The past few months I have been looking closely at the potential for valuations challenges over the last months and days of LIBOR with a potential cliff and wall as we approach December 2021. The rather benign pricing in the market predicts a very gradual ‘glide’ into the end but this may not actually be the case.

The visible market pricing is generally based on cleared derivatives: swaps and other derivatives which are assumed to be cleared at CCPs. If one or both sides of the trade prefer (and are permitted) to trade outside the cleared system then the price can vary. For example, XVA adjustments can be added to prices moving them away from the theoretical mid.

This blog looks at the impacts of fallbacks on the pricing and valuation of non-cleared derivatives which can even start with a different base curve (to cleared derivatives) before XVAs are added.

Certain derivatives are likely to use a variety of fallbacks and triggers (perhaps to align to the underlying risks of loans and debt issues) and would not be eligible for clearing. Derivatives with non-ISDA fallbacks may value very differently to their cleared versions.

The problem with valuing all derivatives using the market prices (i.e. cleared derivative) is that the revaluation curve may not be the correct one for that trade.

The preferred fallback and trigger for transition will need to be negotiated bilaterally if the ISDA Protocol is not used. Although it is expected that the ISDA LIBOR fallbacks will be widely adopted, certain trades and counterparties may require alternatives.

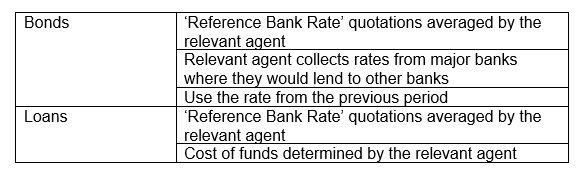

Possible cash product approaches to IBOR fallbacks

In general, any counterparty can have several options for a fallback in derivatives which may be required to maintain derivatives matched to underlying risks.

For example, some debt and capital instruments issued by firms are managed within highly rated (AAA) trusts or special purpose vehicles. In these cases, the fallback for IBOR in the underlying issue may be difficult to change which generally means the derivative needs to exactly match the issue leading to a customized fallback and trigger combination.

Current non-ISDA IBOR fallbacks examples include:

And, of course, the triggers can also be different! We see cessation, pre-cessation and other potentially others in the mix of options.

The derivatives may need to be changed to match the cash product trigger and fallback to maintain the important ‘hedge’ status.

New ISDA fallbacks

Much has been written on the proposed ISDA fallbacks and triggers which I will not repeat here. However, the key features are:

- IBOR fallbacks are changed to be more robust and prescriptive;

- In case of an IBOR permanent cessation, the IBOR is typically replaced with:

- An ARR (Alternative Reference rate) compounded over the relevant period; and

- A spread added to the compounded rate reflect the historical (5-year median) of the difference between the IBOR and the compounded ARR.

Much of the derivative market is likely to adopt the ISDA fallback changes. As we are aware, major CCPs (LCH Swapclear and CME) showed early and consistent support for the ISDA fallback language and triggers. They have stated they will change Rule Books to be consistent with the ISDA fallback approach.

The Fallback Calculation

The ISDA spread will be fixed at some point between now and the cessation date of USD LIBOR commonly expected to be on the pre-cessation announcement by the FCA.

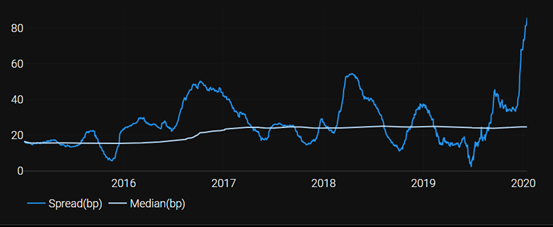

I have used the following USD charts in both previous blogs and they are just as relevant here.

The spread (5-year median) is the white line on the following charts and clearly shows low volatility around 11.5 bps for 1-month while the 3-month spread is around 26 bps.

So, all is well understood for an ISDA fallback.

