Following on from my article FRTB – Internal Models or Standardised Approach, I wanted to look at specific component of the Internal Model Approach (IMA), namely the fact that all risk factors are subject to a Modellable or Non-modellable requirement and non-modellable risk factors result in a higher capital charge.

Background

In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known as the Fundamental Review of the Trading Book (FRTB). These new standards replace parts of the Basel 2.5 reforms, which were introduced in 2009 to address the material undercapitalisation of trading book exposures during the 2007-08 financial crisis. (Document is here).

Internal Models Approach (IMA)

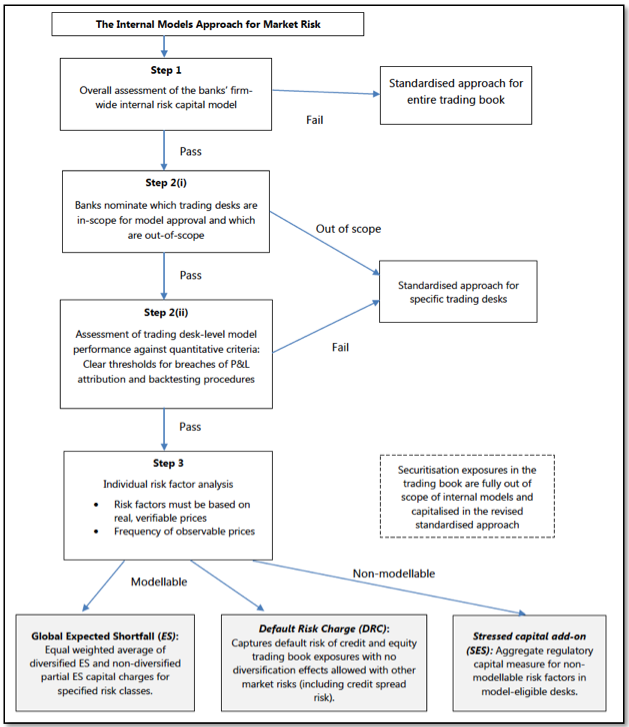

Lets start by looking at the Overview chart from the BCBS document.

Which shows that Step 3 is an Individual Risk Factor analysis, after which:

- Modellabale risk is included within a Global Expected Shortfall (ES) and a Default Risk Charge (DRC)

- Non-modellable risk is subject to a Stressed capital add-on (SES)

Lets look at these in detail.

Modellable Risk Factor Analysis

This step determines which risk factors are eligible to be included in a bank’s internal model for regulatory capital. Paragraph 183 (c) of the BCBS document states that for risk factors to be classified as modellable there must be continuously available real prices for a sufficient set of representative transactions. A price will be considered real if:

- It is a price at which the institution has conducted a transaction;

- It is a verifiable price for an actual transaction between other arms-length parties; or

- The price is obtained from a committed quote.

- If the price is obtained from a third-party vendor, where: (i) the transaction has been processed through the vendor; (ii) the vendor agrees to provide evidence of the transaction to supervisors upon request; and (iii) the price meets the three criteria immediately listed above, then it is considered to be real for the purposes of the modellable classification.

A specific test is then specified for continuously available real prices:

- a risk factor must have at least 24 observable real prices per year

- with a maximum period of one month between two consecutive observations

- the above criteria must be assessed on a monthly basis

- and measured over the current ES period (e.g. past 12 months)

[UPDATE: January 2019, this criteria has been revised, see FRTB RFET.]

Note that this test must be applied to all risk factors, from the highest volume which trade continuously (e.g. USD IRS 10Y) to the lowest volume which trade in-frequently. While the former should easily pass the requirement, there will be many others in the world of OTC Derivatives that will not pass easily e.g. Swaption Volatilities for longer expirys and tenors.

And “any real price that is observed for a transaction should be counted as an observation for all of the risk factors concerned (i.e. all risk factors which are used to model the risk of the instrument that is bought, sold or generated through the transaction as part of the overall portfolio)”.

Risk factors derived solely from a combination of modellable risk factors are modellable, e.g. Equity Betas.

Once a risk factor is deemed modellable, the bank should choose the most appropriate data to calibrate its model – the data used for calibration does not need to be the same data used to prove that the risk factor is modellable.

Where a risk factor deemed modellable is not available during the historical period used for stressed calibration (e.g. 2007-08), proxy data can be used provided the general approach for generating old missing data is documented and part of the independent review of the internal model by the bank’s supervisory authority.

