The BCBS recently published a Consultative document on a ‘Simplified alternative to the standardised approach to market risk capital requirements” and in this article I will look at the detail of this.

Standardised Approach (SA)

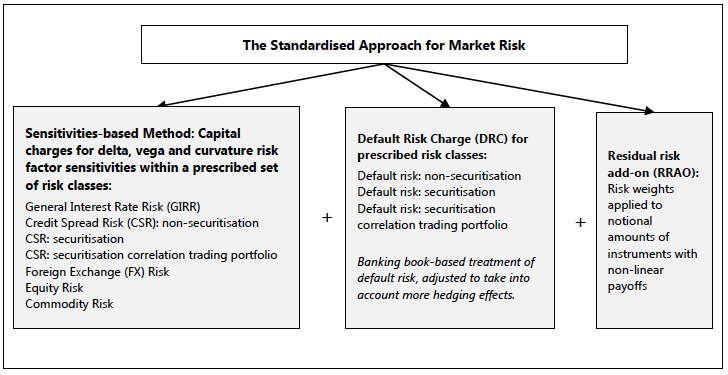

BIS provides the following diagram to summarise the Standardised Approach.

(For a re-cap of the SA see FRTB – What You Need to Know).

What is the proposal?

The main component of the Standardised Approach (SA) is the Sensitivities-based method (SbM) and the proposal is a simplified form of this method, while leaving the Default Risk Charge and Residual Risk AddOn as they are. The simplifications to the SbM are:

- Vega and Curvature charges are dropped

- (So just Delta charge remains)

- Basis risk calculation is simplified

- Less granular risk factors and correlation scenarios

As an alternative, the consultation also seeks feedback on whether retaining a re-calibrated version of the existing Basel II standardised approach to market risk would better serve the purpose of including a simplified method for market risk capital requirements in the Basel framework.

The full document is available here.

Who is it for?

The proposed approach is for banks with a low concentration of trading book activity and smaller banks that typically do not have sufficient infrastructure for the Sensitivities-based Method.

The BIS document also provides a more specific list of criteria for banks intending to use the simplified method:

- The bank must not be a G-SIB or D-SIB (Global/Domestic Systemically Important Banks)

- The bank must not be engaged in writing options (with the exception of back-to-back options and covered options whereby the bank owns the securities it may need to deliver under the terms of the option).

- The bank must not use the internal models approach for any of its trading desks.

- As measured by the bank’s relevant accounting standard, the bank’s total non-derivative trading book assets and liabilities plus the sum of the gross fair value of its trading book derivative assets and liabilities must not exceed [€1.0 billion]

- The bank’s total market risk-weighted assets, when using the R-SbM, divided by its total risk-weighted assets, are less than [5%].

- The aggregate notional amount of non-centrally cleared derivatives (including both banking book and trading book positions) must not exceed [€X billion].

- The bank must not hold any correlation trading positions.

Simplification Details

While the aggregation formulas for the Delta risk charge are the same as in the SbM, there are a number of differences in what BIS now call the Reduced Sensitivities-based Method (R-SbM), which I summarise by asset class below.

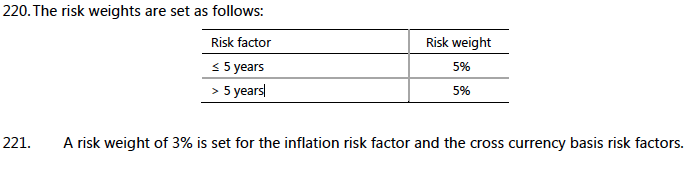

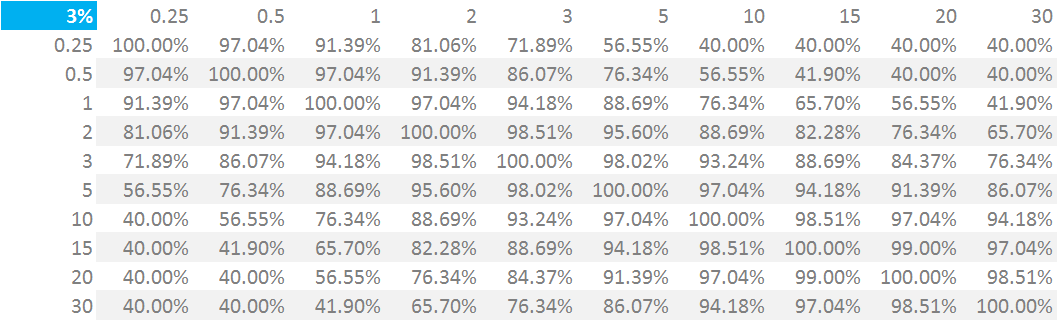

Interest Rate Risk

The R-SbM tenor vertices and risk weights are:

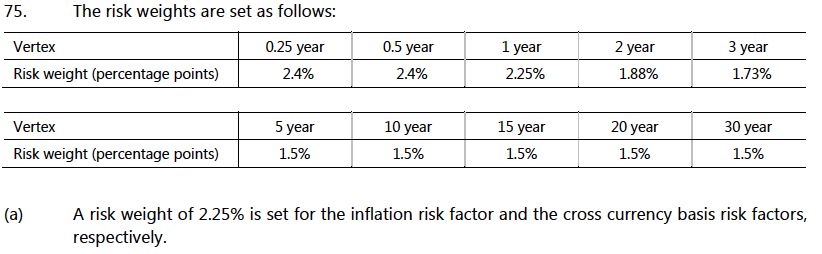

Compared to the SbM, which has:

Risk weights of 5% to 1.5% are significantly higher in the R-SbM and these are key drivers of the capital charge Consequently RSbM will have a significantly higher capital charge.