But non-ISDA fallbacks (and therefore spreads) are determined at the time of the rate fix as is the case for IBORs now. These rate fixes could follow the blue lines and the spread to the ARRs could be significant compared with the ISDA approach.

If the past is any indicator of the future, fallbacks based on the funding rates at the time (similar to current IBORS and commonly used by cash instruments) could be very different to the ISDA fallbacks with a compounded ARR plus a fixed spread.

If a counterparty is hedging a cash instrument, then they may pay close attention to this potential difference. They may be required, or prefer, an exact hedge for their fallback in the debt issue or loan which means a customized, non-ISDA fallback for the derivative hedge.

How do you value the non-cleared, non-ISDA derivatives?

Based on the historical performance of the USD LIBOR spread relative to the ISDA (and cleared) spread the challenge is how to value a derivative with a fallback which is not based on the observable market prices, i.e. cleared derivatives.

Not only does the credit and liquidity spread vary but ARRs tend to set in arrears while the alternative set in advance. So how accurate is the forward-looking calculation and the spread?

The observable market is the CCP-cleared derivative which is only one of the alternatives. The other fallbacks may, and likely will, have no truly observable market.

This potentially leads to a probabilistic pricing approach where the outcomes may be better approximated with a simulation. Although this approach could work for fallbacks which act similarly to LIBOR and may have similar volatility characteristics which can be reasonably calculated from historical data, some (e.g. the calculation agent’s ‘funding rate’) may be more difficult to model.

But individual firms will need to make a decision on how to price non-ISDA fallbacks without a current pricing curve.

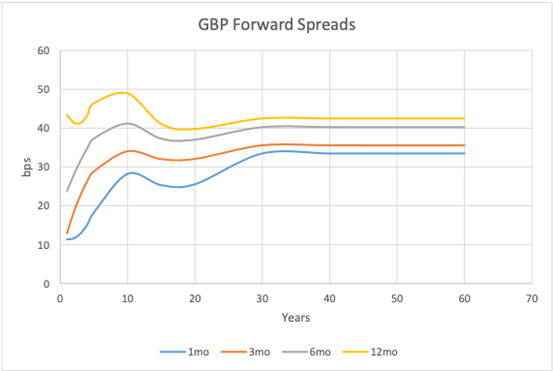

What about the term structure of non-cleared derivative fallback spreads?

Some commentators have pointed out the possible term structure for the spread in the past. The following chart from May 2018 shows the market price for GBP forward spreads for 1-month to 12-month LIBOR minus OIS.

In May 2018, before the ISDA consultations, there was a very clear term structure for the spread in GBP. For example, the 1-month spot spread is around 11 bps while the 40-year spread is closer to 33 bps.

However, the ISDA fallback has a fixed spread (i.e. flat line) across the entire curve because the ISDA spread is calculated from the 5-year median of the spot spread.

Again, the observable curve is the cleared basis curve which follows the ISDA fallbacks and is now flat past 2022.

But it this the correct term structure for a non-ISDA fallback? Should that curve be more similar to the one which pre-dated the ISDA consultations in May 2018?

And if so, how should it be modelled and priced?

In Summary

When looking at alternatives to ISDA fallbacks, pricing can be challenging and the inputs may not be observable. It is important to recognize this fact and plan accordingly.

This is especially important when matching derivatives to underlying risks and ensuring hedges include fallbacks which actually offset the risk.

Clarus systems such as Clarus Microservices can greatly assist in providing the necessary toolkit to deal with fallbacks in contracts referencing LIBORs. The complexity introduced by the potential for differing fallbacks, and understanding event-driven valuation changes, raises the real possibility that legacy enterprise systems will no longer be able to handle even vanilla trades. And certainly their time to change and implement is a hurdle to understanding this complexity right now.

This is why we see a change in the industry toward flexible trade-stores. Multiple different services can then access the primary (and secondary!) economic terms of a contract to perform domain-specific processes. This is precisely the architecture that Clarus Microservices is designed for.