- Cross Currency Swaps exchange a funding position in one currency for a funding position in another currency.

- The interbank market trades a resettable floating-floating swap, incorporating a USD cash payment to reset the mark-to-market close to zero at each coupon date.

- We explain the nuances of the product via the cashflows.

- The cross currency swap market has particular price dynamics that have evolved in recent times.

Explaining a cross currency swap to non-market participants gets complicated very quickly if we try to draw parallels with either FX Forwards or Interest Rate Swaps. The best way to think of Cross Currency Swaps is to forget what you think you know and start from the basics.

Definition

A broad definition serves little purpose here as it would simply state:

The exchange of cash-flows and associated notional amounts in one currency for another

Rather, we need to consider what people actually mean when they say “Cross Currency Swap”:

An OTC Interest Rate Derivative with physical exchange of notional and interest amounts between two currencies. The physical exchange of the currency amounts occurs on the start and end dates of the swap contract. The interest amounts are calculated according to the outstanding notional amount of each currency and are physically exchanged on every interest payment date for the life of the trade.

Use

What are Cross Currency Swaps used for? A broad use-case would simply state:

To exchange cashflows in one currency for another.

Again, we need to consider why market participants actually choose cross currency swaps:

To transfer a funding position in one currency for a funding position in another currency.

What do we mean by a “funding” position? It is the requirement to physically make loans and deposits. Whilst most OTC derivatives trade as contracts for difference, the exchange of funding makes a Cross Currency Swap a physical swap. The underlying is a financial asset (cash) rather than a hard commodity.

Market Conventions

The Cross Currency Swap market has always been split in two – the Dealer-to-Dealer market versus the end-user Dealer-to-Client market. The “market standard” product that trades in the Dealer community is far removed from what an end-user client typically requires. However, it has evolved into the most efficient risk-transfer mechanism that we have for basis risk.

Remember that Cross Currency Swaps are still not offered for Clearing, therefore any standardisation efforts continue to face headwinds.

D2D Markets

Dealers trade a very specific structure:

Floating-Floating Resettable Basis (a.k.a. MTM Swaps)

- A cross currency swap with initial and final exchange of notional (occurring on the spot value date and subsequently reversed on the final maturity date of the swap).

- The USD leg, for all major currency pairs, will be 3 month USD Libor. There will be a zero spread on the USD Libor leg.

- The foreign currency leg will be the prevailing 3 month interbank rate (“‘Ibor”, e.g. Libor for GBP or Euribor for EUR). The “price” of the trade is the spread, in basis points, over this foreign currency leg (although it is now typically a negative spread).

- Interest payments will occur every 3 months, with cashflows physically exchanged between the counterparties.

- Each payment is calculated within currency as:

- (Notional * No. Of Days * 3m Libor)/360

- The Resettable (or Mark to Market) element of the swap refers to the USD notional amount. Every 3 months, the current FX rate between the two currencies is observed. The difference between the previous FX rate and this new FX rate is cash-settled in USD and paid on each interest payment date (excluding maturity).

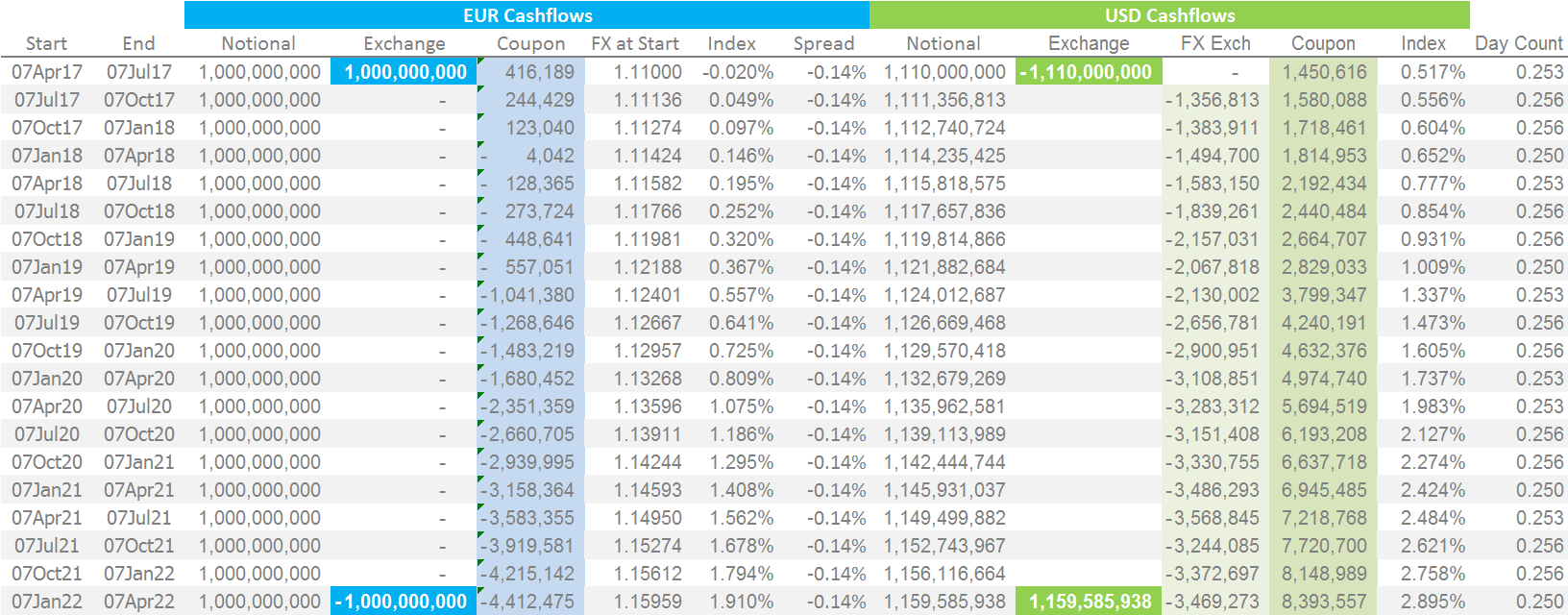

Cashflows

The easiest way to explain a Cross Currency Swap is to talk about a loan in one currency versus a loan in another currency. Throw in some cashflow diagrams and talk of principal exchanges, and the story is fairly complete.

Via the beauty of Excel, here is what a currency swap should look like:

Showing;

- A market standard, resettable cross currency swap between EUR and USD.

- The swap has a maturity of 5 years.

- From the perspective of my spreadsheet, I am receiving €1bn upfront versus paying $1.11bn.

- I must then repay the €1bn at the end of the swap. In exchange, I will receive the USDs back.

- We do not expect €/$ FX rates to stay constant throughout the life of the swap. To therefore forecast the FX-resetting element, we calculate the expected FX rate at each coupon date in the future. These FX rates are calculated as FX Spot * df(€$)/df($), where df(xx) is the respective discount factor on each curve at a given date.

- Accordingly, we expect the USD notional amount to be $1,159,585,938 for the final 3 month period of the swap.

- By extension, I therefore expect to pay-out a small amount of USD every time the FX rate resets on a coupon payment date. I am expecting to cash-settle the interest rate differential between the two currencies over time.

- As a result, I expect to receive back $1,159,585,938 at maturity. This is the value of all of the USD notional payments I have made over the life of the trade.

- Each coupon payment on the EUR side is based on a notional of EUR1bn. We use our forecasting curves to project where Euribor 3m will be on each coupon payment date. Coupled with the known coupon on the trade (a spread of minus 14 basis points in this example), I can project my expected coupon cashflows.

- Each coupon payment on the USD side is based upon the expected USD notional. As time moves forwards, just as with Libor fixings, these will become known USD notionals. At the time of the final FX fixing in January 2022, all of the cashflows on the swap will be known.

- I cannot stress enough that every payment is physically exchanged in hard currency. There is no netting of cashflows between currencies.

- To bring our analogy back to the beginning of this section, in this example I am borrowing EUR1bn for 5 years, versus lending USD1.11bn for the same period.

- Therefore, on each coupon payment date I must pay EUR interest (on my loan). In return, I receive USD interest (because I have lent the USD out).

