- We detail the trades required to raise USD from a local central bank, using the Fed USD swap lines.

- We show that the cost of these USD is substantially below that implied from FX markets.

- The FX haircuts on non-USD collateral for these operations vary between central banks.

- The largest amounts outstanding in these USD operations historically have been nearly $600bn.

- This week, roughly $160bn was raised by banks.

- The new daily operations

Tuesday 24th and Wednesday 25th March 2020will be very closely monitored.

More USD Please

**Update 20th March 15:00** Central banks have just announced that these auctions will now run daily for 7 day funds.

The Fed has just extended the list of central banks that it offers USD to:

The total list, with amounts, now reads as:

- Japan (BoJ) – $ unlimited

- Bank of Canada (BoC) – $unlimited (?)

- Europe (ECB) – $ unlimited

- UK (BoE) – $ unlimited

- Switzerland (SnB) – $ unlimited (?)

- Australia – $60bn

- Brazil – $60bn

- South Korea – $60bn

- Mexico – $60bn

- Singapore – $60bn

- Sweden – $60bn

- New Zealand – $30bn

- Denmark – $30bn

- Norway – $30bn

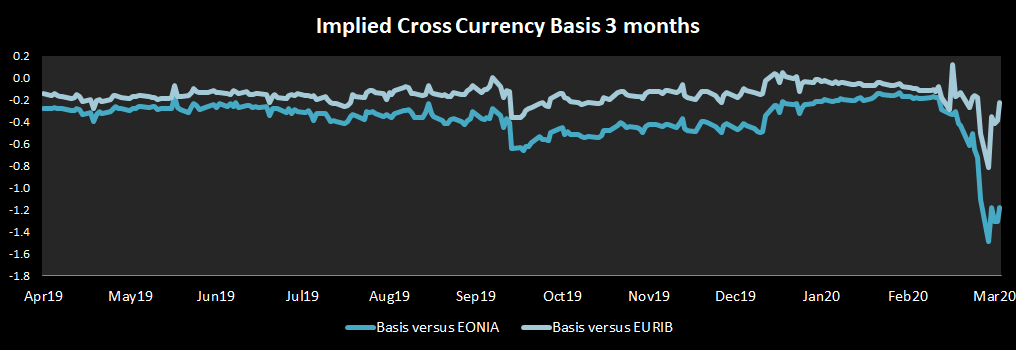

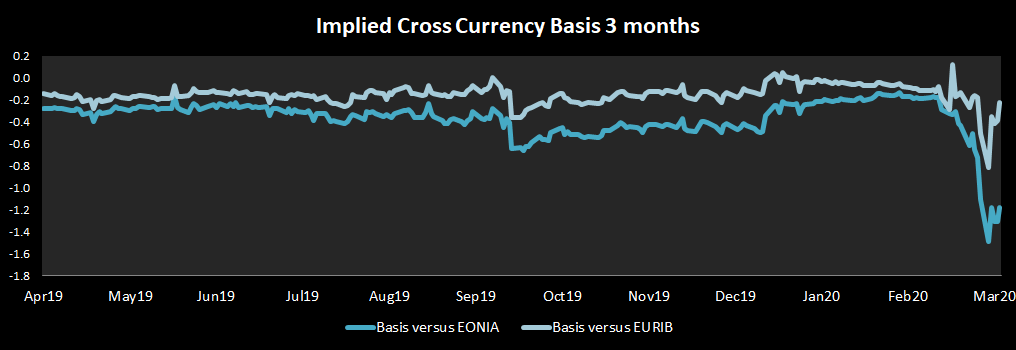

This is in reaction to the extreme volatility we have seen in the short-end of cross currency basis swap markets recently:

This blog will ask what are these central bank FX swaps, how do they work and what has the market appetite/impact been for them?

