The BCBS published a Consultative document in March 2018 with the title ‘Revisions to the minimum capital requirements for market risk” and in this article I look at the details.

Background

In January 2016, the BCBS published the standard Minimum capital requirements for market risk ( “January 2016 standard”), designed to address a number of structural shortcomings in the Basel II market risk framework and a key reform of global regulatory standards in response to the global financial crisis.

The implementation and regulatory reporting date of the January 2016 standard is now 1 January 2022.

The deferred implementation date allows banks additional time to develop the systems infrastructure needed to apply the standard and for the BCBS to address certain specific outstanding issues, some of which are n this March 2018 consultation. (The complete document is here).

From my earlier blog, FRTB – What You Need to Know, we know that firms have a choice between using a Standard Approach (SA) or an Internal Models Approach (IMA), so lets look at the proposed revisions to each of these.

Revisions to the Standardised Approach

Annex A of the March 2018 document lists the following:

The one that immediately stands out is that last one; revisions to risk weights. Recall that risk weights are the variances/volatilities of risk factors in the sensitivity-based method and as such are the key determinants of the size of the market risk capital requirement.

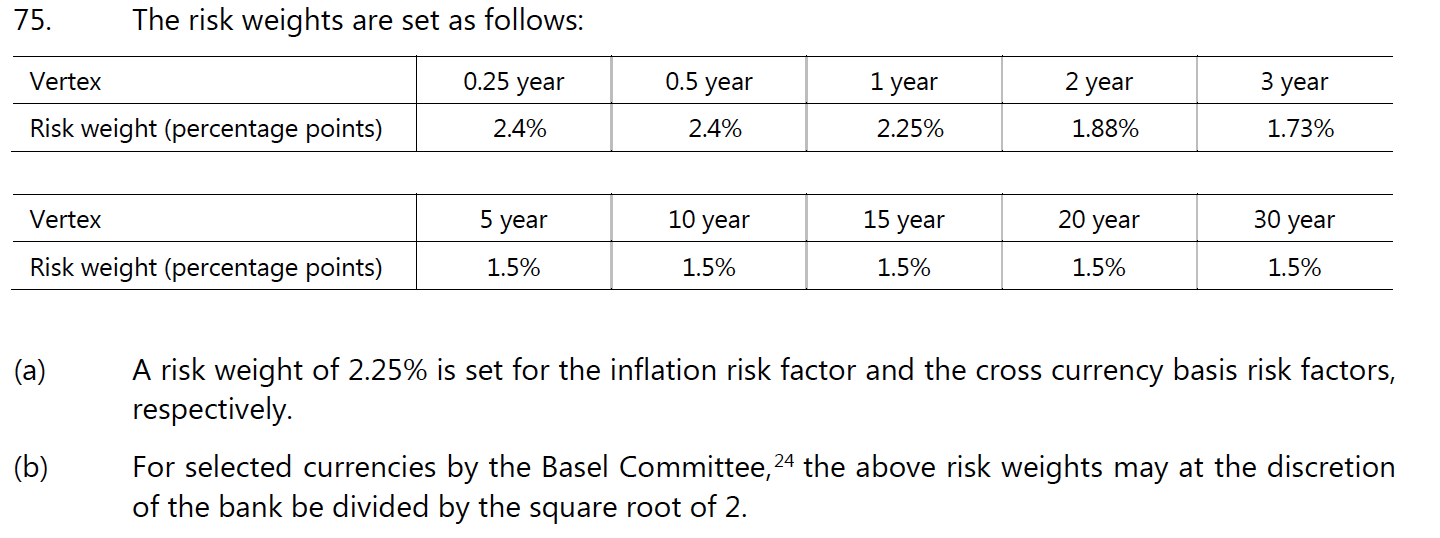

The BCBS notes that the risk weights as originally proposed in January 2016 need to be reduced to bring market risk capital requirements closer to the originally intended level and based on impact data received to date, the risk weights for the general interest rate risk class are to be reduced by 20–40%, and equity and FX risk classes by 25–50%. (While there are no revisions for the credit spread and commodity risk classes).

