We’ve received many comments and citations around the data we presented at the CFTC TAC meeting in June. Nearly all of the comments are positive, but as with any data, many wanted to confirm their understanding of the data presented.

In particular, people took note of the 72.8% of swaps dealt in June being forward start. It should first be acknowledged that it was 72.8% of Off-Facility swaps were forward-start in May, but even that can be interpreted as quite alarming.

I wanted to take the time to dig into the data further, explain what the metrics mean, and then provide some updates through the month of June.

WHATS “MAT” AGAIN

As usual, it’s helpful to remind ourselves what products have been made “Made-Available-To-Trade” or “MAT” for short. After all, it is only MAT products that are required to be traded on-SEF. Everything else is simply “permitted”. The CFTC site here is still a valid resource. Generally speaking, if your interest rate swap is USD denominated and meets the following rules, it is MAT:

- Fixed vs Float

- Floating index is 3M or 6M Libor

- Swap start date is either:

- Spot (T+2)

- Either of the next 2 IMM dates

- No optionality exists

- Fixed leg is either Annual or Semi-Annual, and is either 30/360 or Act/360

- Floating leg resets quarterly (for 3M Libor) or semi-annually (for 3M or 6M Libor), and accrues Actual/360

- Has a fixed notional (not amortizing/accreting)

- Fixed rate is a par coupon, or for MAC contracts, is a standard / “market agreed coupon”

- Tenor is 2, 3, 4, 5, 6, 7, 10, 12, 15, 20, or 30 years

- Trade size is under the block threshold (Block trades are not required to be traded on-facility)

- Neither party to the trade can declare an end-user exemption

- It is a clearable transaction (I actually can’t say for sure if this is written in the rules or just implied because the clearing mandate is broader than the MAT rules)

Of course, there are somewhat similar rules for EUR and GBP, as well as other peculiarities and specifics that need to be met, but let’s try not to get too “Inside Baseball”.

THE DATA I PRESENTED IN JUNE

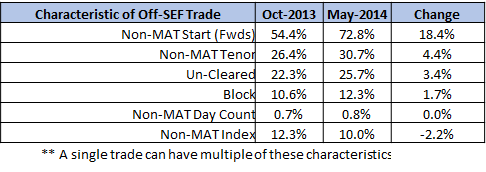

At the TAC meeting, I presented the following table, which showed that among the population of trades dealt Off-SEF, the percent of trades that had “Non-MAT Start” dates increased from 54.4% in October 2013 to 72.8% in May 2014. This is still correct. In my verbal commentary I was clear that we need to be careful here, as the denominator (the number of Off-SEF trades) would have decreased, so we may not want to make much of it. The intent with much of my commentary was not to raise alarm bells, but rather to make the point that this is the OTC market, and you’re simply not going to get 100% adoption unless you MAT the entire curve, along with all the peculiarities of OTC swaps.

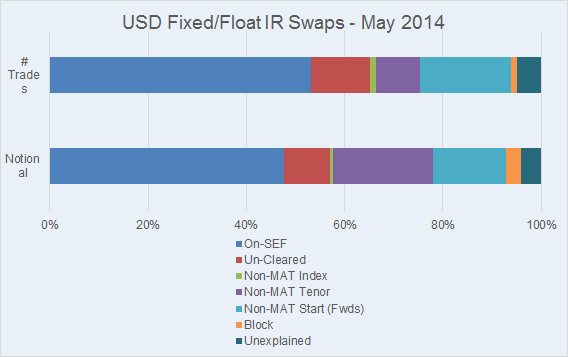

I also presented a chart, which looked at the population of USD swaps, and attempted to characterize what was Off-SEF. The table, shown below, shows over 50% of the swaps, by trade count, were On-SEF (the large blue bar), then the Off-SEF comprised of Un-Cleared, trades that were not 3M or 6M Libor (Non-MAT Index), were not a MAT-tenor, etc, etc. The large light blue segment were forward-starting.

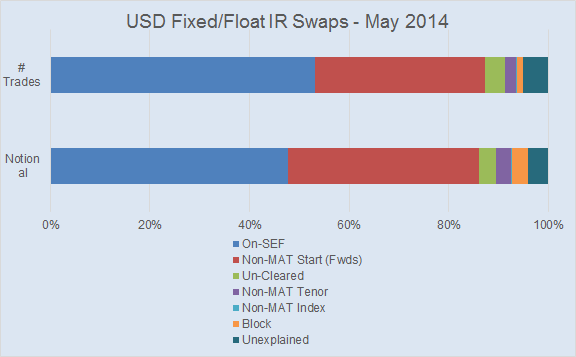

However I also presented the same data in a separate chart. I described this as “peeling the onion” differently. If you acknowledge that many of Off-SEF trades exhibit more than one non-MAT characteristic, the order in which you analyze the data matters. For example, if all of the Off-SEF trades were block trades, the chart would be pretty dull if I first examined block trades – as the entire population would be block. However if I “peeled the onion” differently, looking at un-cleared, fwd-start, 1M Libor, etc first, there might not be any trades that were Off-SEF solely because they were block sized.

Hence in the following chart, I first peeled back the trades that had a “Non-MAT Start”. The results are of course quite different.