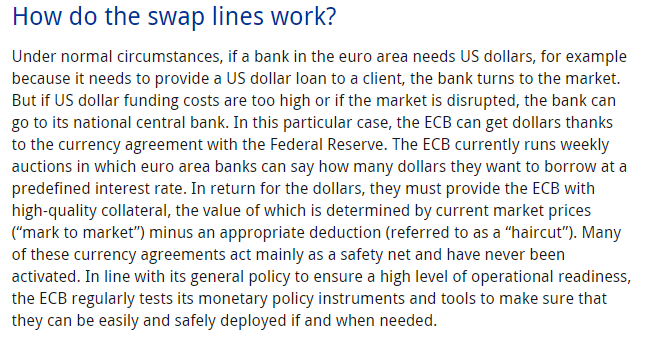

Cross Currency Swaps between Central Banks

These FX swap lines are more akin to a cross currency swap than FX swaps, although I am splitting hairs here. For a bank accessing these USD funds from their central bank, they must:

- Lend domestic currency to their local central bank. This can be in any form of eligible collateral. Any non-USD collateral posted to the local central bank will attract an additional FX haircut, on top of any haircut typically associated with it.

- In return, the local central bank (e.g. the ECB) will lend to the bank an equivalent amount of USD at OIS + 25 basis points.

- An FX rate is set by the central bank at the start of the swap. This FX rate is used for the initial exchange of notional. I have just learnt from this ECB document that the swap has weekly FX resets applied to it. This means that the FX rate is restated once every week, and the EUR amount of collateral held rebalanced weekly accordingly. Interesting!

The cashflows are as follows, excluding these FX resets and weekly EUR interest (see below).

These cashflows are very similar to those set out in one of our popular blogs Mechanics of Cross Currency Swaps. If you want to see an example with the FX Reset cashflows included, please refer to that original blog.

Please note:

- The USD interest is fixed at the start of the cross currency swap. The USD coupon is set at OIS + 25bp. Looking at the results of the 18th March 2020 allocations, a USD 3 month OIS (Fed Funds vs Fixed) must have been at 0.13%, as the total coupon was 0.38%.

- Reading through the tender procedure from the ECB here, it is not 100% clear what rate is paid on the EUR collateral posted. However, I think it is safe to assume that the collateral posted with the central bank will be treated along with all other collateral. So if it is posted for one week (in line with the FX Reset frequency), it will attract the same rate as the Main Refinancing Operation (MRO) conducted on that day in EUR. The EUR leg (or non-USD leg) is therefore also a floating leg, so the above diagram should really show all 12 weeks (12 MRO operations, which are currently operated at 0% for EUR).

Collateral Haircuts

- Note that there is a haircut applied to the collateral being posted to the central bank.

- It would be somewhat bizarre to place USD collateral with your local central bank and pay OIS + 25 basis points, plus a 0.5-1.5% haircut, just for the privilege of converting it into cash.

- Therefore, I believe all of the collateral received in these USD auctions will be non-USD. This means that the local central bank will apply an FX-related haircut to the collateral being posted.

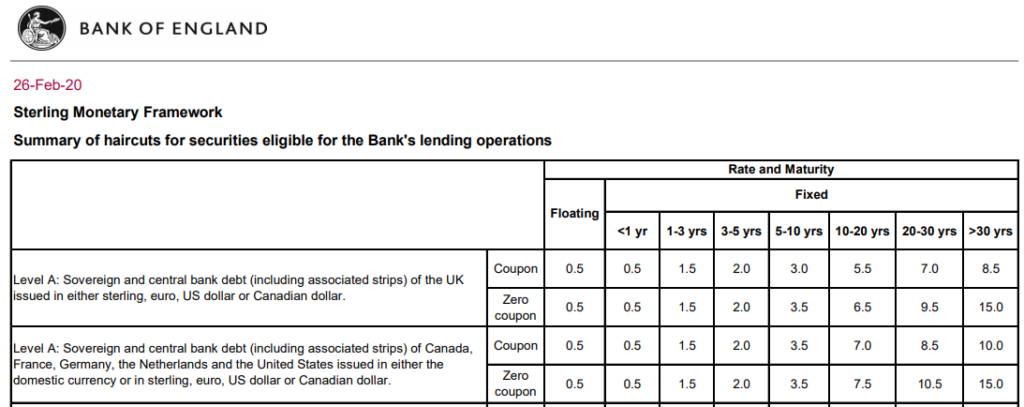

- From the BoE website, this haircut is a minimum of 6.5%:

Just to stress that footnote:

A minimum of 6pp [Clarus: percentage points] is added to haircuts to allow for currency volatility for non-sterling denominated securities in non-US dollar denominated securities in the US dollar repo facility.