The final recalibration for all risk classes will be determined based on further analysis of impact data provided by banks, and feedback provided to this consultative document.

Comparison of risk weights – Jan 2016 to Mar 2018

Lets look at the detail of these, starting with the original January 2016 table for GIRR.

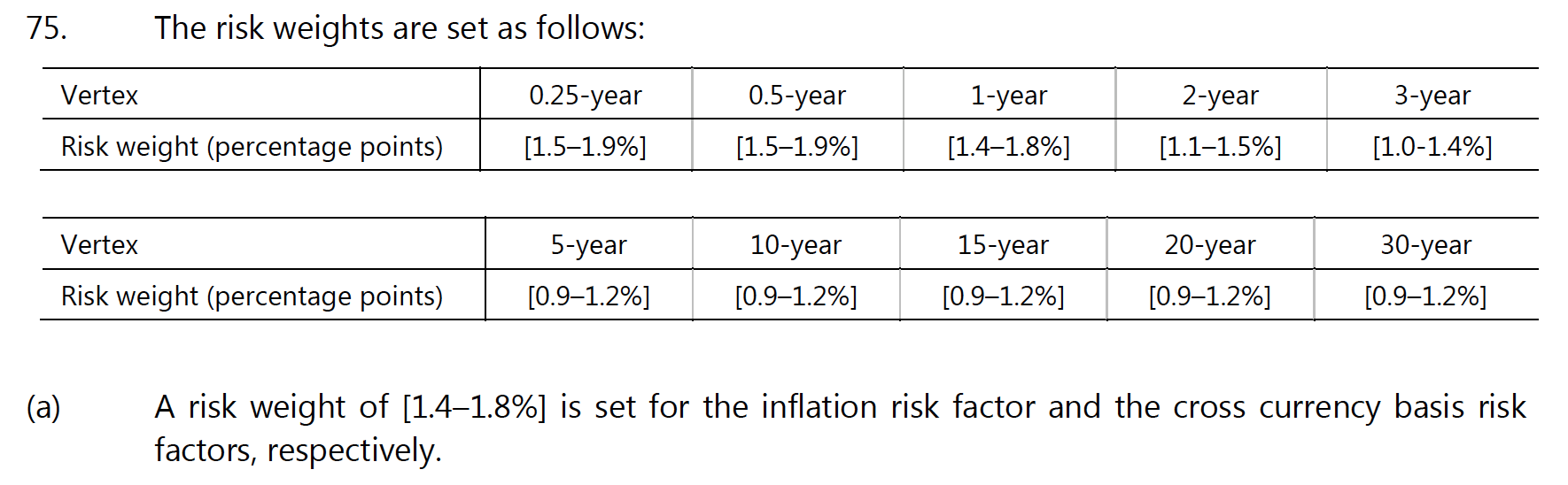

And then the new March 2018 table for GIRR.

So as an example the 10-year risk weight will drop from 1.5% to between 0.9% to 1.2%, a reduction of between 20% to 40% and more than the discretionary sqrt 2 (29%) previously available for selected currencies.

Inflation and Cross Currency Basis are reduced from 2.25% to between 1.4% – 1.8%.

FX sensitivities risk weight is reduced from 30% to between 15% – 22.5%.

The equity table is too large to reproduce here but has similar reductions to FX.

These revisions are a welcome reduction in the market risk capital charge and will serve to make the standardised approach more attractive to firms that were wavering between IMA and SA.

Revisions to the Internal Models Approach

Annex B of the March 2018 document lists the following:

P&L Attribution test

There has been much comment on the January 2016 P&L Attribution test and the difficulty of passing this as well as the consequence of failure meaning reverting immediately to the SA.

