Last week I wrote about the uncleared margin rules (UMR) that mostly came into effect on September 1 in the US & Japan. We concluded that:

- No evidence of a September 1st panic; there did not seem to be any halt or reduction in swaps trading through the new mandate

- Clearable swaps that have no clearing mandate showed:

- No noticeable change in clearing behavior for Swaptions and FX NDF

- Inflation: An increase of clearing activity from 15% to 75%

- Truly non-clearable swaps (eg xccy swaps) showed only little evidence of reduced US-named activity.

I was intrigued to see that yesterday, Risk Magazine ran an article that claimed:

- 95% of the inflation market is now cleared, compared to 10% in August

- The 10% (In August) corresponded to roughly 30 cleared trades per day at LCH

- IDB’s are now quoting LCH mid-market prices, reflecting the fact that the inflation swap market is primarily a cleared one now.

With that extra insight, and another week under our belt, I thought it appropriate to update the analysis.

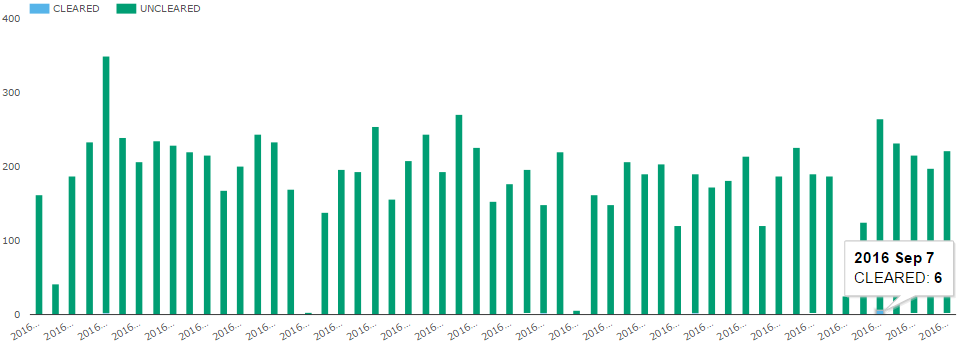

Swaptions

Keeping the same order as last week, let’s begin with swaptions. SDRView activity for swaptions in G4 currencies shows a handful of cleared swaptions in July and August, and 6 trades in September. It’s actually quite difficult to even see the blue cleared trade activity amongst the 200 or so uncleared swaptions traded each day. Hence still not much of a story here.

Slightly more confounding is that CCPView, which tracks cleared activity reported by the CME clearing house for swaptions, seems to show only the 1 cleared swaption from September 1st. I’ll spare you the chart, given that a chart for one data point is like looking at a dot; not very interesting. But if you are an SDR data junkie (and who isn’t?), what this means is that there are swaption trades being flagged as “intended to clear” when executed, but that are not being cleared. Whether that is bad trade reporting, or a case of trades failing to clear for valid reasons, or perhaps the trades will clear in a few more days, we don’t know.

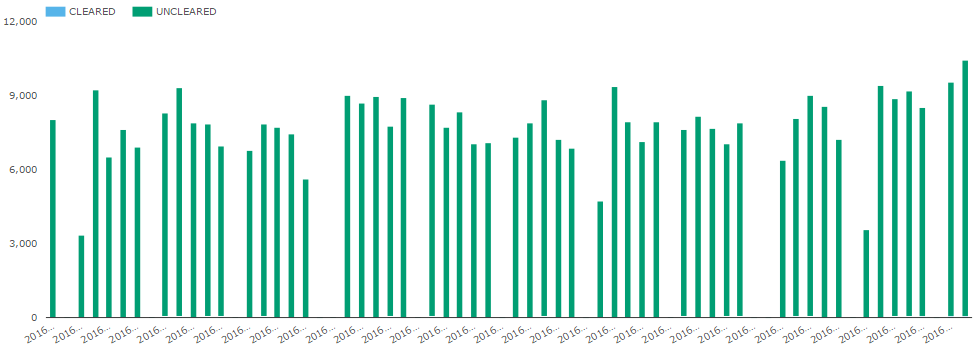

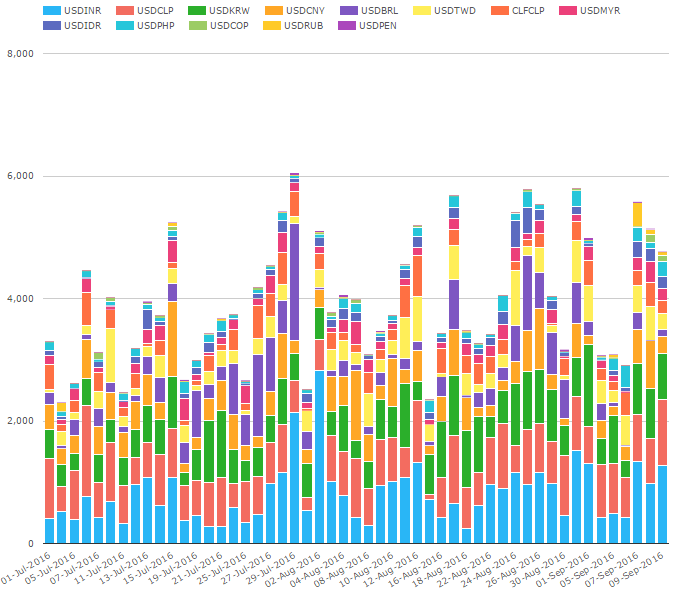

FX NDF

Next up, FX NDF. I’ve chosen to include all 14 active currency pairs this week. SDRView shows nearly 8,000 trades dealt per day, and no matter how hard I try, I am not able to highlight the chart for the 20 or so cleared trades that happen on some days.

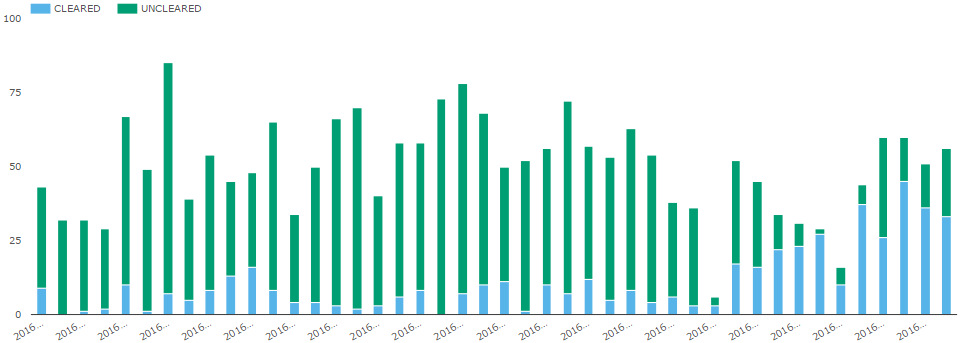

So let’s remove all the uncleared trades and just examine what is cleared:

This tells a slightly more interesting story, as indeed the daily average in September (post-mandate) shows perhaps 15 or so more cleared trades each day, peaking at 45 trades on September 12.

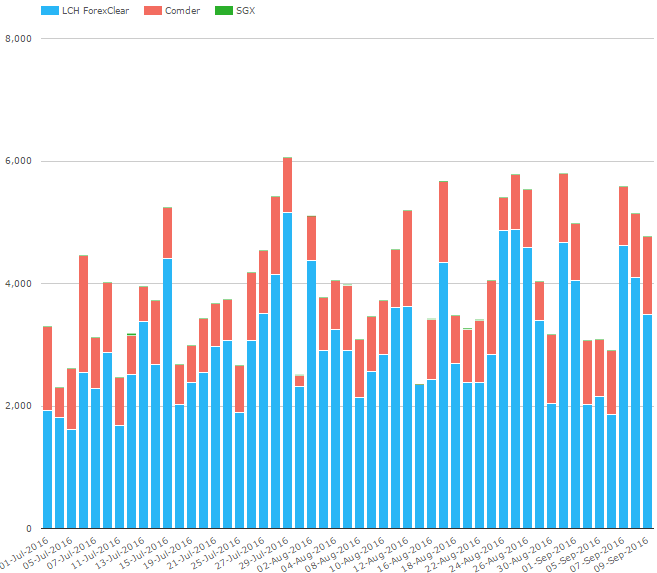

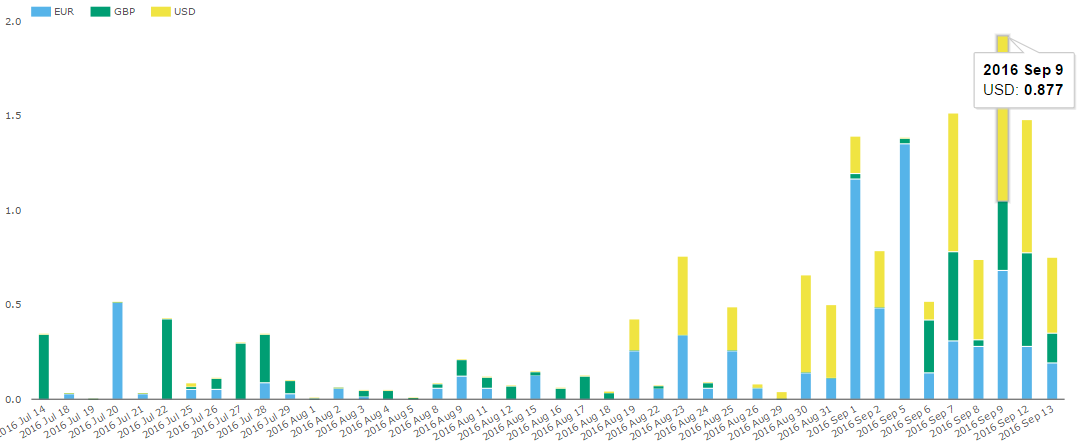

And if we look at FX Clearing Activity in Notional terms on CCPView, it’s a bit more of a mixed bag. Note this is only through September 9th, as this data is reported weekly.

