In August I looked at the potential for valuation challenges as for non-cleared derivatives. This month I will cover the additional challenges for risk management and reporting that would arise with a pre-cessation announcement.

A LIBOR pre-cessation announcement from the FCA could occur by the end of 2020. This was first discussed publicly in June 2020 and has been repeated several times since.

The original intention was to time the pre-cessation announcement to follow the date when the ISDA Supplement and Protocol become effective. ISDA had initially indicated the effective date could be November or December 2020, i.e. 3 – 4 months after the announcement initially scheduled for 27th July 2020. However there have been a few delays and the confirmed effective date is now 25th January 2021.

The actual FCA announcement could still occur in 2020 or alternately early 2021. This would give impacted firms more time to fully develop their transition process with a higher degree of certainty about the dates when financial instruments with the pre-cessation trigger would actually move to the fallbacks.

But not all financial instruments will include the pre-cessation trigger and may not be moved to the fallbacks. These are either the ‘tough legacy’ trades or derivative hedges for these trades.

Therefore, many portfolios could actually have a mix of trades which would be subject to a pre-cessation trigger event and some with other triggers.

Added to the complexity is the probability that a variety of fallback methodologies (e.g. lookbacks, lockouts etc.) may come into play at the same time. Or a different time if the trigger events differ!

This blog looks at the possible impacts of a pre-cessation announcement on the risk management and reporting.

The pre-cessation announcement

When (rather than if) the FCA does announce that LIBOR is no longer representative of the underlying market a number of important changes are put in play:

- The ‘spread’ is set in accordance with the Bloomberg Fallback Rate Adjustments Rule Book;

- The derivative trades which are subject to the ISDA Supplement and/or Protocol will be contractually moved to the specified fallbacks for LIBOR benchmarks from the FCA announced LIBOR cessation date; and

- The risk vectors in the trades with the pre-cessation trigger move to the fallbacks rates from LIBOR from the announcement date but only for those rate fixes after the cessation date.

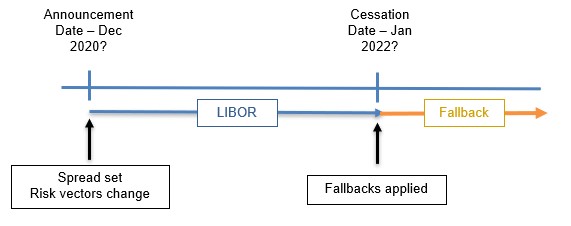

The FCA pre-cessation announcement is likely to be well ahead of the cessation date which is still expected to be 1st January 2022. The dates are quite important and the risk will change on the announcement date for trades referencing the pre-cessation trigger.

The timeline looks like the following. In this case the ‘Cessation Date’ is the one defined in the pre-cessation announcement and it may not coincide with a permanent cessation date for LIBOR.

The actual announcement could take a number of different paths: there is no precedent and no specific format. For example, the FCA could simply announce all LIBORs are not representative thereby triggering the fallbacks and setting the spreads for all LIBOR currencies and tenors.

Or the FCA announcement could specify LIBOR currencies and tenors rather than a blanket ‘all-in’ announcement. In this case, only the spread and fallbacks are triggered for certain currencies and tenors.

In any case, the announcement will have significant impacts on risk management and reported risk for most firms. These changes will be in effect from the announcement which may be well ahead of the actual cessation event.

Pre-cessation announcement or permanent cessation?

The definitions can be confusing as both pre-cessation and permanent cessation have a reference to the ‘Cessation Date’.

The pre-cessation announcement allows for a regulator or licensing entity, in this case FCA, to declare LIBOR not representative of the underlying market from a particular date. This date is referred to as the ‘cessation date’ for the pre-cessation trigger. In this case, the benchmark may continue to publish but all contracts referencing this trigger will apply the fallbacks from the cessation date.

If the benchmark continues to be published after the date used for the pre-cessation trigger then it can still be referenced in contracts that do not include the pre-cessation trigger. In this case, the cessation date has not been reached for these other triggers.

Of course, if the benchmark is discontinued then this is the cessation date for all triggers. Such a discontinuation event may pre or post-date the cessation date of the pre-cessation trigger.

All very confusing but the easiest way to think about this is that every trigger can define its own cessation date.

Risk management after a pre-cessation announcement

After the pre-cessation announcement the fallbacks are legally implemented from the future date only for those trades with this contractual inclusion. All other trades remain on the existing benchmark.

For example, the trades subject to the ISDA Protocol or cleared at a CCP will have this trigger and the risk is now moved to the fallback post the cessation date of the trigger. Also, trades which have been bilaterally negotiated to add the pre-cessation trigger will also move the risk to the fallback.

However, any trades without the pre-cessation trigger will very likely still be on the old benchmark.

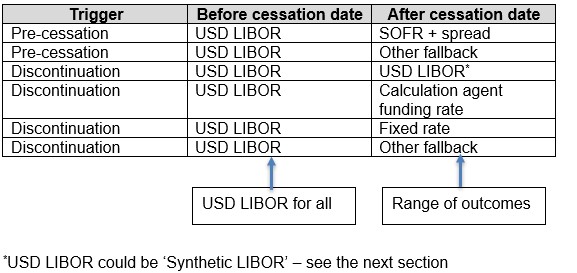

By way of example, if we consider a USD LIBOR trade it could take the following paths:

After the cessation date for the pre-cessation trigger there will be a number of potential outcomes. These range from the ISDA fallbacks to ‘other fallbacks’ and the common ‘calculation agent funding rate’ and ‘fixed rate’.

All of these outcomes will have to be mapped to different curves as they may well have a basis between them and therefore move relative to each other.

Traders will have to recognize this difference and, if possible, manage the basis risk.

Also, second line risk will need to manage limit use for each outcome, report the risk against the limit and probably calculate VaR based on the actual fallbacks. Since this activity is very often subject to regulatory oversight and reporting, ensuring the risk calculations are accurate will be critical.

And this will need to commence at the time of the pre-cessation announcement.

Synthetic Libor

Much work has been done on the ‘tough legacy’ issue in UK and USA and the possibility of legislative remedies or having a synthetic (also referred to as zombie) LIBOR published for those contracts and issues that simply cannot move from LIBOR.

As it happens, FCA does actually have the ability to direct the publication of a synthetic LIBOR and very likely the methodology. The FCA have previously indicated they may try to make this synthetic LIBOR resemble to the ISDA fallbacks (Term RFR plus fixed spread). Of course, a synthetic LIBOR with a dynamic credit spread could also work and may be closer to the current LIBORs. The USA has had several discussion on how this may be achieved but there has been no practical progress to date.

But the exact methodology is not known at this time. And whether FCA will exercise their ability to direct the publication is also uncertain.

But a synthetic LIBOR may be a useful addition for tough legacy positions. However, given the methodology of the calculation is not well progressed there is a real risk of relying on it as a viable post-cessation alternative.

Summary

If all trades and positions have a pre-cessation trigger and use ISDA fallbacks then risk management and reporting would be simple.

However, this is very likely not the case for many firms who will have to contend with a range of trigger and fallback combinations. These will have to be accurately tracked per trade so that risk can be calculated and managed for each option.

Risk reporting is also likely to be challenging both in the management of limits and position to each option as well as the calculation of VaR.

Clarus CHARM or Microservices can greatly assist in providing the necessary toolkit to deal with fallbacks in contracts referencing LIBORs.