- Thinking of it this way, you can see why we refer to this trade as paying the cross currency basis. I am paying to borrow EUR funds versus lending USD.

- Equally this should explain why this is a funding trade. We are literally exchanging a loan/deposit in one currency for a loan/deposit in another currency.

- The pricing variable that we refer to as the Cross Currency Basis is the spread above/below the non-USD currency leg.

D2C Markets

Dealers trade a very specific structure. Customers do not. The end-user market for cross currency swaps is typified by its’ vagaries. Therefore, in our example above we could equally change:

- The floating Euribor leg for a fixed rate.

- The floating USD leg for a fixed rate.

- Both legs for a fixed rate.

- Remove the initial exchange.

- Change the start date to one week forward.

- etc. etc….

One thing is for sure – very few customers will want to trade the resettable structure with a variable notional. This is very unlikely to satisfy their hedging requirements.

Market Dynamics

Prior to the financial crisis, cross currency swaps were a sleepy corner of the capital markets, little affected by the whims of monetary policy or economic outlooks. The razor-thin spreads over non-USD floating indices simply reflected the (small) imbalances between supply and demand for funding in a given currency at that particular time. These spreads were typically treated as mean reverting (to zero). After all, in a capital markets world where all banks on the planet assumed they could roll unlimited funds at Libor flat, why would you pay a premium over Libor to lock-in term funding. (How strange it is to see those words written down in 2017… )

The GFC changed all of that. Now;

- Banks typically discount cashflows back into their domestic currency.

- USD is broadly considered to be the global “risk-free” currency and most other funding markets trade at a premium (negative basis spread) to USD.

- Any changes in monetary policy that may tighten (loosen) the supply of USD will cause short-dated cross currency basis to head lower (higher).

- Issuers and investors are more than happy to pay steep “premiums” (relative to their domestic currencies) to lock-in term USD funding.

- QE-policies significantly affect the supply and demand imbalance within a particular debt market. The introduction of QE in e.g. the UK made it very attractive for non-UK issuers to issue GBP-denominated debt into the UK market in order to sate the appetite of investors who would otherwise struggle to get their hands on GBP-denominated bonds. This caused a downward pressure on GBP/USD basis as issuers swapped their GBP liabilities back into their domestic currencies.

- Due to the increased linkage with monetary policy, coupled with scrutiny over funding markets in general, Cross currency basis is now much more volatile than it once was.

- Volumes continue to increase. The latest BIS survey suggested that $82bn trades every single day in cross currency swaps.

In Summary

- Cross Currency Swaps are a physically delivered swap entailing the exchange of notional and interest payments in one currency for another.

- They are not currently available for Clearing therefore operate in a bilateral market.

- The D2D market trades a very specific structure.

- The D2C market is varied.

- It is important to understand the exact cashflows in a cross currency swap to have an understanding of the market dynamics.

- The cross currency market as it exists today is almost unrecognisable to the one that existed ten years ago.

A little detail missing here: the CSA applied to the swap. In the D2D market, the vanilla liquid swaps seem to have a specific CSA, which then affects how you price the swap (as with IRS).

The other point is that M2M is only usual for major currencies, presumably partly because it relies on a spot fixing, but also by having a fixed principal the basis swap becomes effectively an FX Forward trade.

USD CNH Cross Currency Swaps are cleared in Hkex

Hi Kelvin – this is very true! I didn’t want to complicate the blog with reference to this as it is somewhat a limited offering at the moment – only two currency pairs and I believe a small maximum amount each day of around $50m. We are keeping an eye out in CCPView for any volumes, we haven’t seen any reported as yet.

Hi Phil – thanks for the comments. It is interesting that you reference the CSAs. At the moment, there is no true standard, even in the D2D market. This is something that ISDA tried to address with the SCSA and something that we hoped may have been resolved via the VM Big Bang in March. Whilst some CSAs are being simplified, we still cannot universally state that all D2D cross currency is priced with reference to an e.g. USD Cash CSA. This may well change if the OTC market continues down its’ path of standardisation, which most market participants agree would be beneficial in the long run.