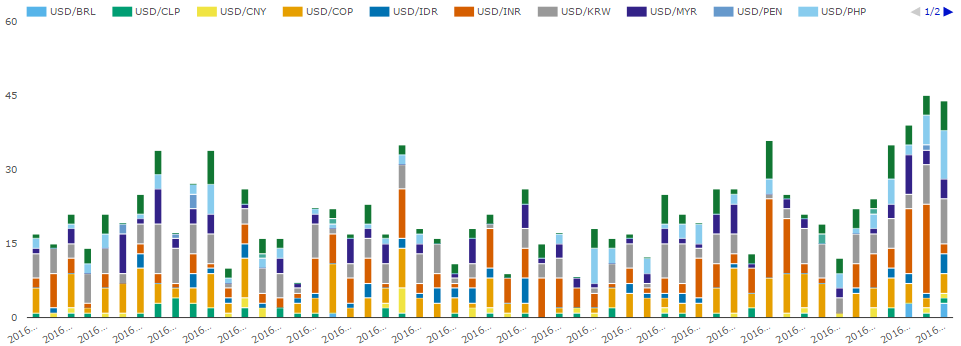

And now, looking at notional cleared by CCY Pair:

Again a bit of a mixed bag.

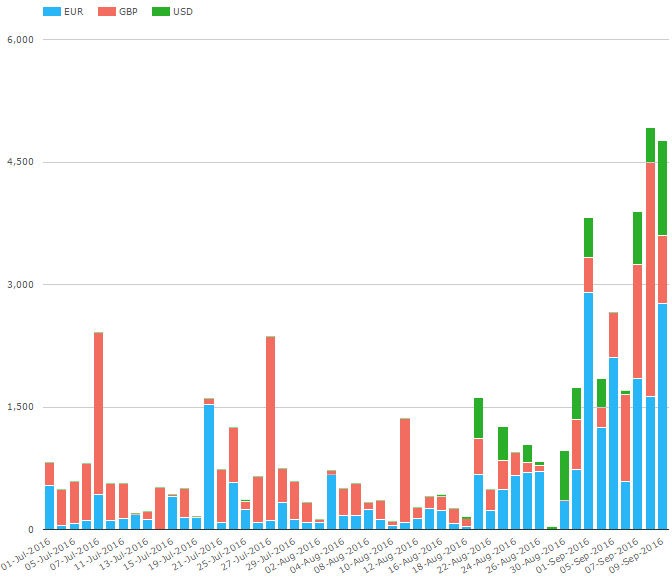

Inflation Swaps

Let’s start with SDRView data for the past 2 months of inflation swaps in G4 currencies:

And indeed this seems to be the success story coming from uncleared margin rules. There seems to be a total daily average of about 50-70 trades per day – remember this is just US-named SDR activity – and we can now see as much as 45 cleared trades on September 9th.

Let’s now remove the uncleared swaps and refine the analysis for cleared-only inflation swaps. From a notional perspective, these cleared trades in September account for aggregate notional sizes of up to 2 billion USD equivalent. The following chart suggests there is suddenly a cleared USD inflation swap market!

If we now take a global look at Inflation data on CCPView, the story is nicely corroborated:

Remember that the Risk Magazine article stated that the global inflation swap market shifted to cleared in the past couple weeks. Our data seems to generally support this:

- The US-named (SDRView) business shows upticks of 1 to 1.5 bn per day in cleared inflation swaps

- The global cleared data (CCPView) shows an uptick of 2 to 4 bn per day

- Quick attempt to confirm the notion that cleared trading has jumped from 10% to 95% of the market. Back-of-Napkin math could support this if you say that cleared activity has gone from ~500 million to ~4.5 bn. This would, however, require you to believe that ~500 million is 10% of the market, and even the most recent BIS report doesn’t seem to break out inflation swap trading, so that remains unconfirmed.

Also noteworthy is the fact that there doesn’t seem to be much USD denominated inflation swaps cleared at LCH prior to the mandate. Note that this might be due to something explained in the Risk Magazine article – that USD inflation swaps have a nuance that makes offsetting cleared trades difficult.

Summary

It would seem the UMR’s have indeed had an impact on one product: welcome to the new cleared inflation swap market.

FX NDF shows only a small glimmer of evidence in any change. I do wonder if that might be because the universe of trades in NDFs encompasses the full gamut of Category 1, 2, 3 etc firms, whereas inflation swaps might be more large-dealer driven.

Swaptions data not yet supporting any story here.

But of course time will tell. Stay tuned.