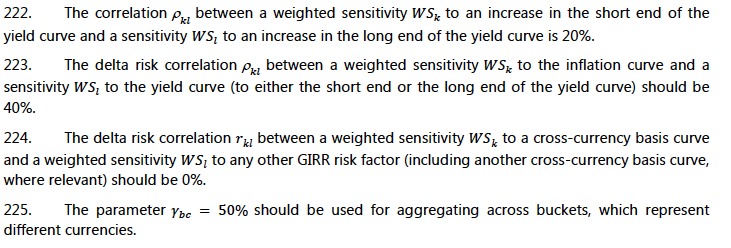

The R-SbM specifies the following correlations:

These are much lower than the formulae for SbM, which Chris worked out in his blog here as:

So substantially different with the 5Y vs 10Y correlation from this being 97% as opposed to the 20%, meaning a curve position such along 5Y and short 10Y in equal DV01, will have higher capital charge under R-SbM due to the correlation used in the aggregation formulae.

In addition it seems that the R-SbM does not require Libor 3M and Libor 6M to be sperate curves as just one risk-free yield curve per currency is specified.

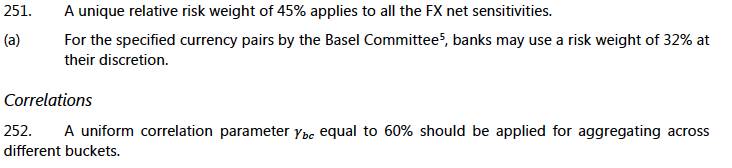

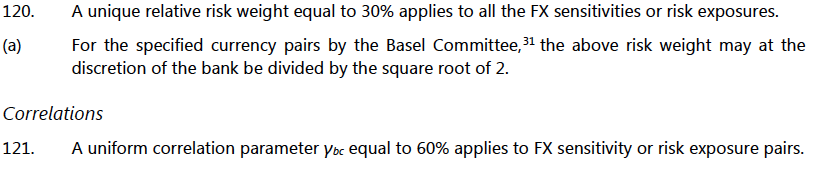

Foreign Exchange Risk

The R-SbM specifies:

While SbM has:

Again, you get the picture, a higher risk weight 45% to 30%, resulting in a higher capital charge.

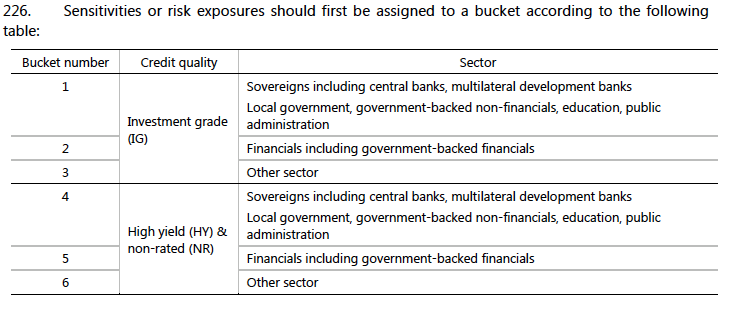

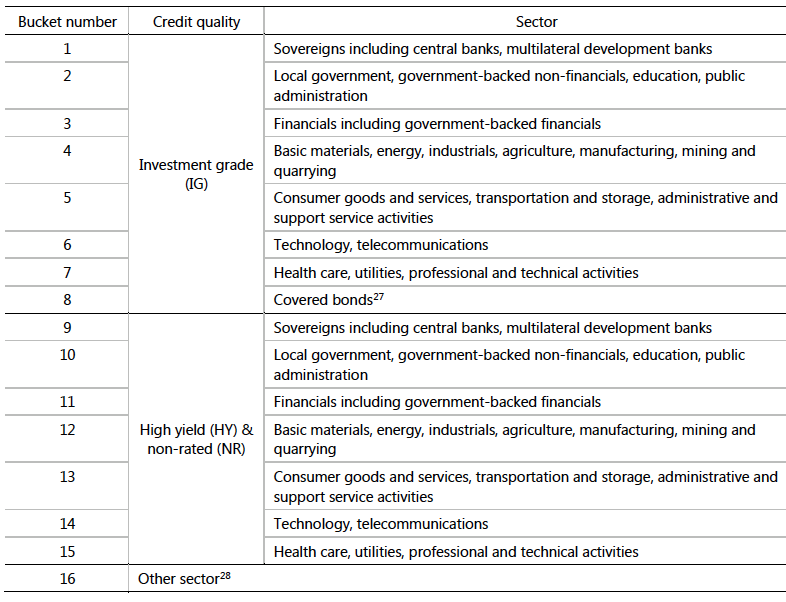

Credit Spread Risk

The R-SbM has less granular buckets as follows:

Compared to the SbM with:

I am not going to re-produce the associated Risk Weights and Correlations here, suffice to say they are generally worse in the R-SbM.

Equity and Commodity Risk

If you are interested on details on these, I refer you to the BIS document available here.

Suffice to say the same philosophy as IRR, FX, CSR holds, with the R-SbM having less granular buckets, higher risk weights and lower correlations.

Final Thoughts

The Reduced Sensitivities-based Method (R-SbM) is simpler than SbM.

However it will result in higher Market Risk Capital.

The absolute difference may not be material for small banks.

As their Capital requirement will be dominated by Credit Risk.

However for banks with a Trading business, the difference will be material.

Making the R-SbM much more expensive.

The BIS Consultation closes September 27, 2017.

It will be interesting to see what emerges in the final document.