SO LETS MAKE SENSE OF THIS

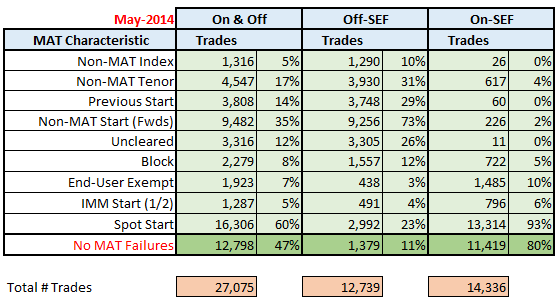

The table below looks at characteristics of the population of USD IRS in May 2014.

This tells us there were 27,075 USD Fixed/Float swaps in May, of which 12,739 were Off-SEF. Importantly, you cannot add up the columns, as each row is not necessarily exclusive, but rather is a simple count of the number of trades with that characteristic. For example, you can have a single trade be block, non-MAT tenor, non-MAT start, and non-MAT Index (imagine a 1bn USD, 9 year, 10-day fwd starting, 1M Libor trade, which would show up in multiple lines).

Some characteristics, however, are exclusive. In particular:

- Non-MAT Start (Fwds)

- IMM Start (1/2)

- Spot Start

If you add these three up, they will always describe the entire population. In other words, if it is not spot-start and not a first-two IMM start, it is a Non-MAT Start. What this also means is that any trades with start dates in the past (Previous Start) are characterized as Forward-Start.

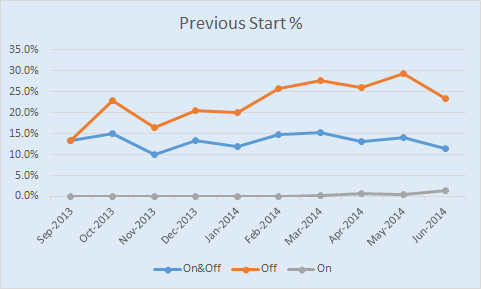

These Previous Start trades seem to be significant. 14% of the total trade activity in May has a start date prior to the execution date.

BACK TO THE FUTURE?

So what is a “Previous Start” swap? These trades have been reported since the inception of SDR reporting, and often we would chalk them up to:

- trades being reported late

- underlying swaps from exercised swaptions

- or just bad data

However with the flurry of PTC activity on SEFs (as Amir discussed in his blog), it’s become clear that all of the new offsets to legacy trades that are generated by the compression/compaction process is responsible for a decent chunk of these trades. Of course, each trade has an implied fee associated with it, however often times only one trade in the bundle will get a fee to account for the entirety of the compression.

Either way, “Previous Start” is a significant number.

Hence if you want to know how many trades are fwd-start, with that start date in the future (not spot or IMM), you need to subtract “Previous Start” from “Non-MAT Start (Fwds)”.

Clear as mud? Good. Let’s move on.

GOT IT. NOW SHOW ME SOME COOL TREND CHARTS

So the question would be, is there any notable trends in this or other OTC swap behavior?

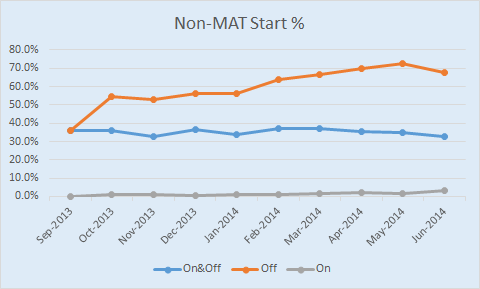

Let’s first observe the percentage of trades that are not MAT-start (this will include anything not spot or first two IMM). Here you will find the 73% number for May Off-SEF. Note that for the entire population, this number hovers between 30 and 40%.

And if we look at the amount of trades with Previous Start Dates, this too seems to hover in a range since SEF inception:

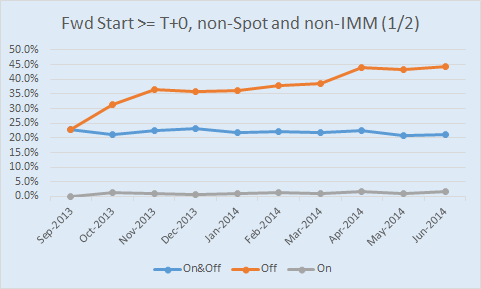

Truly forward start (starting today or later, but not spot or first two IMM dates):

Important to again draw your attention to the total population (blue line) as this shows a narrow band.

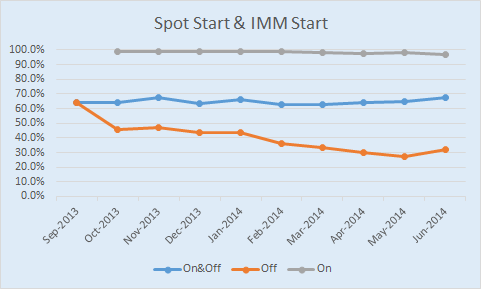

Finally, let’s look at Spot Starting and IMM Starting swaps (this is the inversion of the first table in this section). These are of course what has ultimately been deemed MAT start dates (the MAT designations were defined, and also took effect during this timeframe). When looking at the entire population (On+Off SEF), the number of MAT-able start dates hovers between 60 and 70%.

SUMMARY

Hopefully the market’s behavior, when it comes to forward starting swaps, is now clear. Generally speaking the market traded these before, and still does, with no notable change in behavior.

Given that only 60-70% of all trades are spot or IMM start, there would seem to be a firm cap on how much of the universe of swaps that could possibly be MAT-able and hence traded On-SEF. And we didn’t even look at some of the other characteristics such as how many of the trades are 1M Libor, or block, or uncleared. You can wait for me to do another installment, or do that for yourself on SDRView.