This revision completely revises the PLA test from one based on the mean difference between risk-theoretical P&L (RTPL) and hypothetical p&L (HPL) and the variance of the unexplained P&L divided by the variance of HPL.

The new test is to be conducted on a quarterly basis using a time series of data collected over the preceding 12 months and uses two new metrics:

- Spearman correlation between the values of HPL and RTPL

- A measure of the similarity of the distributions of HPL and RTPL using either a Kolmogorov-Smirnov (KS) test or a Chi-Squared test, for which BCBS seeks comments on the relative merits of one over the other

Based on the outcome of these metrics a trading desk is assigned to one of three zones:

- The green zone if the spearman correlation is > 0.825 and KS < 0.083 / Chi-squared < 14.

- The red zone if the spearman correlation is < 0.75 and KS > 0.095 / Chi-squared > 18.

- The amber zone if neither green or red

PLA test failure consequences

These three zones have been introduced to replace the automatic consequence of PLA test failure being to make a trading desk ineligible to use IMA.

Under the March 2018 revisions, trading desks in the green zone pass the PLA test, while those in the red zone fail the PLA test and must fall back to use SA.

However trading desks in the amber zone have not performed so poorly as to necessitate immediate fallback to SA, instead they are subject to an additional simple, formula-based capital requirement to be added to the trading desk’s IMA-based capital requirements.

This additional requirement is determined by the difference between IMA and standardised approach capital requirements as determined on an aggregated level for all trading desks in the green zone and the amber zone. This difference is adjusted by (i) a weighting factor that is determined by the materiality of the amber zone trading in relation to the combined set of green zone and amber zone trading desks; and (ii) a multiplier that sets the severity of the capital surcharge determined as a fixed multiplier of 50%.

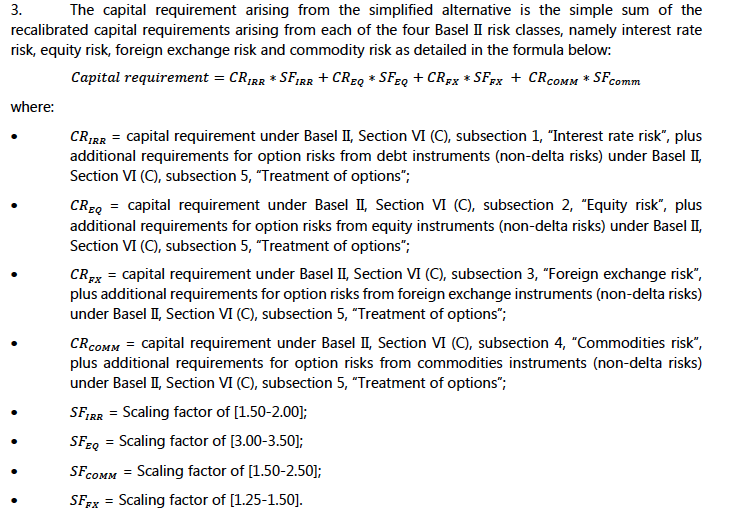

Simplified Alternative to SA

In June 2017, the BCBS published a consultation document to propose a simplified alternative to the standardised approach, which I covered here. In response to comments received the BCBS has decided that a recalibrated Basel II standardised approach would be better suited to facilitate the adoption of the standard by the banks for which a simplified alternative is intended.

This recalibration takes the form of multipliers to the capital requirements in each risk class with the final calibration of these multipliers to be determined.

The use of the simplified alternative is subject to supervisory approval and supervisors will consider the following indicative criteria:

- The bank should not be a G-SIB.

- The bank should not use the internal models approach for any of its trading desks.

- The bank should not hold any correlation trading positions.

Other Details

There is more detail in the BCBS March 2018 document on the above as well as topics I have not had time to cover:

- Non-modellable risk factors,

- Treatment of structural FX positions and

- Boundary between trading book and the banking book.

For those of you interested, please see here for the d436 document itself.

Thats it for today.