Sterling Monetary Framework Bank of England

BUT! But! The ECB FX haircut is 12%!

Risk control measures: The usual risk control measures..will be applied. In addition, unless another percentage is indicated in the tender announcement for the relevant operation, a margin of 12% will be applied to cater for foreign exchange rate risk

USD Tender Procedures at the ECB

If a bank has access to both the BoE and the ECB, I guess they could post EUR collateral to the BoE at a 6% haircut and get their effective EURUSD swap much cheaper? That’s a bit weird….!

Anyway, let’s assume that banks won’t be playing the system. These haircuts serve to increase the effective cost of the cross currency swap. Rather than being the equivalent of OIS + 25 basis points, the actual basis will be larger. At the moment, with EONIA down around -50 basis points, the effect is to make the basis about +31 basis points (at a 12.5% haircut).

Crucially, that is still way below market levels. And I mean WAY below. The implied OIS basis for the past week has been over 100 basis points (average of about -140bp when expressed versus EONIA).

On the face of it, this is free money being offered to market participants.

Allocations

Let’s assume that banks eligible to participate in these auctions understand the mechanics above. They would be crazy NOT to participate, right?

Well, there is still somewhat of a stigma associated with accessing USD from your local central bank rather than from the open market. I’ve never really understood that viewpoint. If central banks are willing to lend to the market at such cheap levels, the market should “fill their boots” and get on with distributing the USD in the market.

So what have we seen this week? The total USD allocations are available over on the FRED website, updated once a week (@ FRED it would be very helpful to update your data daily during the crisis!).

Showing;

- Peak allocations across all central banks have been as high as ~$600bn across year end in 2008.

- However, this is measured as the total outstanding. So it will have accrued over a few months as banks took more and more USD over year-end – it isn’t the maximum allocation in a single week.

- Even in times of stress subsequent to this, such as the European Sovereign Debt Crisis, total outstanding (and weekly) allocations have only reached ~$100bn.

- This weeks total allocation was ~$160bn, so certainly significant.

- The key is whether banks decide to take even more next week.

For those who want to follow the data as it comes out, the results from the major central banks are linked below, Click back on these next Wednesday to see the allotments come in:

- US – New York Fed, including all links to other Central Banks at the bottom.

- Switzerland – SNB.

- Europe – ECB.

- UK – BoE.

Note that the New York Fed has also published all of the USD results, consolidated, here. The format is a pig to work with in Excel, but I am assuming this is the ultimate source of the FRED data.

Further Reading

The central banks themselves provide plenty of background to these operations as well. For those really digging into this, it is also worth having a read of the following:

ECB – What are currency swap lines?

Plus the even more in-depth Tender Procedure, in which I discovered the weekly FX Reset for the EURUSD operations.

The final bit of reading are the FRED notes themselves:

FRED – Central Bank Liquidity Swaps

Once again, FRED setting the bar very high there for data providers to accurately describe what their data is actually showing!

In Summary

- Central bank FX swaps are considered a key component in the crisis response.

- They are akin to an OIS vs OIS Cross Currency Swap for three months.

- With a spread of just 25 basis points over USD OIS (plus haircut, equating to an all-in cost of ~31 basis points) these are the cheapest source of USD funds out there.

- To be clear, the central banks are offering USD funds at rates way below those implied in the market (i.e. at a tighter implied cross currency basis).

- With 14 banks now able to access USD from the Fed, it has had some soothing effect on the market. Implied 3 month Cross Currency Basis has contracted, but only slightly.

- Next weeks USD auctions from the Central Banks are going to be very closely watched by markets.

Update: Daily USD auctions will now be offered: