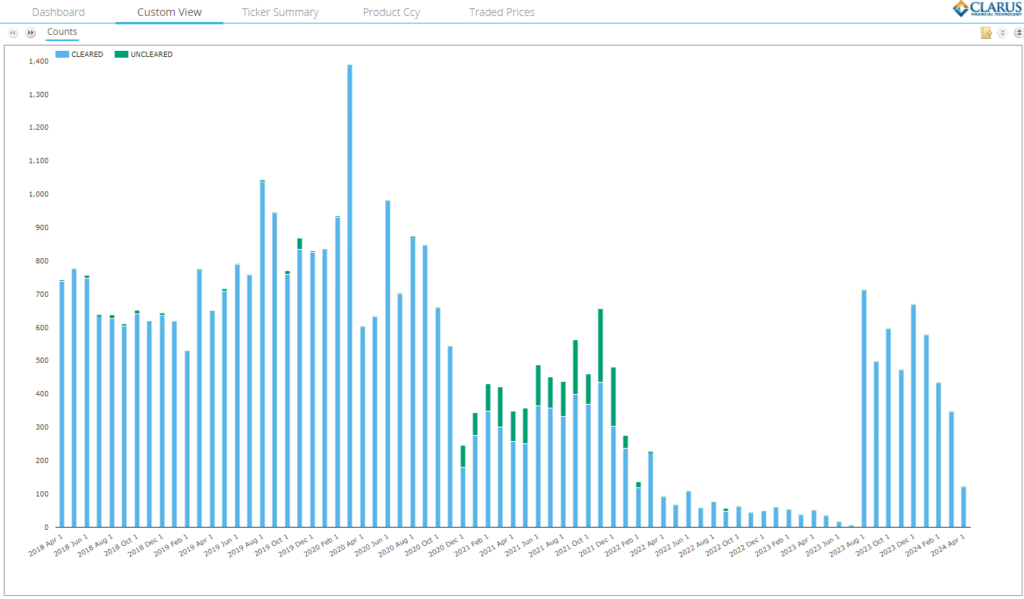

MAT but off-SEF

So, how many MAT trades are executed off-SEF each month? It is surprisingly consistent month-on-month:

Showing;

- Monthly trade counts for the past five years of USD swaps that match the MAT criteria (IRS until August 2023 and subsequently including OIS) that are executed off-SEF.

- Before transition to SOFR, we saw a few hundred MAT trades per month traded off-SEF. This exceeded 1,000 trades in a couple of months.

- In August 2023 we saw 700 MAT swaps executed off-SEF.

- This has continued at a rate of about 500 per month since the latest MAT determination.

The CFTC’s Final Rule concerning “Exemptions From Swap Trade Execution Requirement” was published in February 2021. According to this text, there are only two exemptions allowed:

- If a MAT trade is inter-affiliate – i.e. an internal trade between two entities that are owned by the same group.

- If a MAT swap is executed by an “end-user” who is exempt from the Clearing Mandate.

And here is the kicker….

Reading those two exemptions, I assumed these trades would be largely uncleared. Why?

- An internal inter-affiliate trade would have to post TWO lots of Initial Margin, on the Pay and Receive legs.

- If an end-user is exerting their exemption from the Clearing Mandate to trade off-SEF, I assume they are also keeping the actual trade uncleared as well.

Well, it would be a pretty boring blog if I now showed you a chart showing that all of these trades are indeed Uncleared. So here is the puzzle – the trades are mainly reported as Cleared. In fact, there hasn’t been a single Uncleared MAT swap traded off-SEF so far in 2024:

Conclusions

My working assumptions:

- The handful of uncleared trades are the end-user trades. There are precious few of them because end-users rarely trade spot-starting structures.

- The cleared trades are largely inter-affiliate. My guess is these are “optimisation” type of trades, whereby banking groups have more than one affiliate as a member at a CCP. They actively move risk between affiliates to bring down their total IM burden.

Yet again, it strikes me how unpredictable the interplay of regulation and data is. You really have to dig into the weeds to make sense of the data. It ends up being surprisingly complicated to make sense of what is essentially very simple data!