Non-Modellable Risk Factor (NMRF)

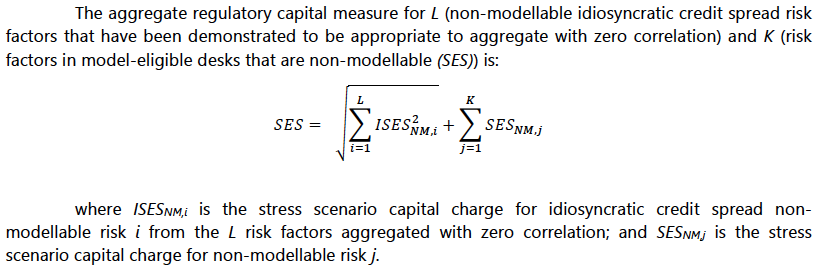

Risk factors that do not meet the modellable criteria are by definition non-modellable and each risk factor has to be capitalised using a stress scenario calibrated to be at least as prudent as ES at 97.5% calibrated over an extreme stress period.

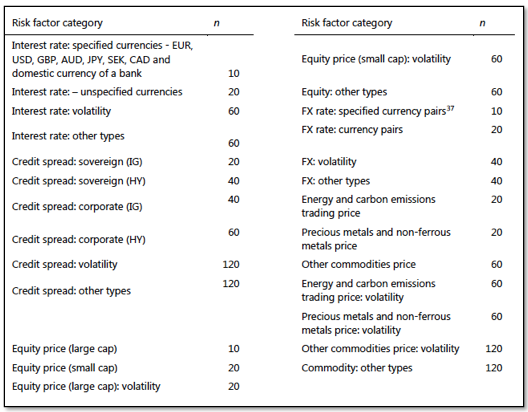

For each non-modellable risk factor, the liquidity horizon of the stress scenario must be the greater of the largest time interval between two consecutive price observations over the prior year and the liquidity horizon assigned to the risk factor as below.

Meaning that we may end up with longer liquidity horizons than above for specific risk factors, resulting in a higher stress scenario charge.

In addition no correlation or diversification effect between other non-modellable risk factors is permitted.

Meaning that the aggregation of stress results will lead to a much higher charge than aggregation for modellable risk factors under ES, where diversification is permitted within a risk class.

The BCBS document then gives the following:

Thoughts

Given the above it is important that sufficient importance is given to the task of determining modellable risk factors as the cost of not doing so is a much higher capital charge.

All risk factors need to pass the continuously available real prices test.

And as the risk factors in question here are pertinent to what a bank trades, a good start point is to take the current set of risk factors used in production for market risk capital and map these to the history of a bank’s own trades, analysed each month for the prior 12 months to see if the 24 trades and monthly gap test is met and so determine for which of these risk factors the requirement can be satisfied.

However this exercise is likely to leave a lot of risk factors failing the test even for the largest global banks, as a trading desk may quite readily have a current risk position, which the bank has not traded 24 times in the past year and traded at least monthly.

Not only will too many non-modellable risk factors result in a higher capital charge, they will also make it more difficult to satisfy the P&L attribution and Backtesting requirements for Trading Desk IMA, which ultimately result in a fall-back to the Standard Approach (higher capital).

Consequently it is important to minimise the list of non-modellable risk factors by looking for:

- sources of trade data that cover many parties transactions, or

- rely on third-party vendors that have processed the transaction and will provide evidence of the transactions to supervisors on request.

Possible vendors for the second are Exchanges, Trading Venues, Affirmation platforms, Clearing Houses, ..

Possible source for the first are Swap Data Repositories (SDRs) and Trade Repositories (TRs).

And it is the latter that is of most interest to us.

After all banks and the industry as a whole have spent a lot of time, money and resources to report OTC Derivatives trades to Repositories and in certain jurisdictions there is public dissemination of trade-level data.

Surely this data can be leveraged to re-coup some of that investment.

We believe it can.

The End

Our SDRView product has transaction level OTC Derivatives data reported by US persons for all Asset Classes covering the period from the inception of mandatory trade reporting to the present. This data is granular enough to identify the risk factors of the trade and such a source can be used to:

- evidence that the continuously available real prices test is met, and

- determine liquidity horizons for non-modellable risk factors

Please contact us for information if you are interested in doing this.

UPDATE: We now offer free 14-day trials for our FRTB for Excel product