- ISDA SIMM versions are annual with go-lives in december

- This year for the first time there will an off-cycle release

- SIMM v25a will be effective July 15, 2023

- It is necessary due to signifciant interest rate moves in 4Q 2022

- Higher interest rate delta risk weights will increase IM for many portfolios

- Clarus CHARM can run both SIMM v2.5a and v2.5 now on your portfolios

- Months before go-live, to quantify the margin impact

Version 2.5a

ISDA has published ISDA SIMM v2.5a with a re-calibration of interest rate risk weights only.

This is an off-cycle release, due to the higher interest rates volatility observed in 4Q 2022, compared to that in 2019-2021 and the stress period of Sep-08 to Jun-09; the time period used for the calibration of v2.5.

Quarterly industry monitoring of actual portfolios has led to the need for an off-cycle release, v25a in July 2023, almost 4-months earlier than the next annual release (v2.6) scheduled for December 2023.

CHARM

Clarus customers using CHARM or Microservices are able to easily run SIMM v2.5a and compare the margin with SIMM v2.5 for their actual or hypothetical portfolios, before the go-live date:

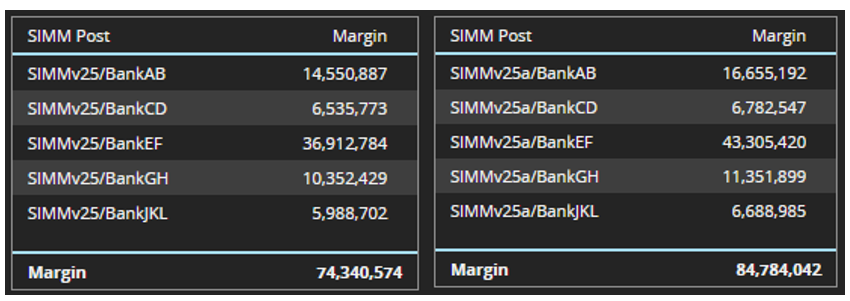

- The total gross margin for these increasing from $74.3million to $84.8 million

- An increase of 14% for the total margin; significant indeed

- However increases depend entirely on the interest rate risk in the portfolios

- And changes at the counterparty portfolio level are more important

- These can show a wide variation in changes

- For our hypothetical portfolios, the range is a 4% to 17% increase

Portfolios with risk pre-dominately in Commodity, Credit, Equity or FX would see no change or non-material changes of less than 1%.

Portfolios with material Interest Rate Risk (e.g. Swaptions, Caps/Floors, Interest Rate, Cross-Currency Swaps) would see signifciant increases, most likely in the 6% to 14% range.

Eyeballing the new re-calibrated risk weights, we can observe the following:

- For regular currencies, the 2w to 6m risk weights are lower, while 2Y and above are higher, in particular 5Y is up from 52 to 60, an increase of 15%

- For low voltaility currencies (JPY), risk weights from 3Y and above are higher, with 10Y increasing from 19 to 23, an increase of 21%

- For high volatility currencies, risk weights are higher for all tenors except 30Y, with the shortest 2w tenor, up from 119 to 163, an increase of 37%! 1Y is up from 90 to 102 or 13% and 3Y from 95 to 101 or 6%.

This gives us an idea of which risk factors will result in increases and the ballpark of the possible increase. However the only way to really know is to calculate SIMM v2.5a on your actual portfolios and compare results.

CHARM makes this easy to do, months before the actual change.

Foresight is fore-warned and allows for better planning of collateral requirements and pre-emptive action.